Alix Peterson Zwane is CEO of the Global Innovation Fund, which invests in social innovations designed to improve the lives of the poorest people in the developing world. In this talk, she explores her current thinking around what it means to be an “effective altruist”and how this definition applies to the field of development finance. She proposes that the tools funders use have not kept pace with the rate of change in the world’s most “fragile” places — and she advocates for new approaches, such as supporting early-stage entrepreneurs.

A transcript of Alix’s talk, as well as a follow-up Q&A session with Nathan Labenz, is below. We have lightly edited it for clarity. You can also watch this talk on YouTube or read its transcript on effectivealtruism.org.

The Talk

Sometimes I think: Am I an effective altruist (EA)? What does that mean in terms of my job and my beliefs?

When I spoke at an EA conference in Prague, I talked about an answer to that question that has stuck with me: the concept of "hard-headed and soft-hearted." This is the mindset that unites us all as EAs, whether you work on international development, which is what I do, or in the other areas you're all engaged with during this conference.

In my current role, I partner with governments to think about effective development finance. I think the EA mindset translates into ensuring that philanthropy and government resources are spent as effectively as they can be. We want to use evidence to determine where we can achieve the greatest good at the least cost. And being an EA also leads us to realizing, at least in my field of international development, that we need to find new and innovative solutions to our existing challenges.

As I said, my visit to Prague made me excited to continue this conversation. There, I talked a little bit about what works in development — and how we know that. Today, I want to talk about engaging with the private sector from an EA perspective, and really advance my own thinking around this identity a little bit further.

I want to begin by saying that no matter how evidence-based our model is — and I’m as “randomista” as they come — our current approach to development finance will not solve the complex challenges that we face.

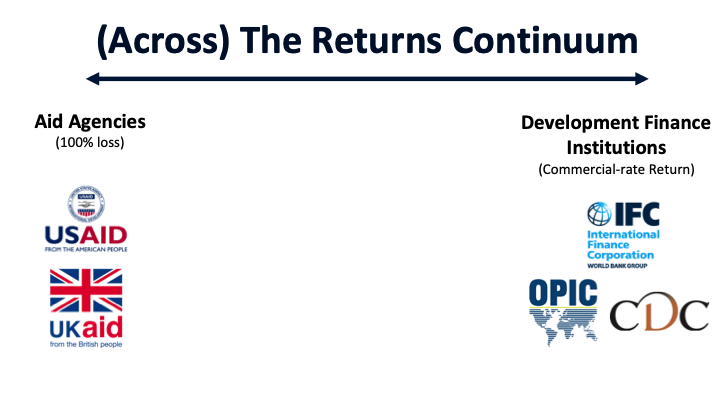

I'm going to use this picture [points to slide] to illustrate that in just a moment. When we think about foreign assistance or development assistance, we generally deploy grant-based aid on the one hand, and make investments in private companies, seeking essentially commercial rates of return, on the other. We don't, as a general rule, deploy all of the tools that are available in the development finance tool kit. We're not using scarce and valuable aid money to crowd in other capital to help solve the challenges that we face. And I'm going to argue in a few minutes that the world has changed sufficiently — in terms of where poverty is located and what poverty looks like — such that we need to begin to look through that tool kit and figure out other ways to support international development assistance.

This is particularly important in an area of increasing concern for developed or rich countries: fragile places. “Fragility” is sometimes used as a shorthand for post-conflict, but I'm using the term here in the more formal definition: places where norms, institutions, rights, and regulatory regimes are weak and, according to bankers, country risk is high. When country risk is high, the required risk-adjusted rate of return that private capital needs to invest is also extremely high. And that means flows of private capital are low.

If we are looking to build out the private sector — that engine of jobs and inclusive economic growth — we've got to figure out how to improve our ability to invest in those kinds of places. And one of the ways to start is to think about social return, in addition to financial rates of return. When you place increasing weight or value on social returns, the case for investment changes. That's the model that we've adopted at GIF [Global Innovation Fund]. We call ourselves a “social-returns-first investor.”

That's kind of an EA approach to supporting and engaging with the private sector, particularly in fragile places. It's how we help the governments that back us to direct their resources and take smart risks in ways that aren't typical with grant-based funding or with the kinds of instruments where we seek commercial rates of return.

I'm going to dig into that a little bit more. I want to tell one quick story to help us do that. This is the story of Lively Minds.

Lively Minds is a grantee of GIF working in northern Ghana. Northern Ghana is a pretty fragile place, and women and girls fare especially poorly there. Just 44% of young women living in that region are literate.

Lively Minds works with these young women by involving community mothers in the delivery of kindergarten classes for kids ages four to six, and there's evidence from a randomized controlled trial suggesting that this not only improves cognitive outcomes for those kids, but also reduces teacher absenteeism. Interestingly, it empowers these local, often illiterate women. I've heard the stories firsthand myself of mothers who — and yes, this is anecdotal, but it's pretty compelling to hear — tell stories about how being engaged in the education of their children has made their self-esteem rise and their level of empowerment in the household and community change.

But Lively Minds is a social enterprise, registered as a nonprofit. We've got a very difficult road to scale. The right path to scale is some kind of public-private partnership with the government of Ghana or perhaps some kind of franchise model, but you need buyers with not only the willingness to pay, but the ability to pay. And it's pretty hard to imagine that the returns are there on the financial side that would make this interesting from a traditional investor’s perspective.

In terms of the social impact, the case for supporting this is strong. In Accra, the capital of Ghana, when I was there visiting Lively Minds, I stopped by a place called the Impact Hub. This is an incubator, founded by an amazing guy called Will Senyo, and it feels just like the WeWork where my office is in London. These are innovative entrepreneurs. They're trying to tackle social problems by finding ways of bringing global capital to Ghana to make money, generate jobs, and change the world. That probably sounds like some of you who are in this room. But growing these businesses is going to be a very long row to hoe if we rely on the Ghanaian capital markets. I asked my research assistant to quickly check what the average rate is if I want a loan from the Bank of Ghana, when I was getting ready to come here. And last week it was 34.5%. The cost of capital is high, and there's not a flourishing market of local venture capitalists or patient investors.

Ghana is not alone as a place that has both this [points to photo] and Will Senyo’s incubator. Increasingly, that's what the world looks like, and that means we need to think about supporting development differently. Neither Lively Minds nor the Impact Hub is a traditional recipient of aid money from DFID [UK Department for International Development] or USAID [US Agency for International Development]. And increasingly, it might be that to help the clients and women who work with Lively Minds, you could take the path of supporting one of those firms or the Impact Hub itself. We've got to think about how to do things differently. We want this kind of impact from our development assistance. We've got to think about how to do that in a changing world.

I'll show a few slides about what I keep saying about this changing world.

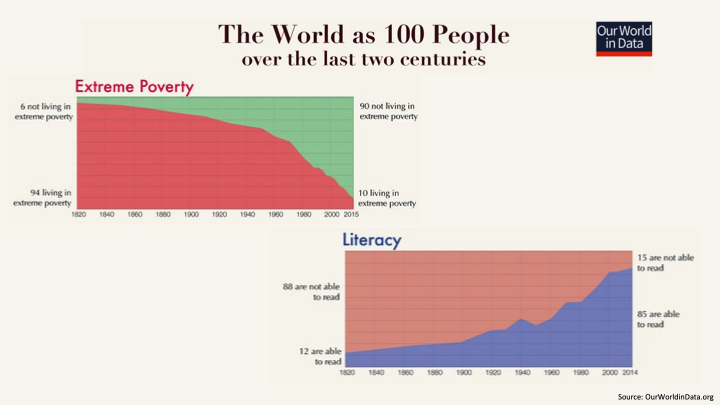

As you all know, we have made amazing progress in reducing extreme poverty and increasing literacy around the world. Hundreds of millions of people's lives have improved over a relatively short time horizon.

Increasingly, where poverty does exist, it's in these fragile places. Poverty is concentrated in fragile pockets of middle-income countries. And by 2030, something like 80% of the extreme poor are going to live in fragile places. This complicates thinking about how to support the private sector as an engine of growth and development. Development finance institutions — CDC [Group], OPIC [Overseas Private Investment Corporation], those kinds of entities — in 2016 sent only 10.6% of their funding to the world's most fragile places. And that's the DFIs. Private foreign direct investment is even smaller than that.

So, as this development landscape has evolved, have the tools in our toolbox evolved? Not as much as they probably need to. I think that most of us, when we consider development assistance, think more about DFID than we do about CDC (in a UK context). Same for USAID in the United States. And DFID and USAID spent $30 billion on official development assistance in 2016. That is important, highly valuable money that supports global public goods, responds to disease outbreaks and humanitarian disasters, and improves the public health and security of poor people. And I am by no means arguing that this kind of ODA funding should be reduced.

Development finance institutions (DFIs) — CDC, OPIC and those kinds of places — support infrastructure and the vibrant private sector by converting public money into private investment in emerging markets, and making some real money while they do it. OPIC brought in $358 million more than it spent in 2016. The IFC (International Finance Corporation), which is part of the World Bank Group, has an annual surplus that averages around $600 million. DFIs spend most of their money in non-fragile places — about 26% of their money goes to upper-middle-income countries, and something like 8% to the poorest countries.

We have ODA for fragile places. We have DFI money going mostly to middle-income places. And both of those are critical. But there’s a gap. I call it the “pioneer gap” — a term that I think came from the Omidyar Network. Traditional aid agencies and DFIs have really not been good at taking risk in this early stage and supporting entrepreneurs with innovative ventures, who may have been able to scramble together that first round of funding to test out an idea and see if it has merit. But pioneers need more money to validate their ideas and transition their innovation to scalable, bankable projects. And this pioneer gap can quickly turn into a chasm for entrepreneurs who are trying to build the market into which they're selling.

That's because of what economists call a market failure, plus some externalities. The externality here is that success for these pioneers benefits many companies, not the individual firm alone. But those benefits are hard to quantify, and they're hard to privately capture. So how can you demonstrate that you're investment-ready to funders that are interested solely in private financial returns?

If we can figure out smart ways to accept concessional financial returns and trade for outside social value, then funding to bridge the pioneer gap is a new tool to add to the development toolkit. It can augment the range of things that we're able to offer to support and improve the lives of poor people living in fragile places. Impact investors and venture philanthropists have been thinking about doing this for some time now, but those pools of capital will be most powerful if we can complement their work with some government budget commitments.

I'll illustrate how this can work in practice by introducing you to an entrepreneur by the name of Kola Masha. When Kola founded his company, he had a vision of not just a profitable business, but one that would improve the lives of smallholder farmers in northern Nigeria. Babban Gona provides end-to-end assistance to farmers so that they get their crops to market and get the best price at the best time. To make that happen in a very difficult context, Kola needed capital that was early-stage, flexible, and patient. For his early-stage capital, he got his first round of funding mostly in the form of grants from a small Bay Area family foundation. This was well before any of this was commercially viable, but the grant money helped Kola demonstrate that he could execute and refine in the earliest stages of his business model.

Second, Kola needed flexible capital, because Babban Gona provides credit to the farmers in their network throughout the harvest season and has large capital requirements to operate. International commercial capital, including from the DFIs, is generally dollar-denominated. And Kola is operating in a context in which currency risk is significant. So at GIF, we made our investment in Babban Gona denominated in the local currency. We took a subordinate position and accepted currency risk in the debt that we provided to Babban Gona, and that allowed other, more risk-averse, dollar-based funders to join in a senior position. That meant that Kola had access to more capital, more quickly, than he otherwise would have if a funder like GIF had not been able to take on that kind of currency risk.

Kola also needs patient capital. What he's trying to do is hard. Returns, while they might be attractive, are coming over a relatively long time horizon. Many impact investors have closed-end funds. That means they are looking to exit, and earn returns for their limited partners, in a relatively short period of time. That can make even the most socially-minded impact investment funds hard to match up with business models like the one that Kola is developing. GIF has been set up deliberately as an evergreen structure. We're not going to face incentives to encourage Kola to go upmarket with his clientele to quickly make his firm more attractive to other investors. We need more evergreen structures like that to support entrepreneurs like Kola.

Looking to the future, if Babban Gona works, it can support hundreds of thousands of jobs in northern Nigeria, and not just improve livelihoods, but put a small dent in the root causes of the long-simmering conflict with Boko Haram.

Of course, this kind of approach is not without its challenges and risks. Using public money to support private entrepreneurs causes us to worry about distorting markets or crowding out private finance, when we really are interested in crowding it in. There are a couple of lessons that GIF has learned in mitigating these concerns.

First, seek your investments in contexts in which you understand why social returns might not just be large, but large relative to private returns. That means you're looking for places where there are market failures. Often, this is because there's a missing market due to high costs of market discovery. Innovating in new markets might require a long process of testing and experimenting to find the right product-market fit and discover the right cost structure. A firm's ability to capture the returns of that investment and do all of that learning is typically limited. With that kind of market failure, you can be more certain that you're actually crowding in other capital rather than crowding it out.

Second, you have to measure impact rigorously and discipline yourself to use evidence of impact as a positive screen on your investment decision-making. You claim you want to find those places where social return exceeds financial return. You owe it to your own investors or yourself to really test that proposition by investing in measurement. GIF has an approach to this that we call practical impact, which is lean and pretty flexible. We use the best available data and evidence to guide our investment decision-making, and then we update our assessment and our measure of the social value of our investments — the same way that a venture capitalist assesses the valuation on the financial side of their portfolio on a regular basis.

Of course, your concessionality — the subordinate position, remember, that we just took in the Babban Gona case — means you are effectively subsidizing other investors. You should understand the risk you’re bearing, and the risk that is difficult for the other investors to bear, and why that’s an appropriate use of your capital. And this is that “hard heads, soft hearts” approach to thinking about how to engage.

And finally, meet the entrepreneur where they are on their journey. We talked about flexibility: being willing to come in early, be patient, and use different instruments — including equity, debt, and convertible notes.

I will finish up here today by thanking you again for the opportunity to be here and talk about these topics. There are some interesting new developments in this space that I think are worth keeping an eye on. I mentioned that Omidyar Network and other philanthropic institutions have lit the path, and not only is GIF now engaging in this kind of work, but reforms are allowing institutions like the DFI and OPEC to engage more in the “missing middle,” if you will. Keep an eye on the IDA’s [International Development Association’s] private-sector window at the World Bank. And I urge you to seek opportunities to take smart risk in pursuit of social value with that “hard head and soft heart” mindset. Also, keep the “pioneer gap” in mind, whatever that might mean for you and where you are as an investor and an EA. Take some smart bets for social change. That's the EA approach to impact investing.

Nathan: I love the concept of making an investment in a junior position and the general concept of crowding out, versus crowding in, capital. Could you talk a little bit more about how that dynamic plays out? Who are these other investors? What does your relationship with them end up being as these deals come together?

Alix: Sticking with the Babban Gona example, we weren't alone in taking on this subordinate position. We did that along with a couple of other impact investors. And then the senior position would be taken by folks like OPEC or the IFC — so, some of these development finance institutions. And the ultimate vision, I think, which would be really great, is if, over time, you de-risk the model enough so that it's funded in local capital markets and in Nigeria. In other words, all of the expenses and revenues are in local currency. They do have a flourishing pension fund infrastructure there. That would be a real prize.

One thing that's interesting about another role that GIF was able to play in that area: We provided the on-the-ground due diligence that many investors didn't feel like they had the capacity and the capability to dig into. We agreed to do that work as a public good that could be shared with the other impact investors who shared the subordinate position in our consortium. That's another way of thinking about how we're set up to tolerate this risk in a way that others aren’t. And the more you think about who can take on different kinds of risks, the better you can put together these interesting coalitions.

So, as a general rule, we invest with impact investors, DFIs, some true venture funds, local venture funds, and sometimes with private equity. We are able to be in different positions with different partners.

Nathan: How does your organization decide which organizations they intend to invest in? And can you give some examples of other organizations that you have already invested in?

Alix: GIF was very deliberately set up to support innovation, and open innovation is at the heart of what we do. I didn't emphasize that so much in my talk here, but that's very much core to our identity. Part of how we interpret that is by saying, "We don't have a sectoral focus. We don't have a geographic focus. We're really interested in accelerating evidence-based innovation that improves the lives of people who live on under $5 a day."

On the one hand, that’s great. On the other hand, it's also like, "Okay, my goodness, where do you start?" We work really closely with networks of other co-investors, with accelerators and incubators, and really try to see what their entrepreneurs are excited about. We focus on backing an entrepreneur as much as we're backing an innovation.

That's sort of a bottom-up approach as opposed to a top-down or strategy-driven approach, which oftentimes many strategic philanthropies elect to take when investing their money. We've deliberately complemented that with something more bottom-up.

To describe a couple of deals: Let me tell you about something I'm currently excited about. There's a real interest in international development in figuring out innovative ways that we can help governments increase their own tax revenues. The jargon for that is “domestic resource mobilization.” It’s attractive because, when you start thinking about the journey to self-reliance and graduating from international assistance, tax revenue is hugely empowering to local decision-makers and local actors. They can spend the money on their priorities [because they collected it themselves].

What you need to do to move the needle on domestic resource mobilization is help firms formalize, or better yet, start out in the formal sector and never spend time in the informal sector. But in many contexts that's conceptually hard, even if the spirit is willing; paying your taxes as a small business in a place like Indonesia is daunting. It's a clunky, paper-based thing.

We've recently taken an equity stake in a company called OnlinePajak. It's like Quicken tax software but for SMEs [subject-matter experts] and with a mobile app-based approach to it that's free to firms. OnlinePajak makes money by selling you other services. They’re like, "I can do your accounts payable and receivables, even some of your HR stuff, once you've put all of your data into the OnlinePajak system."

What was interesting for GIF is that the other lead investor in this round was a private equity firm that obviously had way deeper pockets than we do. At first we said to ourselves, "Great — domestic resource mobilization. I love it, but what else are we really bringing to the table? Because we're not bringing money to the table. The weight of this private equity firm clearly is."

But in conversation with the firm, we realized we could be valuable to them in unique ways. First of all, one of our partners is the Australian government, and the Australian government is working with the tax authorities in Indonesia to improve regulatory reform efforts there. We were able to facilitate conversations because of our relationship with the government of Australia that could help embed the OnlinePajak approach into larger tax conversations being had there.

Secondly, we are able to match them up with the Behavioural Insights Team — to whom we had previously given a grant — to do some nudges around getting people to pay their taxes. And now, we're able to think about nudges to use OnlinePajak and how to think about marrying the technology and the behavioral economics. Maybe the whole is greater than the sum of the parts. We were able to say, "Actually, I do understand why we're taking a seat at this table alongside the deep pockets of this private equity firm. We're bringing something different and valuable and unique.”

I think that’s a great example of how our being backed by governments is a feature, not a bug. And our wonky interest in evidence and economics can be valuable for the firms we partner with, too.

Nathan: Awesome. We'll just end with one more question, which probably has a relatively short answer: How would you recommend that someone get into your field? Would they start with a more traditional finance background, or something else?

Alix: I think understanding markets, local contexts, and the economics of the challenges that we're thinking about is just as important, if not more important, than being a financial wizard. We work very collaboratively at GIF with local people who have deep experience in scaling up housing in developing countries. Economists on our analytics team and our finance folks all work closely together.

The reason we were excited about OnlinePajak is because of its contribution to growth and development. And many impact investors might say, "Is that an impact investment? You can't take a picture of the woman farmer that you're helping." But that's okay. It's exactly the richness of those conversations that help us do exciting deals. I think it's helpful to have not just a traditional MBA, but something a little bit more magical than that.