I'm still unclear on the problems that Bitcoin is solving versus fiat. I can also imagine many issues that Bitcoin has that fiat doesn't. This post is a one-sided take, and it'd be more honest to put both the disadvantages/advantages side-by-side by fiat. There are clear advantages to our current system that we'd give up by switching more to Bitcoin; for example, if I lose my banking account login information, I can recover it with the help of a customer service representative. Whereas if I lose my wallet keys, I'm screwed.

Furthermore, fiat benefits the population because a central actor can intervene. I don't see it as necessarily evil that the Fed can perform quantitative easing to fight inflation or stimulate economic growth, say when a crippling pandemic hits. Could many of the issues you're highlighting be solved just by better functioning government?

Some other more specific issues:

State control of money has empowered corruption, surveillance, and restriction of people’s ability to save and transact freely.

Why/how does Bitcoin solve corruption? Also, all the transactions are public. If I'm performing Bitcoin transactions in China, the government will be able to surveil my transactions. Whereas, no one else can deduce my Bank of America transactions without having access to the system.

Lack of accountability

I'm not seeing how this solved by Bitcoin. Malefactors can obfuscate financial behavior with Bitcoin too.

Let me end by asking whether Bitcoin can solve significant problems better than fiat. Problems include climate change, suffering, risk of pandemics, risk of misaligned AI, disease, and poverty. With scant altruism resources, are we best served to invest it into Bitcoin projects in order to do the most good?

Hi Karthik, I appreciate your feedback. I've added a couple of paragraphs to the original post in order to cover more explicitly some of the points you've raised.

1. Seeing this article as a dishonest or one-sided take:

The article devotes an entire appendix to the most popular arguments against Bitcoin.

Nevertheless, the purpose of this essay is not to compare the pros and cons of Bitcoin with those of the fiat system, and to declare a "winner" on the basis of intellectual analysis.

Rather, it is to point out that, whatever form the global monetary system takes 50 years from now, it should reflect the preferences of individuals who are free to choose what is best for them. Unfortunately, today's monetary system has major drawbacks from which many people around the world wish to escape - but, because money is currently a government monopoly, these people have no alternative.

If you prefer using fiat money, then nobody should stop you. But if you need a form of money that can't be inflated away, that doesn't depend on the good behaviour of the authorities, and that you can receive directly without having it channelled through third parties (and if those requirements are more important than any drawbacks you might associate with such a system), then that option ought to be available to you too. That potential is what Bitcoin offers.

2. Regarding the benefit of having a central actor intervene with QE/interest rates, I've added:

debt accumulates in a vicious cycle: as the amount of societal debt outgrows the amount of money that exists (Figure 1), the only solution is to print and lend even more money – thereby creating more debt.

In other words, while the current system gives governments more freedom to print money and inject economic stimulus in the short term, most of this stimulus is required simply to pay down debt that was accumulated in previous rounds of spending. This is inherently unsustainable in the long run.

The Fed had to print trillions of dollars during the pandemic so that we wouldn't see mass insolvency. But the situation was only that dire in the first place because they'd allowed so much money (and therefore debt) to be created in the past. And by adding more money/debt to the system on this occasion, they've ensured that it will be even more vulnerable next time. The anonymous author of the "Fix the money" essay goes into more detail on this point.

3. How Bitcoin addresses corruption: if a small group of people have control over the money source in your society, some of them will inevitably abuse that power for their own ends. Furthermore, if you have corrupt officials in charge of handling aid money from abroad, then some of them will steal that money for themselves.

Bitcoin avoids these specific problems by having no centralised authority over its money supply, and by allowing people to receive money (e.g. aid) directly instead of having to rely on middlemen. It doesn't purport to solve all corruption per se.

4. Regarding how Bitcoin addresses privacy, I've added:

While the Bitcoin blockchain (the ledger containing all Bitcoin transactions) is public, payments are pseudonymous, and do not require the sort of personal information (e.g. name, bank account, or address) that governments, corporations, and merchants sell or leak on a regular basis. Further developments to Bitcoin (such as the Lightning Network, Taproot, Graftroot, and Schnorr Signatures) are already making it cheaper and easier to send bitcoins privately.

5. Bitcoin versus government accountability: if Bitcoin ruled the world, then governments wouldn't be able to simply print money in order to fund their unpopular ventures (as opposed to taxing their people and having to justify their expenditure). On an individual level, it's another reason why you can trust that your bitcoins won't be susceptible to inflation.

6. Losing your Bitcoin-wallet key: if you choose to take sole custody of your bitcoins (and it is a choice), then, yes, you are responsible for storing your key safely. The reason that your local bank can recover your account, on the other hand, is that they (not you) have custody of your savings.

That said, there is no reason why you couldn't make use of equivalent services in a Bitcoin economy. Bitcoin may not necessarily be user-friendly right now, but such relatively minor issues are unlikely to persist as the network undergoes development over the next few years – and it is this work that I encourage EA and other groups to support.

7. Whether Bitcoin can solve global issues better than fiat money: Bitcoin is just another form of money, so in theory, you can spend it on the same things that you would with fiat. The difference is that it appears to meet the fundamental requirements of sound money better than fiat does - in which case, the downstream benefits for issues such as poverty, climate change etc. would be huge.

8. "Could many of the issues you're highlighting be solved just by better functioning government?": I'm suggesting that Bitcoin is a way to achieve better-functioning government. Political/economic reform necessarily occurs at an institutional level.

Alex, I appreciate the thoughtful comment and all of the edits. I gave you an upvote, but I'm still far from convinced that this is worth EA's time and money. Most of what you've written so far as convinced me that poor, unstable governance is the ultimate pathology to treat, and Bitcoin is a potential ointment for (some) resultant symptoms. I know EAers work on improving election and democracy systems. A few more follow up thoughts on a few of your remarks:

Responding to (3) and (5): Sure, I see other issues that need to be worked out, for example, governments being able to tax fairly to pay for social goods such as schools and health care. I'm not convinced that the problems solved here outweigh those sorts of bad.

Responding to (6): How much of this is just fundamental though? Any sort of "customer service" will require a middle man, i.e. a brokerage or institution. It's not like we can retrofit the blockchain to have a "Forgot my Password" feature.

Responding to (7): But how much better? Are we better off into investing into anti-corruption projects or the democracy improvement ones?

poor, unstable governance is the ultimate pathology to treat, and Bitcoin is a potential ointment for (some) resultant symptoms.

Are we better off investing into anti-corruption projects or the democracy improvement ones?

A sound monetary system is a crucial element of a healthy democracy.

It is not enough to address these problems simply with better governance. An institution is vulnerable to the extent that it relies on a small group to govern responsibly; the aim of political reform is instead to construct a system that cannot be hijacked by the incompetent or authoritarian actors that it will inevitably encounter. The most foolproof way of doing that is to make it impossible (e.g. by technological means) for any single entity to wield such power in the first place.

That’s precisely the approach that Bitcoin takes: instead of relying on political leaders to self-regulate, or counting on imperfect carrot-and-stick institutions to police good governance, Bitcoin ends the government monopoly on money altogether. Instead of hoping that people vote more rationally, Bitcoin appeals to people’s economic self-interest, offering a way out of their failing monetary systems.

As a result, Bitcoin is perhaps the only effective measure that could help to democratise societies that are hostile to reform. Members of Effective Altruism have offered many suggestions for strengthening democracy in nations where there is already some kind of avenue for popular change. But when it comes to authoritarian states where the ruling regimes show no interest in ceding power, we seem to have had no answers until now. Bitcoin is unusual in that it initiates institutional change from the ground up; governments can no more stop its proliferation than they can switch off the Internet. It is no accident that the nations most hostile to Bitcoin tend to be the most authoritarian ones.

2)

I see other issues that need to be worked out, for example, governments being able to tax fairly to pay for social goods such as schools and health care.

I don’t see how fairer taxation is made more challenging by Bitcoin. Decentralised money is not an aberration that humanity has never seen before – we’ve been there for most of human history (commodity money, such as gold, is fundamentally decentralised). Bitcoin is essentially trying to create a digital version of the classical gold standard that prevailed until 1914. Lending, taxation, and public works still happened in that era – if anything, it was a relatively peaceful and prosperous time. There is no reason to believe the same would not be possible when using Bitcoin. Government-enforced paper money, on the other hand, is an aberration, and one that has consistently resulted in rapid devaluation (as we are seeing right now).

3)

Any sort of "customer service" will require a middle man, i.e. a brokerage or institution. It's not like we can retrofit the blockchain to have a "Forgot my Password" feature.

I've added this to the appendix:

8. “If you lose your private key, you lose your bitcoins forever”

Then take care not to lose your private key. Alternatively, use custodial wallets: services where your private keys are held by an institution, similarly to how you might entrust your savings to a bank. Multi-signature wallets also allow you to spread your risk between several keys or people. That said, the option to take sole responsibility for your savings is the fundamental point, and the problem is that it's not currently available to people who need it.

What are the main benefits of fiat that Bitcoin doesn't have?

Doesn't fiat allow governments to raise money more easily, by increasing the money supply and possibly easier taxation, to pay for important programs, including health care, education, research (and other public goods) and for emergencies (like COVID)?

All of those things would still be possible under a hypothetical "Bitcoin standard". The difference is that they wouldn't be funded by limitless money-printing and runaway debt.

The goal of Bitcoin is essentially to create a digital version of the classical gold standard (the monetary system used by Europe, the US, and other countries, before 1914). Under that system,

lending still happened;

governments still had the power to raises taxes for public projects; and

while governments would issue standardised notes that represented fixed amounts of gold, they weren't able to inflate the gold supply itself.

All that having been said: theorising is fun, but the success or failure of a currency ultimately depends on whether the individuals using it find that it serves their needs. Right now, there are many people around the world whose local currencies are clearly not serving their needs - but because money is currently a government monopoly, these people don't have an alternative. The point of Bitcoin, then, is simply to give people a choice.

This post is co-authored with Ben Garfinkel. It is cross-posted from the CEA blog. A PDF version can be found here.

Summary: Some strategic decisions available to the effective altruism m...

TL;DR: I'm releasing a website that ranks philanthropists according to EA principles and research, and allows users to re-rank the list using their own assumptions. I'd like feedback and help making it better. I'd especially like ideas for how to make the results more trustworthy. Funding may be available.

I recently built Impact List (impactlist.xyz), a site which ranks people by their positive impact via donations.

The goal is t...

Disclaimer: Although I work on the Groups Team at CEA, I’m writing this in a personal capacity, and this post does not constitute an endorsement by CEA.

Agency - the realisation that you really can just do things.

TL;DR

Biosecurity needs people (of any background) who are agentic and have a high execution velocity and track record....

Many of the world’s most pressing problems are linked to how money is created and distributed.

Money today has two critical flaws:

There’s no physical limit to how much money can be created.

People’s savings and transactions depend on the responsible behaviour of banks, governments, and other financial middlemen.

These flaws have far-reaching consequences:

Debt spirals: when major institutions default on their debts and crash the economy, governments can simply bail them out by creating and lending them new money. However, these additional loans create bigger debts that stifle growth and cause bigger crashes later.

Inflation: excessive money creation erodes the wages and savings of billions worldwide.

Inequality: new money flows to banks and wealthy investors first, letting them capture scarce assets and drive up prices for everyone else.

Spending without accountability, as governments use money-creation to quietly fund wars and other controversial ventures.

Financial extortion, surveillance, and censorship by oppressive regimes and predatory intermediaries.

Bitcoin is a new form of money, designed to offer a way out of these problems. Unlike conventional money, it has a fixed supply, allows people to take sole custody of their funds, and isn’t controlled by any government or bank. The result is an alternative monetary system that could reduce global inequality and weaken the financial stranglehold of even the most authoritarian rulers.

I recommend that Effective Altruism and similar organisations consider supporting the Bitcoin cause, by:

funding independent Bitcoin projects,

promoting Bitcoin-related discussion, and

analysing Bitcoin’s suitability as a vehicle for investment in long-term altruistic causes.

1. Modern (fiat) money and its problems

Today’s monetary system has been in place since 1971. Before 1971, most major countries used gold as money. Gold was an effective form of money because gold is scarce: as it has always been difficult and expensive to mine, there was no danger that anyone would dilute the value of your savings by flooding society with new quantities of gold.

When people started using bank notes for convenience, these notes were simply cheques that entitled the holder to a certain amount of gold at the bank. This meant that for every dollar, pound, franc etc. that existed, there was (in theory) an equivalent amount of gold held somewhere.

However, governments were eventually tempted to print more bank notes than they could back up in gold. When this overprinting became apparent, several major nations rushed to the US (which was holding most of the world’s gold reserves) to have their notes exchanged for gold before it ran out. President Nixon responded by severing the link to gold: bank notes would no longer be certificates of ownership; they would become the money itself.

As a result, we now live in an era of fiat money: government-issued money that can be created in theoretically unlimited amounts because it’s no longer tied to anything finite.

This system already shows signs of being unsustainable.

1.1. Debt spirals

The ability to create money without limit turns routine debt defaults into snowballing economic crises.

In most countries today, money is created almost entirely in the form of loans. This happens through two types of institution:

Commercial banks: the places that hold your savings. When banks give loans, the money isn’t taken from elsewhere; it’s created on the spot.

Central banks: government institutions that control a nation’s currency. They create money to lend to commercial banks or the government.

While lending isn’t inherently bad, there is always a risk that people will default on their debts. Every few years, a critical mass of people and businesses fail to repay their lenders, crashing the economy with a chain reaction of bankruptcies.

Economic crashes are not unique to the modern era. What is unique, however, is how governments use money creation to delay and worsen the problem. Rather than face political backlash from letting bankruptcies run their course and allowing bad debts to be written off, governments instruct their central banks to create and lend even more money to bail out the defaulting parties.

In other words, each rescue operation by the government amounts to paying off old loans with bigger loans, adding more debt to the system than they relieved. This guarantees the next crash will be larger, requiring an even bigger bailout, and setting up an even larger crash after that. Meanwhile, banks are incentivised to lend more recklessly, knowing they can keep the profits during the good times while relying on the government to rescue them when things go wrong.

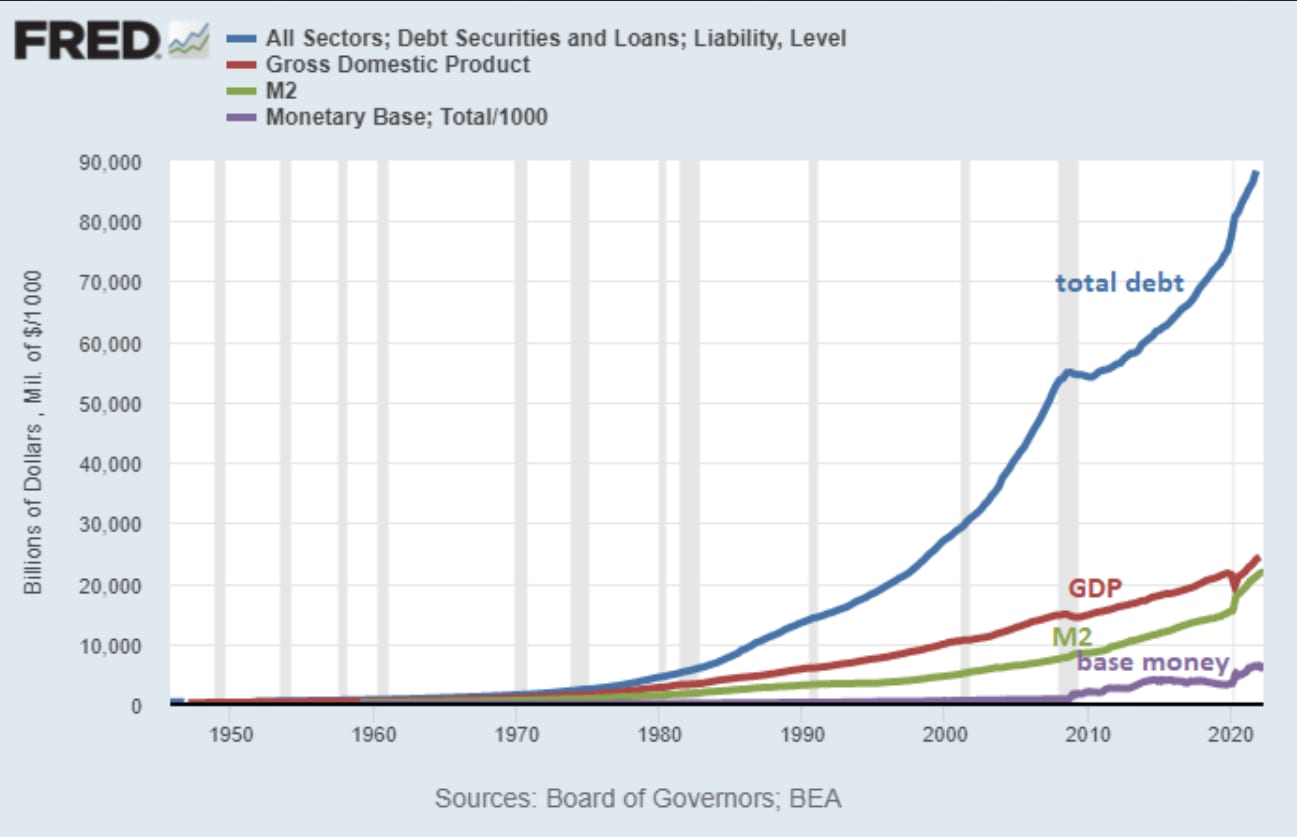

The massive debt burden strangles the economy even between crashes: as more of society’s income is needed just to pay the interest on a growing mountain of debt, less money is available for jobs, wages, or public services (Figure 1). This is a major reason why economies like the US, the EU, and Japan are chronically sluggish today.

Figure 1: Since 1971, total debt in the US has vastly outpaced both economic growth (GDP) and the total money supply. This means more and more debt is needed just to pay off old loans and generate the same amount of growth.

1.2. Inflation

The fact that money today can be created easily and without limit is highly unusual. Throughout history, every successful form of money was naturally difficult to produce more of: gold had to be mined, silver extracted from ore. This scarcity protected people from inflation – that is, it prevented anyone from creating so much new money that it diluted the value of what people already held.

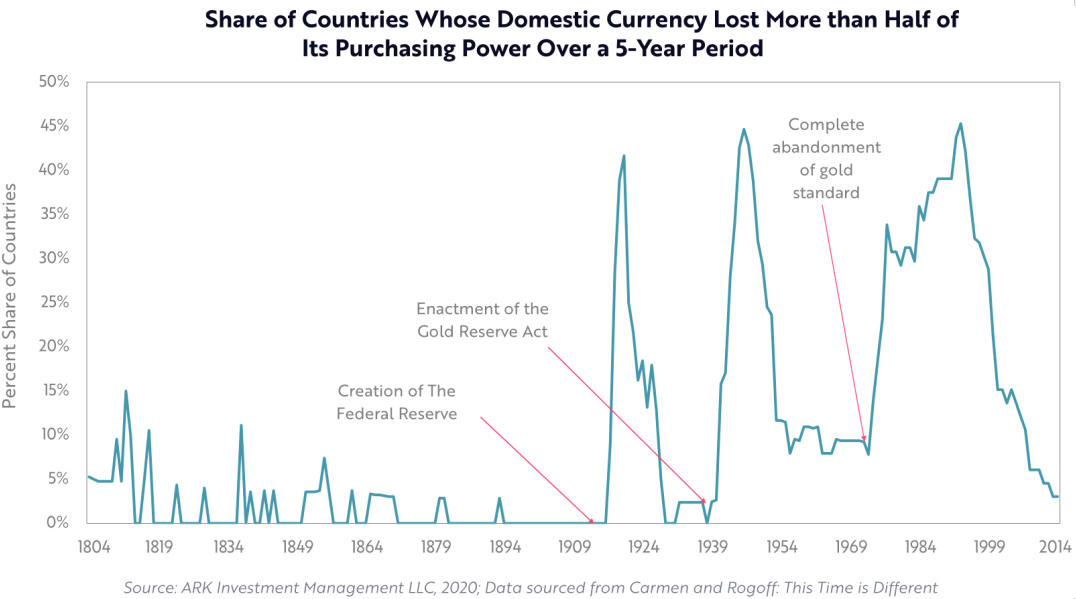

Modern policymakers do what they can to stop inflation from getting out of hand, but this sort of economic planning is extremely difficult, even assuming your intentions are good. The number of major inflation episodes has exploded as we’ve moved away from the gold standard, destroying savings and upending societies around the world.

Almost every year, a double-digit percentage of countries grapple with inflation that will cut the value of their currency in half over five years. The start of this trend coincides with the shift towards fiat money (Figure 2).

Figure 2: The shift towards a flexible money supply started with the temporary suspension of the gold standard during World War I (1914), and was completed with the abandonment of the gold standard in 1971. This correlates with an uptick in major inflation episodes globally.

1.3. Wealth inequality

New money is not distributed evenly.

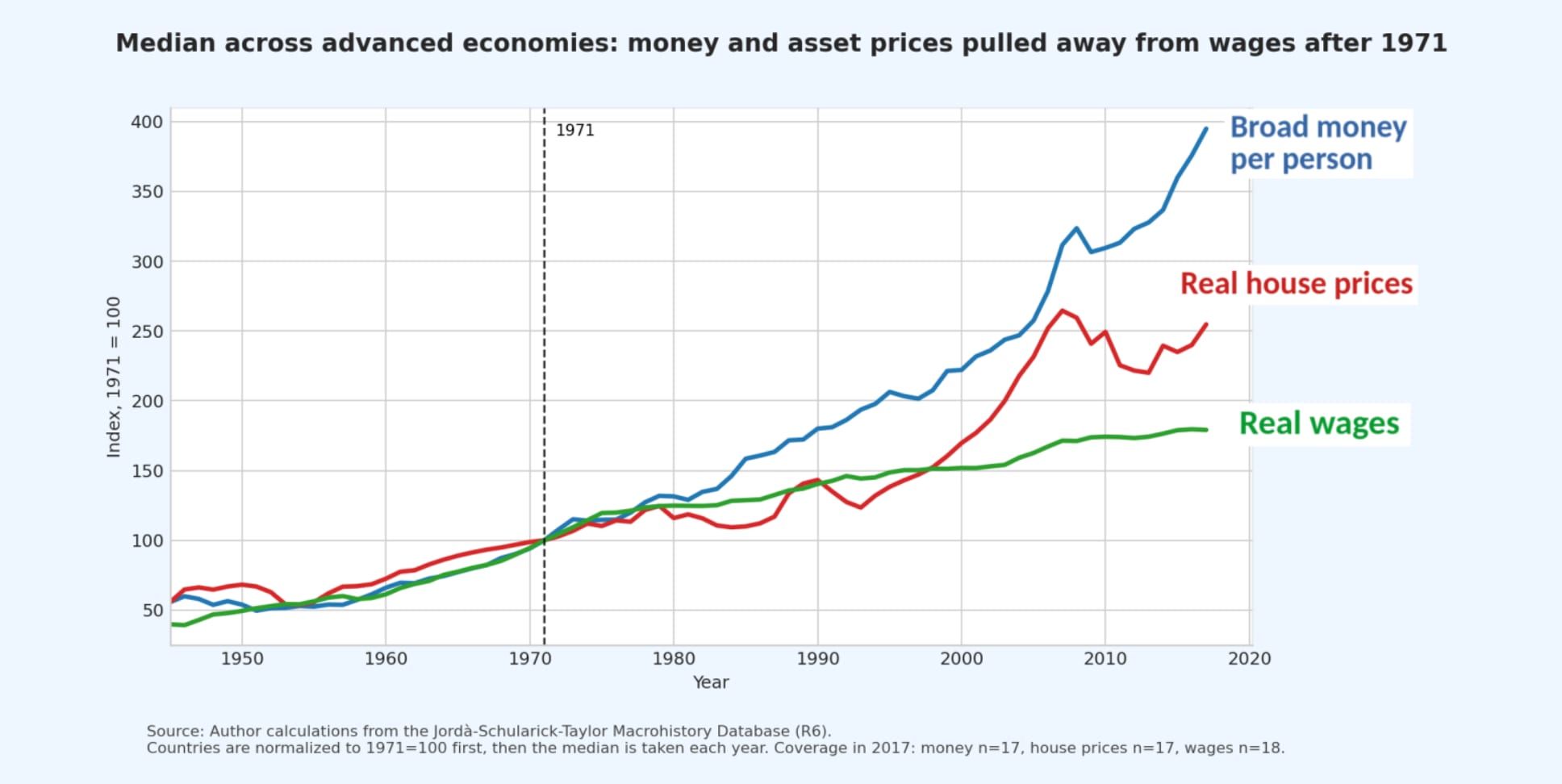

Because money is created through lending and bailouts, it naturally enters the economy through the financial sector rather than being distributed directly to citizens. This gives large banks and connected institutions a massive, arbitrary advantage: simply by being close to the money spigot, a select group gets to enjoy the benefits of this new wealth first, before it has had time to circulate and drive prices upwards.

The consequences for everyone else can be devastating. Financial institutions and their customers naturally use this influx of cash to buy up scarce, valuable assets like housing and stocks. This artificially drives up the price of those assets – enriching the wealthy people who already own them, but pushing them beyond the reach of the average wage-earner (Figure 3).

Ultimately, the working class and the global poor are left bearing the hidden costs of this newly created money, while seeing very few of the benefits.

Figure 3: Across advanced economies, real wages, house prices, and money supply largely grew together until 1971. After the shift to a pure fiat system, the money supply surged, flowing into financial assets and causing house prices to outpace wage growth.

1.4. Lack of accountability

Money creation gives governments a way to finance controversial activities (such as war) surreptitiously through inflation.Instead of imposing taxes and therefore having to justify their expenditure to voters, governments can quietly print and spend what they need, leaving their population to deal with the economic consequences years down the line. Their citizens, in turn, become emotionally and politically disconnected from their government’s actions, the true costs of which are no longer visible.

World War I was famously drawn-out because the participating nations resorted to printing paper currency far beyond what they could back up in gold.

Analysing a century’s worth of data, US Air Force veteran and legal scholar Sarah Kreps found that wars funded by money-printing are 20 per cent more popular than wars funded by taxation. In other words, money-printing blinds voters to the cost of war – and therefore makes them less inclined to pressure their leaders to shorten or avoid conflict.

1.5. Humanitarian issues

Modern money does not provide a realistic means for people to take direct custody of the value that they create. Instead, responsibility for one’s savings and transactions must be outsourced to banks, payment platforms, and other intermediaries.

However, each of these financial middlemen is a potential avenue for extortion, surveillance, and censorship – especially for the majority of the world's population that lives under authoritarianism. The institutional barrier to entry also means that many people are cut off from the financial system entirely.

Former UN Secretary General Ban Ki-moon declared in 2012 that corruption “prevented 30% of all development assistance from reaching its final destination”. In one Oxfam study, researchers could only verify that 7% of the USD 28 million meant for Ghana between 2013 and 2015 had arrived safely.

Only 7% of global transactions are still carried out with cash (the only private way to transact with fiat money). That number is expected to shrink rapidly, reducing people’s financial privacy to nearly zero.

The user data amassed by online payment platforms WeChat and Alipay (which have over a billion users) reportedly inform government-mandated social-credit scores that regulate people’s everyday behaviour. These systems are based not just on finances, but also on political opinions, identity, and social interactions.

2. How tractable is this issue?

What makes this issue potentially tractable is the existence of a proposed solution that requires only development and scaling.

Bitcoin was created amidst the Global Financial Crisis, specifically to address the problems listed above. Whereas conventional money consists of centralised and local currencies with unlimited supply, Bitcoin offers a type of money that is:

decentralised: no single entity has the power to manipulate the money supply, to seize your assets, to exclude you from the network, or to censor your transactions;

global: it isn’t confined to any particular jurisdiction;

finite: the number of bitcoins in existence cannot be inflated beyond 21 million; and

digital: it exists purely in computer software, and has no physical form.

Bitcoin is modelled largely on gold: since the asset itself is finite, there is no risk that one’s savings will be diluted by an open-ended increase in the number of bitcoins. Furthermore, there is no central authority that is motivated to devalue Bitcoin in order to manage debt cycles, or to fund wars or corporate bailouts.

However, while gold’s physical bulk led to its eventual centralisation and representation in paper form, bitcoins are massless and transmissible electronically – they are designed to replicate gold’s sound monetary properties in digital form.

2.1. How Bitcoin works

Every financial system requires a ledger: a master list of accounts and transactions that declares who owns what. In our conventional system, this ledger is maintained by central authorities: commercial banks track your personal savings, while central banks track the national money supply. Because these institutions have exclusive control over the ledger, they have the power to freeze accounts, censor transactions, or create new money by adding numbers to the list.

Our conventional financial system also works in layers. At the top are everyday networks like Visa, which process millions of small transactions quickly. Below these are slower, highly secure settlement layers (like FedWire in the US, or SWIFT globally). Banks use these base layers to bulk-settle the transactions made in the layers above, updating their master ledgers.

Bitcoin uses a similar layered structure, but without needing a central authority.

2.1.1. The Blockchain (base layer)

The Bitcoin blockchain is the ultimate settlement layer - the ledger that records every Bitcoin transaction ever made. However, because Bitcoin is decentralised, it does not rely on a single authority to hold this ledger. Instead, the blockchain is copied and distributed across tens of thousands of independent computers (called “nodes”) worldwide.

Whenever a user wants to make a bitcoin payment, they broadcast their proposed transaction to this global network.

2.1.2. Mining and Proof of Work

The Bitcoin network includes participants known as “miners”, who listen for proposed transactions, bundle them into “blocks”, and race to add them to the blockchain.

Adding a block is a massive cryptographic exercise requiring large amounts of electricity and computing power. This is an intentional security feature, known as “Proof of Work.” Under this rule, if there are competing versions of what the ledger looks like, then the network trusts the version that took the most computational work to create. Therefore, to fake a transaction or rewrite the ledger, an attacker would have to continuously out-compete all the honest miners combined – which they could only do if they controlled a majority of the network’s computing power. This makes Bitcoin practically impossible to hack.

The first miner to add each block is rewarded with newly created bitcoins, alongside small transaction fees paid by the users. Crucially, the number of bitcoins awarded to miners is hard-coded to decrease automatically over time, mathematically guaranteeing there will never be more than 21 million bitcoins in existence.

Bitcoin’s monetary policy is thereby enshrined in code; no CEO, politician, or central bank can change it.

2.1.3. The Lightning Network

Because Bitcoin's base layer prioritises absolute security and decentralisation, it processes transactions relatively slowly. It is designed for high-value settlements, similar to a global wire transfer or moving physical gold.

For everyday purchases, Bitcoin uses a secondary layer called the Lightning Network, which facilitates instant transactions for virtually zero fees. It does this by allowing two parties to exchange bitcoin separately from the main blockchain, broadcasting the final balance to the base layer only once they are finished. Just as Visa batches millions of small retail purchases before settling up with the banking system at the end of the day, Lightning allows the world to use Bitcoin for daily commerce while keeping the base layer as a safety net.

2.2. How Bitcoin could provide a better form of money

2.2.1. Creating a fairer and stabler global economy

Bitcoin gives people a way to opt out of failing fiat currencies, in favour of a money that is resistant to long-term devaluation. In doing so, it could help to shrink the asset bubbles (such as those in real-estate markets) that commonly result from people’s attempts to escape inflation.

Moreover, Bitcoin aims to create a monetary system that is more befitting of today’s digital and borderless economy. As a global form of money that runs natively on the Internet, it could help people to move more freely around the world, creating more equal competition for labour, and giving workers more of the value that they produce. Wealth would then accumulate in countries that export labour, supporting local businesses and infrastructure.

A Bitcoin-based economy would also likely see the decline of big banks – especially those deemed “too big to fail”. As they lose their special relationship with governments and their control over people’s money, banks and other financial corporations would need to provide useful services, instead of relying on bailouts.

2.2.2. Disincentivising wars

If Bitcoin were to replace fiat currencies as the preferred form of money, it is likely that wars would no longer be financed as easily as they have been for the past century. With governments unable to simply print and borrow more bitcoins behind the scenes, military ventures would likely face greater public scrutiny, and become even more of a last resort than they are today.

2.2.3. Making international development more effective

Bitcoin transactions do not require handling or approval by third-party institutions. As a result, they make it possible for people to receive aid money directly, circumventing potentially corrupt or obstructive middlemen.

Bitcoin could also promote greater financial inclusion. In a world where smartphones outnumber bank accounts, it provides a way for people to save and transact without needing to seek permission – all that is required is an Internet connection.

2.2.4. Undermining authoritarianism and promoting self-sovereignty

Bitcoin allows one to take sole custody of one’s money: your funds are yours alone, usable and accessible from anywhere, simply by means of a password that can be carried in your head. Dictators who refuse to make democratic concessions could therefore face mass capital flight, as their most productive citizens leave for more favourable societies – this time taking their money with them.

2.2.5. Undermining mass surveillance

While the Bitcoin blockchain (the online ledger containing all Bitcoin transactions) is public, payments are made only pseudonymously, and do not require the sort of personal information (e.g. name, bank account, or address) that governments, corporations, and merchants sell or leak on a regular basis.

Further developments to Bitcoin (such as the Lightning Network, Taproot, Graftroot and Schnorr Signatures) are already making it cheaper and easier to send bitcoins privately.

2.3. But why Bitcoin specifically?

At this point, it’s necessary to differentiate Bitcoin from the rest of the crypto universe that was spawned in its wake. Given all the alternative cryptocurrencies (“altcoins”) and blockchain-based products out there, why should we pay special attention to Bitcoin?

2.3.1. Most other cryptocurrencies serve different purposes.

Nearly all of them can be dismissed at the outset, on the grounds of being useless, irrelevant, or simply scams: many people have realised that inventing your own money/technology and convincing others of its utility for five minutes can make you rich. Some altcoins were even launched as a joke.

A few remaining cryptocurrencies are arguably helpful or at least well intended, but specialise in entirely different uses from those of Bitcoin, and therefore operate according to different rules. Taking a look at some of the biggest altcoins (in terms of market capitalisation) currently out there:

Ethereum (along with similar platforms such as Solana) is designed to support various software applications that also make use of blockchains. This is where you’ll hear terms like “decentralised finance” (DeFi), “non-fungible tokens” (NFTs), or “Decentralised Autonomous Organisations” (DAOs).

There’s been some debate over just how useful these applications will be, and whether it even makes sense to use blockchains in this way. It has also been suggested that, even if such uses prove legitimate, they could simply be incorporated into the Bitcoin system in due course. Whatever your view, the point is that these kinds of cryptocurrency aren’t competing with Bitcoin on global monetary reform – which means that their altruistic potential is significantly different.

Stablecoins are cryptocurrencies that (in theory) have their value pegged to that of a stable reserve asset. Tether and US Dollar Coin, for example, are popular stablecoins that are both programmed to be worth 1 USD, always. This offers some respite to people in developing nations who need a way to keep their savings safe (both from the local authorities and from domestic inflation), but who can’t accept the price volatility that is inherent to Bitcoin at this early stage.

Again, however, such altcoins have little relevance to Bitcoin’s long-term objective – the aim of Bitcoin is not to express fiat money as cryptocurrency; it’s to escape fiat money altogether.

Ripple is also primarily a payment network, but one that acts as an intermediary between banks. It confirms transactions using a consensus mechanism operated by bank servers.

This has nothing to do with Bitcoin.

So, if you’ve only ever heard about “crypto/blockchain” in the collective, or if your main exposure to cryptocurrency has been through speculative gambling, then it may not have been apparent why the various cryptocurrencies out there actually exist, and how they differ from one another. However, if the aim is to work out which is best placed to solve the fundamental problem of fiat currency, then one can’t simply treat them as interchangeable – there’s a huge amount of diversity, for better or worse.

2.3.2. Bitcoin benefits from its network effect.

That said, Bitcoin has seen its share of copycats that ostensibly seek the same objectives as Bitcoin, while claiming to offer improvements in the form of minor tweaks to the original protocol. For example,

Bitcoin XT, Bitcoin Classic, Bitcoin Unlimited, Bitcoin Cash, and Bitcoin Gold are "hard forks" (i.e. alternatives derived from the original Bitcoin code) that use different block sizes from that used by Bitcoin. (The block size refers to the standardised size of each discrete data segment in the blockchain.)

Litecoin is essentially an imitation of Bitcoin, but secures transactions with a different cryptographic algorithm (Scrypt as opposed to SHA-256), and caps its supply of coins at 84 million as opposed to Bitcoin’s 21 million.

However, none of these alternatives has achieved anything like the lasting success of Bitcoin. Of the hard forks, only Bitcoin Cash (currently the 29th-biggest cryptocurrency) has any kind of relevance, while Litecoin has dropped to 21st place after falling out fashion years ago. Bitcoin, on the other hand, has held between 40 and 60 percent of the total cryptocurrency-market capitalisation for the past five years (it used to be above 80 percent when fewer cryptocurrencies existed). This has kept it between 2 and 5 times the size of Ethereum (the second-largest cryptocurrency), and far bigger than any altcoin that is designed for the same purpose as Bitcoin.

The reason for Bitcoin’s dominance is simple: the power of any social network (such as a language, social-media website, or currency) lies not in how difficult it is to create, but rather in the number of people who have opted in to the system. This is especially true of cryptocurrencies, where the security of the network (i.e. the amount of computing power that a malicious actor needs before they can manipulate transactions) grows with the number of participating nodes. Therefore, for any competitor to oust Bitcoin as a decentralised store of value, it would need to be radically better to the point that a critical mass of people would voluntarily abandon a network containing decades’ worth of investment, infrastructure, and security, all of which was responsible for guaranteeing the value of their own assets.

Another issue is that it is difficult to fully replicate Bitcoin’s decentralised structure. It’s impossible to point to any person or group that has significant authority over the Bitcoin network in the long term: the pseudonymous founder(s) of Bitcoin stayed around only long enough to hatch the idea, before vanishing for good. However, with Bitcoin now having established itself as the leading cryptocurrency, any competitor would need to amass significant resources and personnel in order to build and promote their new system, which would only undermine the narrative that it is a truly decentralised network free from top-down influence.

So, why should we consider Bitcoin specifically as the antidote to fiat money?

It’s by far the most (and perhaps the only) promising candidate. Why would you not?

3. How neglected is this issue?

Global adoption of Bitcoin is still relatively low, but increasing quickly. Much of this is undoubtedly due to mere price speculation, but there are also regions where Bitcoin is gaining public favour for its empowerment of the financially disenfranchised (e.g. in Nigeria, Cuba, Russia, Afghanistan, and Palestine). I think this indicates a need for more people who can accelerate and guide its development.

The Human Freedom Index includes consideration of “access to sound money”. However, as far as I am aware, the Human Rights Foundation is the only charity/non-profit that actively promotes financial sovereignty and the role of Bitcoin in achieving it.

I have seen very little interest in this topic within Effective Altruism. This essay is only the second detailed post on Bitcoin that I can find in this forum (the first one having been published just over a week ago). In my own conversations with EA members, the general reaction to Bitcoin alternates between polite interest and outright scepticism. Given that Bitcoin is a potentially transformative development that is most likely here to stay, I think it is time to study this issue seriously.

4. Suggestions for Effective Altruism and members

4.1. Supporting Bitcoin projects/organisations

A common institutional approach, both within Bitcoin and in similar technical fields, has been to fund independent contributors to open-source Bitcoin projects. Examples include the grant programs by Spiral, OpenSats, and the Human Rights Foundation.

The Summer of Bitcoin is another example worth considering: it’s a global online internship program that introduces university students to open-source development of Bitcoin applications.

That said, I am not aware of any efforts to analyse the cost-effectiveness of such projects.

At an individual level, one could consider working for a Bitcoin-related company (Bitcoiner Jobs is a popular website for such opportunities). I would recommend considering any role that improves the performance, robustness, or accessibility of the Bitcoin network; software engineers are in greatest demand, but there is also a significant need for operations and communications staff.

4.2. Bitcoin as a means of long-term investment for altruistic causes

Of course, there can be no certainty about how well Bitcoin will survive contact with the future. On the other hand, it’s done remarkably well since 2009. If it continues on this trajectory, and succeeds in establishing a new global reserve currency (or something similar), then its potential future upside dwarfs what one risks losing by adding it to the portfolio at this (still very early) stage in its adoption curve. A relatively small investment now could yield a massive altruistic payoff in several decades.

4.3. Education and discussion

Above all, what this topic needs is more awareness and understanding.

An important step that Effective Altruism could take immediately is to initiate informed discussion of Bitcoin on the 80,000 Hours podcast with Rob Wiblin. The first guest I recommend inviting is

Lyn Alden: an engineer and financial analyst who has written many detailed articles on the the workings of Bitcoin, as well as on the macroeconomic context that makes it so compelling right now. Here is one of her more entry-level talks on one of the world’s most popular Bitcoin podcasts.

I also recommend interviewing

Alex Gladstein: Chief Strategy Officer of the Human Rights Foundation. He can tell you about the problems encountered by the billions of people around the world who don’t have access to acceptably stable currencies. He can also tell you about the many people who already use Bitcoin in order to safeguard their financial sovereignty.

Appendix: responses to common criticisms of Bitcoin

8. “If you lose your private key, you lose your bitcoins forever”

Then take care not to lose your private key. Alternatively, use custodial wallets: services where your private keys are held by an institution, similarly to how you might entrust your savings to a bank. Multi-signature wallets also allow you to spread your risk between several keys or people. That said, the option to take sole responsibility for your savings is the fundamental point, and the problem is that it's not currently available to people who need it.

I'm still unclear on the problems that Bitcoin is solving versus fiat. I can also imagine many issues that Bitcoin has that fiat doesn't. This post is a one-sided take, and it'd be more honest to put both the disadvantages/advantages side-by-side by fiat. There are clear advantages to our current system that we'd give up by switching more to Bitcoin; for example, if I lose my banking account login information, I can recover it with the help of a customer service representative. Whereas if I lose my wallet keys, I'm screwed.

Furthermore, fiat benefits the population because a central actor can intervene. I don't see it as necessarily evil that the Fed can perform quantitative easing to fight inflation or stimulate economic growth, say when a crippling pandemic hits. Could many of the issues you're highlighting be solved just by better functioning government?

Some other more specific issues:

Why/how does Bitcoin solve corruption? Also, all the transactions are public. If I'm performing Bitcoin transactions in China, the government will be able to surveil my transactions. Whereas, no one else can deduce my Bank of America transactions without having access to the system.

I'm not seeing how this solved by Bitcoin. Malefactors can obfuscate financial behavior with Bitcoin too.

Let me end by asking whether Bitcoin can solve significant problems better than fiat. Problems include climate change, suffering, risk of pandemics, risk of misaligned AI, disease, and poverty. With scant altruism resources, are we best served to invest it into Bitcoin projects in order to do the most good?

Hi Karthik, I appreciate your feedback. I've added a couple of paragraphs to the original post in order to cover more explicitly some of the points you've raised.

1. Seeing this article as a dishonest or one-sided take:

The article devotes an entire appendix to the most popular arguments against Bitcoin.

Nevertheless, the purpose of this essay is not to compare the pros and cons of Bitcoin with those of the fiat system, and to declare a "winner" on the basis of intellectual analysis.

Rather, it is to point out that, whatever form the global monetary system takes 50 years from now, it should reflect the preferences of individuals who are free to choose what is best for them. Unfortunately, today's monetary system has major drawbacks from which many people around the world wish to escape - but, because money is currently a government monopoly, these people have no alternative.

If you prefer using fiat money, then nobody should stop you. But if you need a form of money that can't be inflated away, that doesn't depend on the good behaviour of the authorities, and that you can receive directly without having it channelled through third parties (and if those requirements are more important than any drawbacks you might associate with such a system), then that option ought to be available to you too. That potential is what Bitcoin offers.

2. Regarding the benefit of having a central actor intervene with QE/interest rates, I've added:

The Fed had to print trillions of dollars during the pandemic so that we wouldn't see mass insolvency. But the situation was only that dire in the first place because they'd allowed so much money (and therefore debt) to be created in the past. And by adding more money/debt to the system on this occasion, they've ensured that it will be even more vulnerable next time. The anonymous author of the "Fix the money" essay goes into more detail on this point.

3. How Bitcoin addresses corruption: if a small group of people have control over the money source in your society, some of them will inevitably abuse that power for their own ends. Furthermore, if you have corrupt officials in charge of handling aid money from abroad, then some of them will steal that money for themselves.

Bitcoin avoids these specific problems by having no centralised authority over its money supply, and by allowing people to receive money (e.g. aid) directly instead of having to rely on middlemen. It doesn't purport to solve all corruption per se.

4. Regarding how Bitcoin addresses privacy, I've added:

5. Bitcoin versus government accountability: if Bitcoin ruled the world, then governments wouldn't be able to simply print money in order to fund their unpopular ventures (as opposed to taxing their people and having to justify their expenditure). On an individual level, it's another reason why you can trust that your bitcoins won't be susceptible to inflation.

6. Losing your Bitcoin-wallet key: if you choose to take sole custody of your bitcoins (and it is a choice), then, yes, you are responsible for storing your key safely. The reason that your local bank can recover your account, on the other hand, is that they (not you) have custody of your savings.

That said, there is no reason why you couldn't make use of equivalent services in a Bitcoin economy. Bitcoin may not necessarily be user-friendly right now, but such relatively minor issues are unlikely to persist as the network undergoes development over the next few years – and it is this work that I encourage EA and other groups to support.

7. Whether Bitcoin can solve global issues better than fiat money: Bitcoin is just another form of money, so in theory, you can spend it on the same things that you would with fiat. The difference is that it appears to meet the fundamental requirements of sound money better than fiat does - in which case, the downstream benefits for issues such as poverty, climate change etc. would be huge.

8. "Could many of the issues you're highlighting be solved just by better functioning government?": I'm suggesting that Bitcoin is a way to achieve better-functioning government. Political/economic reform necessarily occurs at an institutional level.

Alex, I appreciate the thoughtful comment and all of the edits. I gave you an upvote, but I'm still far from convinced that this is worth EA's time and money. Most of what you've written so far as convinced me that poor, unstable governance is the ultimate pathology to treat, and Bitcoin is a potential ointment for (some) resultant symptoms. I know EAers work on improving election and democracy systems. A few more follow up thoughts on a few of your remarks:

Responding to (3) and (5): Sure, I see other issues that need to be worked out, for example, governments being able to tax fairly to pay for social goods such as schools and health care. I'm not convinced that the problems solved here outweigh those sorts of bad.

Responding to (6): How much of this is just fundamental though? Any sort of "customer service" will require a middle man, i.e. a brokerage or institution. It's not like we can retrofit the blockchain to have a "Forgot my Password" feature.

Responding to (7): But how much better? Are we better off into investing into anti-corruption projects or the democracy improvement ones?

1)

A sound monetary system is a crucial element of a healthy democracy.

It is not enough to address these problems simply with better governance. An institution is vulnerable to the extent that it relies on a small group to govern responsibly; the aim of political reform is instead to construct a system that cannot be hijacked by the incompetent or authoritarian actors that it will inevitably encounter. The most foolproof way of doing that is to make it impossible (e.g. by technological means) for any single entity to wield such power in the first place.

That’s precisely the approach that Bitcoin takes: instead of relying on political leaders to self-regulate, or counting on imperfect carrot-and-stick institutions to police good governance, Bitcoin ends the government monopoly on money altogether. Instead of hoping that people vote more rationally, Bitcoin appeals to people’s economic self-interest, offering a way out of their failing monetary systems.

As a result, Bitcoin is perhaps the only effective measure that could help to democratise societies that are hostile to reform. Members of Effective Altruism have offered many suggestions for strengthening democracy in nations where there is already some kind of avenue for popular change. But when it comes to authoritarian states where the ruling regimes show no interest in ceding power, we seem to have had no answers until now. Bitcoin is unusual in that it initiates institutional change from the ground up; governments can no more stop its proliferation than they can switch off the Internet. It is no accident that the nations most hostile to Bitcoin tend to be the most authoritarian ones.

2)

I don’t see how fairer taxation is made more challenging by Bitcoin. Decentralised money is not an aberration that humanity has never seen before – we’ve been there for most of human history (commodity money, such as gold, is fundamentally decentralised). Bitcoin is essentially trying to create a digital version of the classical gold standard that prevailed until 1914. Lending, taxation, and public works still happened in that era – if anything, it was a relatively peaceful and prosperous time. There is no reason to believe the same would not be possible when using Bitcoin. Government-enforced paper money, on the other hand, is an aberration, and one that has consistently resulted in rapid devaluation (as we are seeing right now).

3)

I've added this to the appendix: