Abstract

Several major technology companies have announced plans to operate AI data centers in orbit. Elon Musk recently claimed: “the lowest-cost place to put AI will be space […] within two years, maybe three.” If a meaningful fraction of new AI compute really is placed in space within a few years, that would be a fairly big deal for AI governance and strategy. Here we try to disentangle the hype from reality and provide a sober assessment of the technical and economic feasibility of orbital data centers (ODCs).

The main case for ODCs is the cost of energy: space solar panels in the right orbits receive more constant and intense sunlight compared to Earth. Moreover, ODCs don’t currently face the same permitting and regulatory delays as on Earth, cause fewer ongoing environmental harms compared to grid or onsite natural gas-powered data centers, and may be more secure against data exfiltration. We find that the cost-competitiveness case for ODCs depends almost entirely on Starship achieving reusability comparable with what SpaceX achieved with Falcon: space-based solar reaches cost parity with present-day off-grid terrestrial power continuously at roughly $250/kg to orbit, and becomes cheaper than any current terrestrial energy source at around $50/kg, from the present-day launch cost of roughly $1,500/kg. Radiative cooling, often cited as a fatal obstacle, appears surprisingly manageable — potentially even cheaper than on Earth. However, ODCs may require substantial (perhaps ~38%) extra non-compute hardware (like solar, racks, and cooling) over 5 years to compensate for their inability to swap out failed chips, and inter-satellite bandwidth limitations likely confine ODCs to inference workloads, at least early on.

Assuming no transformative AI, but continued demand for data center buildout, we estimate that ODCs are unlikely to represent a meaningful share of compute before 2030, but become cost-competitive with present-day terrestrial data centers within 3–5 years if Starship development stays on track.

Read on the Forethought website here

Introduction & Takeaways

Some of the world’s largest technology companies continue racing for compute. If progress continues, demand for data centers may more than double by 2030. Increasingly, though, new data center capacity is bottlenecked by multi-year queues to connect to the power grid.

The result has been a scramble for workarounds. Leading AI labs have increasingly adopted a “Bring Your Own Generation” model to source power, deploying onsite gas turbines and engines to bypass grid bottlenecks. xAI, for example, reportedly installed hundreds of megawatts of onsite gas generation in Memphis to accelerate deployment, and OpenAI and Oracle have placed large turbine orders for new Texas campuses.

Some argue that energy will become the binding constraint on AI progress, given grid interconnection delays as gas turbines are themselves facing multi-year manufacturing backlogs. But the constraint does not appear fundamentally binding (as Epoch notes): turbine manufacture may expand to meet more demand and companies could go off-grid using combinations of gas, solar, and batteries, scaling power in parallel with compute, albeit at a cost premium. This raises a natural question: if you’re going off-grid anyway, then what’s the best way to get power and where is the best place to put your data center?

Some think the answer will be in orbit. In November 2025, Google announced Project Suncatcher, a plan to put TPU-equipped satellites in dawn-dusk sun-synchronous orbit. In early 2026, SpaceX filed with the FCC for authorization to launch and operate a constellation of up to one million data center satellites. Other entrants include Blue Origin, Ramon.Space and startups like Starcloud, and Aetherflux while China’s Three-Body Computing Constellation has launched 12 operational satellites and run Alibaba’s Qwen3 model in orbit. Recently, at GTC in March 2026, NVIDIA announced the Space-1 Vera Rubin Module, meant to be a dedicated space-rated GPU platform.

At first glance, it seems very unlikely that any meaningful fraction (say, >10%) of additional data center capacity will be placed in space in the next few years. But if the companies betting on space are right, that would be a fairly big deal, and it could change the landscape of AI governance. For example, terrestrial data centers are subject to national and regional regulations, whereas AI developers could potentially exploit jurisdictional ambiguities around compute in space. Also, the path to low-cost orbital compute likely routes through a single launch company, SpaceX, which also now operates a frontier AI lab since its acquisition of xAI. And that might raise concerns around concentration of power.

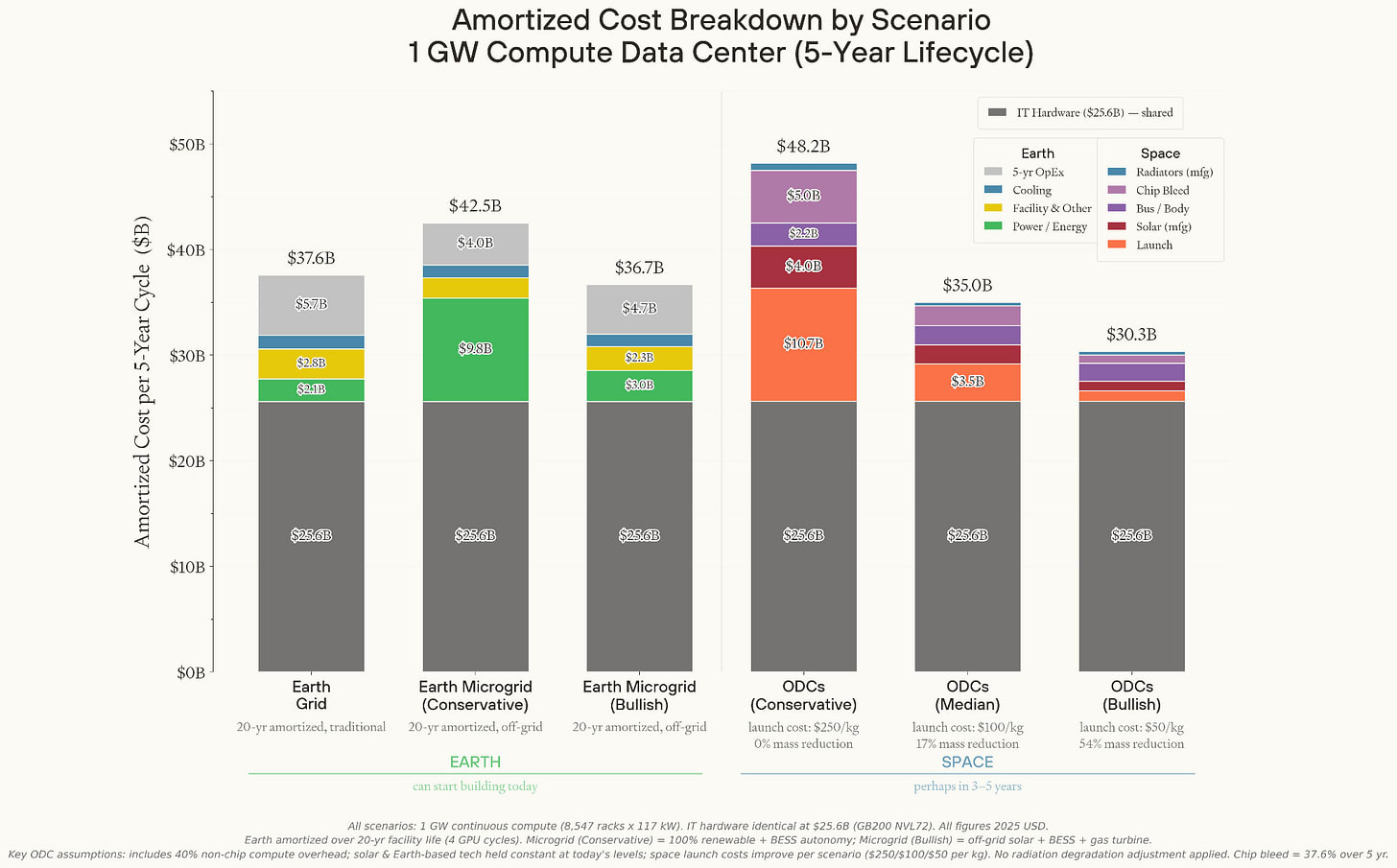

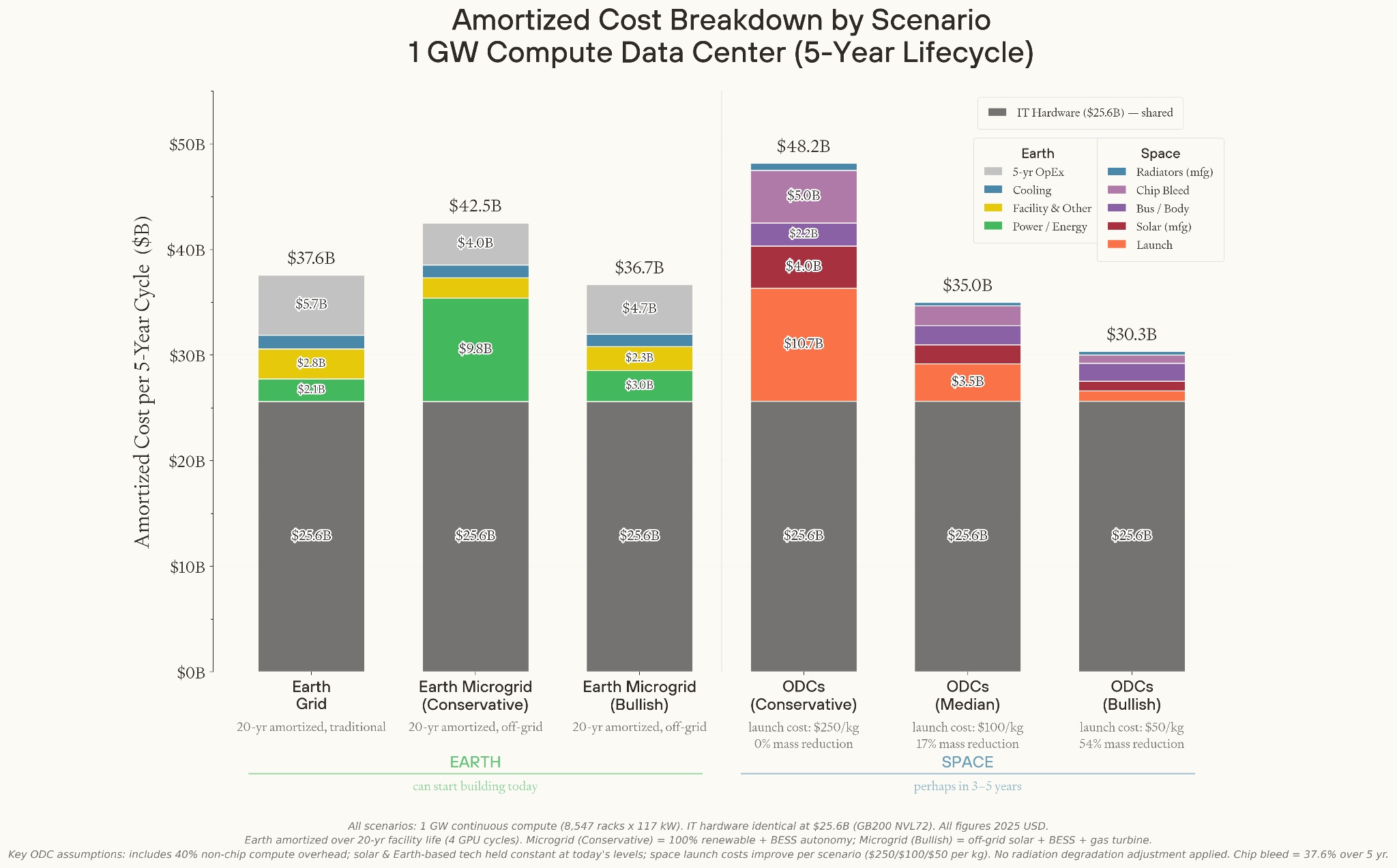

We’ve been looking into the technical and economic viability of orbital data centers (ODCs). Our core model gives estimates for the total cost of Earth and space-based data centers across several scenarios.

Cost breakdown for three Earth-based and three space-based scenarios building out 1 GW of compute. As best we can determine, orbital data centers could become cost competitive with a bullish terrestrial buildout if launch cost reaches around $100/kg given modest reductions to server and cooling system mass, while a bullish case for orbital data centers with substantial mass reductions and launch at $50/kg may offer cost savings.

The report focuses on three questions. First, what is the basic economic case for a meaningful fraction of AI compute being placed in space? Second, the most obvious physical blocker: can you cheaply cool a data center in orbit? Third: how fast could the shift to space data centers happen, how soon, and what would have to go right?

Here is our provisional assessment:

- SpaceX’s Starship is the only vehicle currently on track to deliver the launch costs and cadence that meaningfully scaling orbital data centers would require. Competitors are years behind, making SpaceX’s Starship the only near-term path to large-scale orbital compute. SpaceX aims to complete Starship development by late 2026, with several necessary milestones still ahead. If development stays roughly on track, Starship could plausibly hit the cost and cadence required to scale meaningful orbital compute within 3–5 years. However, chip production may become the limiting factor by this point, rather than launch capacity.

- The cooling problem is more tractable than commonly assumed. Passive radiators using selective coatings and lightweight carbon fibre panels could achieve ~163–346 W/kg at system level, a 13-28× improvement over ISS-era radiators (~13 W/kg). No radiator at these performance levels has been deployed at the scale an orbital data center would require, but prototype high-conductivity carbon composite panels have demonstrated the material properties required. At these performance levels, thermal hardware is 2-5% of total data center cost, and actually less than what terrestrial data centers spend on cooling over a comparable lifecycle.

- If launch costs fall enough, the unit economics could favor space. Solar panels in dawn-dusk sun-synchronous orbit produce roughly 3–5× the energy of the same panel at a good terrestrial site. Space-based solar becomes cheaper than the best off-grid terrestrial installations once launch costs drop below roughly $250/kg using Starlink-like solar arrays. At a launch cost of $50/kg (corresponding perhaps, to a Starship with full reuse as reliable as Falcon), space solar could fall to between $25–45/MWh, making it cheaper than any current terrestrial option available today. Beyond the symmetric cost of chips, launch cost is the dominant line item for ODCs while power and op-ex dominate terrestrial costs but would be near zero in space.

- The inability to do maintenance would be a large cost. Chips often fail and are swapped out in today’s data centers but a dead chip in an ODC would remain dead, wasting the parts of the supporting infrastructure (power, cooling) and diminishing overall compute. We model this below as a 9% annual bleed causing about 40% overbuy of launch and non-chip hardware over the data center’s lifetime. Below $100/kg launch cost this might net out against other savings from ODCs but this is a significant uncertainty since the actual rates of chip failure for ODCs could be higher or lower.

- All-things-considered we think that, absent transformative AI, orbital data centers probably won’t make up a meaningful fraction of compute before 2030, but it’s credible that space could house much or even the majority of compute buildout throughout the 2030s.

Read the full report on the Forethought website: Will We Really Put Data Centers in Space?

I'm glad to see this rigorous analysis!

I was skeptical of the cooling being cheaper in space. It is true that you can radiate to a much colder temperature in space, about -60°C equivalent. It does look like space cooling would be cheaper with your future launch costs for your constellation model. However, for your modular station model, you would need around 1 m diameter pipes to start, which would weigh a lot and pose a large single source of failure. Also, you would have to pump long distances, increasing the pump mass and energy use.

I think inference would be challenging because the satellite is in view for only a few minutes. I guess most queries take less time than this, but would you keep handing off the session memory?

This is much more reasonable than people claiming that going off grid is cheaper than grid electricity with the same reliability. Still, you note that this capacity factor is reasonable for the desert, but typically there is around a two times seasonal variation. Since 80 hours of storage can't handle that, you would need to oversize your PV more. But it wouldn't change the results that much (~10%). And the gas turbine in your Baseline B solves this seasonal problem.

If you want 80 hours of storage for 100 GW, that is 8 TWh, which is years worth of current production, so I think you'd have to pay a premium.

For the longwave radiation coming from the earth, you would get ε absorption, not α absorption. So the equation should be:

P_net = 2εσT⁴ − αS − αF(Al × S) − εF(σT_earth⁴)

Also, the view factor to the Earth is 0.25 for one side of the radiator, but you are counting both sides for the emission, so I think the view factor should be 0.5.

So then at 20°C: emitted 770 W/m², absorbed 248 W/m², net rejected 522 W/m² (not 633 W/m²).

Also note that if your fluid temp is 20°C, the radiator will be lower average temp because of conductive thermal gradient. But with 1 mm of high-modulus pitch-based carbon fibre reinforced polymer, it doesn't look like too much of a loss.

Footnote 17 seems to end abruptly: "The scenarios in a bit more detail are as follows:"

Hey David, thanks for this excellent comment.

Re: cooling skepticism, actually this has been helpful. On review I think the net rejection will be greater than 633 W/m2. You’re right, we get absorption = ε for longwave radiation from Earth (Kirchhoff would not be pleased).

On view factor, hmm I think this will just vary over the orbital band. Computing the analytic per-face as F = (1/π)[θE − ½sin(2θE)] with sin(θE) = R⊕/(R⊕+h) I get:

Altitude

F per face

F total

550 km

0.258

0.515

1000 km

0.194

0.388

2000 km

0.118

0.236

Maybe we should go worst case and also initial ODCs would prefer to be on the low end of altitude for as long as slots are available (lower cost to orbit, less radiation) You do I think want to go high enough to avoid occasional shading in dawn-dusk-SSO so perhaps ~675km and up. If we correct the absorptivity for Earth IR and take the low end view factor, I get your 522 W/m2. That looks like a ~1% increase in total cost for ODCs if you’re right.

While checking this though it occurs to me you should be able to be have the radiators edge on to the sun while still radiating from both sides, something like this:

Basically a Starlink v3 with panels at 90 degree pivots. Then with shading from direct sunlight I think I get 650 W/m2 for 675 km altitude, F = 0.473, so an improvement on radiator performance overall. I’ll have to think about this a bit more and potentially update the appendix. Certainly we can fix the erroneous use of α in the 3rd term.

Re: inference, not my area of expertise and I don’t think the computer architecture totally decided but from looking into it I think it looks like you’d only be handing off the query and response. The routing should be the same as for traditional satellites so this problem is already ~solved (though you may need to scale the satellite mesh as demand/traffic increase). The orbital compute is in a polar orbit so typically not overhead. The trip in a kind of worst case scenario might look something like this:

For example I think for a 100 GB workload through a 100 Gbps optical ground station, total time is ~8 seconds serialization/transfer, essentially the same ~8 seconds as terrestrial on 100 Gbps direct connect, plus something like 175 ms of constellation overhead.

Re: terrestrial solar and battery. Good points: these make terrestrial microgrids look a good bit worse. For solar on Earth in addition to the seasonality we’re also assuming some of the best solar sites in the world so this should be fairly bullish for terrestrial data centers. We didn’t spot any fundamental blockers to scaling microgrids through some combo of solar overbuy + battery and gas but prices may be at a premium either for turbines or for batteries as you say. In some sense it seems like the data center buildout may have hyperscalers acting like water flowing down hill, pivoting into whichever buildout channel offers least resistance at the moment. Similarly if ODCs start going up en masse there could be lower lying supply chain issues that emerge. The most biting constraint of all is probably chips and memory.

I dug in a little more, and I think your Earth cooling estimate is high at $2.5–3.0B/GW with water chillers. An NREL study was more like $0.7B/GW with water chillers. Also, we may be able to dispense with the water chiller (as you have assumed in space), and then it could be even cheaper. So I doubt it's actually going to be cheaper to cool in space. However, your point that cooling in space doesn't wreck the economics still stands.

I'm glad it was helpful!

I was using 550 km, so I agree that higher up, you would have more net radiation leaving the radiator.

As for your bent configuration, that is creative to avoid the sun incidence. However, then you would have radiation from the solar panels to the radiator, and since the solar panels will be warmer than the Earth, I think it will work out worse overall.

Incomplete?

Your other points make sense.

Seems to be a formatting error and it's supposed to be in the main text, referencing the table.