Comments

137

Main Author: Ren Springlea

This is a summary research report by Animal Ask, investigating whether a meat tax campaign could be a recommended intervention for improving the lives of factory farmed animals

We would like to thank the experts we looked to for guidance in this report.

Animal Ask has been founded with the express aim to optimise and prioritise future asks to assist animal advocacy organisations in their efforts to reduce farmed animal suffering. We provide organisations with in-depth research narrowly targeted at key decisions between different animal asks, supporting organisations, individual activists, policymakers and donors so that they may do more good in the long-term.

If you would prefer to view this report in PDF form, you can do so via our website or via this link.

A meat tax is one policy that can reduce meat consumption. This policy has some key advantages: there is strong economic evidence that such a tax would reduce meat consumption while, depending on the type of meat tax, a campaign could also take advantage of the momentum provided by the environmental and health movements.

However, a meat tax also suffers from a substantial risk. As the price of meat increases, consumers may switch from eating beef to instead eating chicken and fish. This could cause an overall increase in the total number of animals killed for food each year. This risk is highly plausible, considering that environmental- and health-motivated policies would likely place higher taxes on beef than chicken or fish. This risk is also difficult to predict in advance, even if the details of the meat tax policy were known. Furthermore, public support for a meat tax is very low.

For these reasons, we do not recommend a meat tax as a campaign for animal advocacy organisations. Instead, we encourage organisations to choose an alternative campaign that has a more robust and favourable base of evidence.

Motivated to address the immense suffering of animals in the agriculture industry, many animal advocacy organisations seek to campaign for government policies to reduce meat consumption. One policy that has been proposed by these organisations is a meat tax. A meat tax would involve a government levying a tax on the purchase of some or all animal-derived food products, including meat, dairy, and eggs (Arvidsson, 2016; de Graad, 2020). A meat tax is currently an area of active campaigning by PETA[1]. It has also been strongly recommended by the book Meatonomics (Simon, 2013) and there appears to be support for it among other animal advocacy organisations (Simmonds and Vallgårda, 2021). A campaign for a meat tax would take advantage of the momentum provided by these environmental and health organisations who have proposed meat taxes (Briggs et al., 2016; Springmann, Mason-D’Croz, et al., 2018; FAIRR, 2020). A meat tax could bring benefits to farmed animals, but it also carries some serious risks. We will discuss these benefits and risks in detail below.

Note that this document focuses on the potential for a meat tax in the UK. Most of the public discussions and academic analyses of meat taxes have taken place in Western Europe, and animal advocacy organisations in the UK have expressed interest in campaigning for a meat tax. However, many of our findings will be readily applicable to other countries.

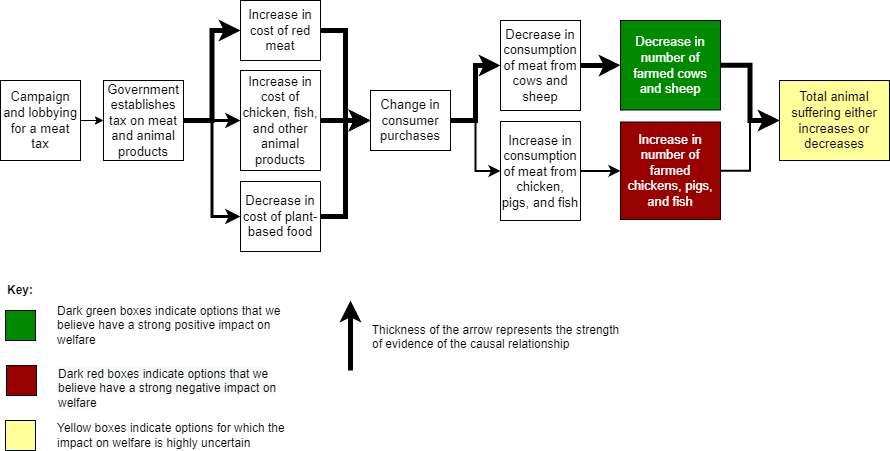

The effects of a meat tax on animal suffering are visualised in the following flowchart. By encouraging the government to establish a tax on meat and animal products, this campaign would increase the cost of these products. Following standard economic theory, an increase in cost would cause a decrease in the demand for meat, and consequently its consumption. However, a greater increase in cost for beef or red meat (which would occur for an emissions- or health-focused tax) would also cause consumers to substitute away from beef or red meat towards cheaper meat (e.g. chicken, fish). This means that the consumption of some types of meat would decrease, but the consumption of others might increase. Therefore, whilst a meat tax is likely to decrease the number of farmed cows and sheep, this may be offset by a larger increase in the number of farmed chickens, pigs, and fish. For this reason, it is highly uncertain whether a meat tax would, overall, benefit or harm animals. This possibility is discussed in detail throughout this report.

The following flowchart visualises this theory of change, based on the economic evidence and modelling studies discussed in this report.

There is strong evidence from economic theory and modelling studies that a meat tax could reduce the consumption of at least some types of meat and animal products. However, note that there is also strong evidence that a meat tax could increase the consumption of other types of meat. This concern is discussed in detail in the ‘Small Animal Replacement Problem’ section below. Empirical studies and historical taxes may provide evidence to support the feasibility of a meat tax, although this evidence appears weaker.

The economic theory of a meat tax is straightforward. A meat tax is essentially a tax levied on the purchase of meat and other animal products. Economic theory predicts that a tax on meat would cause the price of meat to increase. This price increase would then trigger a decrease in the demand, and thus consumption, of meat (Arvidsson, 2016). Literature reviews have found that taxes on food decrease the consumption of the foods targeted (Thow, Downs and Jan, 2014; Sacks, Kwon and Backholer, 2021). The magnitude of this decrease depends on price elasticities. As an illustrative example, the own-price elasticity of beef is often calculated to be within an approximate range of -1.3 to -0.5 (e.g., Wirsenius, Hedenus and Mohlin, 2011; Abadie et al., 2016). This would suggest that a 1% increase in the price of beef would cause the consumption of beef to decrease by between 0.5% and 1.3%.

In reality, the true decrease in consumption of any product also depends on the prices of other products. To paint a more comprehensive picture of the effects of a meat tax, we can turn to modelling studies. We performed a literature review [2] to identify studies that modelled the effects of a meat tax. Specifically, we included studies that predicted the effects of a meat tax on the percentage change of consumption of at least one type of meat. Our literature review identified 19 such studies (see Appendix).

Crucially, all of these studies estimated that a tax results in a decrease in the consumption of at least some meats and animal products. This provides very strong evidence that a meat tax is capable of reducing the consumption of at least some meat and animal products. There is also strong evidence that a meat tax can increase the consumption of particular food groups - this was common for plant-based foods, but was also observed in some studies for poultry and fish (see ‘Small Animal Replacement Problem’ below). Most of the studies calculated a tax based on greenhouse gas emissions, with health-based taxes forming a minority.

There are six studies that we have included in our own detailed analysis (see Effectiveness Analysis, below). Briggs et al. (2013) modelled the effects of a greenhouse gas emissions tax on the consumption of many meats, non-meat foods, and drinks in the UK. Briggs et al. (2016) performed a very similar analysis, with an updated dataset and additional scenarios. Kehlbacher et al. (2016) considered a similar collection of products in their study on an emissions tax in the UK. Wirsenius et al. (2011) and Jansson and Säll (2018) both focused on the EU, modelling the effects of an emissions tax on meat and animal products. Finally, Revoredo-Giha et al. (2018) concentrated on the UK, considering scenarios ranging from a tax only on beef and veal to a tax on all food products.

The remaining studies have not been included in our detailed analysis either due to a geographic focus outside the UK or a choice of food groups different to the groups we consider in our analysis. (Chalmers et al. (2016) focused on Scotland, but included too few food groups for us to reliably adopt the results.) It is interesting to note that, aside from two global studies and one study on Australia, every study focused on either the EU or a country in Europe. This academic interest in Europe seems to be reflected in the concentration of political and public discussion on meat taxes in Europe.

Real-world empirical data on the effects of meat taxes on meat consumption is extremely limited. This is because no country has yet implemented a meat tax (see ‘Meat Taxes Outside the UK’ below).

However, there is empirical data on the effects of the saturated fat tax in Denmark. This tax increased the price of some meat products in 2011 and 2012. Jensen et al. (2016) performed an empirical analysis of the Danish saturated fat tax, limiting their analysis to minced beef, regular cream, and sour cream. High-fat minced beef was subject to a tax of 16% and saw a decrease in consumption of around 13%. Meanwhile, high-fat regular cream was subject to a tax of 14% and saw a decrease in consumption of around 12%. Finally, high-fat sour cream was subject to a tax of 13% and saw a decrease in consumption of around 9%. It is clear, therefore, that the saturated fat tax affected the price of multiple categories of meat products, and it may be possible for a future empirical study to measure the effects on the consumption of different groups of animals. However, due to the limited data available, the studies that have measured the effect of this tax have not distinguished between different groups of animals (Jensen et al., 2016; Smed et al., 2016).

There is also empirical data produced by experimental studies conducted in laboratories and cafeterias. In a review study for the animal advocacy movement, Harris (2020) found that there is strong evidence that a tax can change behaviour. Likewise, a review by Epstein et al. (2012) concluded that price interventions can change purchasing behaviour in laboratory studies. A conflicting piece of evidence is the cafeteria study by Garnett et al. (2021). In this study, a 10% decrease in price in vegetarian meals and an 8% increase in price in meat-containing meals caused an increase in the purchase of vegetarian meals but no effect on the purchase of meat-containing meals. However, the study setting was a university cafeteria where meals are usually purchased using university cards rather than the students' own money, plausibly affecting purchase decisions. This means that the ability to generalise the results of this study to the general population is limited.

Currently, no country has implemented a meat tax [3] (Mosca, 2020). However, multiple countries have held political and public discussions on the possibility of establishing a meat tax.

Most notably, a piece of legislation enacted in New Zealand in 2020 has signalled an intention to bring agricultural production into the country's Emissions Trading Scheme (FAIRR, 2020; International Carbon Action Partnership, 2021). Specifically, the amendment requires all farms to implement a system for measuring and reporting their greenhouse gas emissions by 2025. This requirement would support the entry of agricultural products into the Emissions Trading Scheme, a world first (FAIRR, 2020; Ministry for Primary Industries, 2021). If agricultural products do become subject to the Scheme, meat production will have to account for the cost of greenhouse gas emissions.

Meanwhile in 2019, German politicians proposed increasing the value-added tax on meat from 7% to 19% (Deutsche Welle, 2019). This proposal was uncommon as it seems to have been largely motivated by the desire to improve animal welfare rather than to tackle climate change (Eurogroup for Animals, 2019). In addition, the Danish Council of Ethics [4] (2016) recommended a tax on meat, with an emphasis on beef, but this recommendation was rejected in Parliament (FAIRR, 2017). Looking at Sweden, the government appears to have discussed the possibility of a tax on meat in both 2013 and 2015 (Bähr, 2015; Ryan, 2015), though we are unaware of any concrete outcomes. Finally, there have been some tentative suggestions in the Netherlands that a meat tax may be considered in the future (FAIRR, 2020).

At the supranational level, the European Parliament voted in 2021 to support the "Farm to Fork strategy" (European Parliament, 2021). This strategy contains provisions for decreasing greenhouse gas emissions from agriculture, and a modelling study has shown that implementing these provisions would cause the price of meat to increase (Barreiro Hurle et al., 2021).

There are several historical examples of taxes implemented in the UK that can be drawn upon as analogies (FAIRR, 2017).

The first is carbon pricing. A recent global meta-analysis found evidence that carbon pricing may have caused only a modest reduction of greenhouse gas emissions (Green, 2021). Nevertheless, that review did conclude that carbon pricing policies seemed particularly effective in the UK.

A second example is tobacco taxation. Taxes on tobacco are an effective way to reduce the prevalence of smoking (Hiscock et al., 2017). However, studies of tobacco taxes in the UK have found that the tobacco industry uses a variety of strategies to undermine the intended effect of these taxes (Hiscock et al., 2017). For example, price manipulation by the industry has led to greater sales of cheap cigarettes over time, limiting the number of people who would otherwise be motivated by higher taxes to quit smoking (Partos et al., 2020). These industry strategies appear to have dampened the effects of tobacco taxation on smoking prevalence in the UK.

Our third is the tax on sugary drinks. In discussions on the meat tax in the UK, it is common for people to refer to the UK Soft Drinks Industry Levy (Simmonds and Vallgårda, 2021). Introduced in 2018, this tax on high-sugar drinks, appears to have reduced sugar consumption from soft drinks (Pell et al., 2021). However, the tax was placed on manufacturers and importers (Scarborough et al., 2020), rather than consumers.The Soft Drinks Industry Levy was also motivated by health. While this may be partially the same for a meat tax, there is a larger role for both environmental and animal welfare justifications for a meat tax (Simmonds and Vallgårda, 2021). As such, the value of the Soft Drinks Industry Levy as an analogy for a meat tax may be limited.

While there is strong evidence that a meat tax can reduce the farming of some types of animals, there is also evidence that it can increase the farming of others. The small-animal replacement problem (SARP) is a known concern within many policies that aim to reduce meat consumption. Simply put, when people reduce their consumption of some meat products, they may increase their consumption of other meat products (Charity Entrepreneurship, 2018). In particular, people may reduce their consumption of larger animals like cows and sheep but increase their consumption of smaller animals like chickens and fish. The result is that the total number of animals consumed may increase.

Compounding this issue is the finding that chickens and fish tend to be farmed under conditions more harmful for their welfare than cows and sheep (Charity Entrepreneurship, 2018; Animal Charity Evaluators, 2020). This trend appears to hold true in the UK (Rioja-Lang et al., 2019). Therefore, if people eat fewer cows and sheep but more chickens and fish, the proportion of animals farmed under low-welfare conditions may also increase.

Policies are at a particular risk of causing the SARP when they aim to reduce meat consumption for environmental or health reasons. The environmental and health issues associated with the meat of large animals like pigs and cows tend to be more severe than those of small animals, although this varies by context (Godfray et al., 2018; Climate Change Committee, 2020; Petermann-Rocha et al., 2021; Ritchie, 2021). This is why studies modelling meat taxes focussed on environment or health concerns often predict increases (or smaller decreases) in the consumption of chickens and fish (e.g., Wirsenius, Hedenus and Mohlin, 2011). It is also worth noting that the welfare costs from even a small percentage increase in chicken and fish consumption, by weight, might be much larger than the welfare benefits from a large percentage decrease in cow and sheep consumption. This is because the number of chickens and fish consumed in the UK appears to be several orders of magnitudes higher than the number of cows or sheep (Sanders, 2020).

Since the SARP appears to be a significant risk from a meat tax, it would be valuable to know the exact risk. An estimate of the probability that a meat tax would be subject to the SARP would be of great help in deciding whether to campaign for a meat tax. However, this is difficult to establish given that no meat taxes have been implemented. As such, we do not believe it is feasible to make an useful estimate of this probability while maintaining a strong basis in reality [5]. As Simon (2013) points out in the book Meatonomics, all economic predictions of the outcome of a meat tax are just predictions, and it is impossible to be certain of the outcome in advance.

Nevertheless, studies on a meat tax provide strong evidence that it would be at high risk of causing the SARP. In addition, the risk of the SARP was explicitly raised by one interview participant, an employee of the Vegan Society, in an analysis of the meat tax debate in the UK (Simmonds and Vallgårda, 2021). The modelling study by Briggs et al. (2016) predicted that a meat tax in the UK would cause greater consumption of chickens (10%), fish (3%), and pigs (12%), despite the model also including a tax on meat from those animals. A similar prediction was made by Wirsenius et al. (2011) for the EU, with an increase in the consumption of both chickens (7%) and pigs (1%). Meanwhile, Revoredo-Giha et al. (2018) made similar predictions in their study, though the results varied across the modelled scenarios. In less relevant geographic areas, an increase in the consumption of chickens and fish was predicted in modelling studies by Edjabou and Smed (2013) (Denmark) and Abadie et al. (2016) (Norway). Similarly, Forero-Cantor et al. (2020) observed substitution between meat products in an economic model, concluding that such substitution might limit the environmental benefits of a meat tax.

Importantly, there are also several modelling studies that did not document an increase in the consumption of meat or animal products. These include Kehlbacher et al. (2016), Jansson and Säll (2018), Revoredo-Giha et al. (2018) (in some scenarios), and Springmann et al. (2016) (for highly developed countries). Consequently, the SARP is not a guaranteed outcome, but the possibility of its occurrence does mean that a meat tax carries the substantial risk of causing overall harm to animals.

In theory, there are several possible motivations for a meat tax, including reducing damage to the environment and the climate, improving health by reducing the incidence of disease, and reducing animal suffering.

Public debate on a meat tax is dominated by concerns related to the environment and health, rather than the needs of animals. Thus, a meat tax may be far more tractable if it is founded in environmental and health arguments. However, studies on these types of meat taxes generally suggest levying a greater tax on beef and lamb compared to fish and chickens. This means that a meat tax justified by environmental or health concerns may be at particular risk of the SARP.

It is much rarer to see proposals for meat taxes motivated by animal suffering justifications. We expect that a meat tax would be far less tractable if justified solely by the desire to reduce animal suffering. However, such a meat tax may be specifically designed to avoid the SARP. Most ambitiously, estimates of the suffering caused per unit of each type of food (B. Tomasik, 2018; e.g., Orzechowski, 2020) could be used to levy a greater tax on the most harmful products. We have not seen any formal proposals for a tax levied in this way. More commonly, authors arguing for meat taxes draw upon environmental and health justifications alongside animal justifications. This generally leads these authors to propose a flat price increase. For example, Singer (Singer, 2009) proposes a universal 50% increase in the retail price of all meat products, and Simon (2013) proposes a 50% increase in the price of any product that contains any animal-derived ingredients [6].

Risks of the SARP may be exacerbated by the fact that some people advocate for taxing only the meat from large animals. This can be understood as a selective version of health or environmental arguments and has been proposed or considered by several authors. Bonnet et al. (2018) conclude their modelling study by reporting that "the most efficient scenario would be to tax only the beef category at a high level since it would allow a 70% reduction in the total variation of GHG [greenhouse gas] emissions…". Similarly, Wirsenius et al. (2011) conclude their modelling study by reporting that "most of the effect of a GHG [greenhouse gas] weighted tax on animal food can be captured by taxing the consumption of ruminant meat alone." Meanwhile, Springmann et al. (2016; 2018) and Revoredo-Giha et al. (2018) explicitly model scenarios where a tax is placed on only red meat, while Kehlbacher et al. (2016) model a scenario where a tax is placed only on foods with above-average emissions, a scenario that excludes poultry and fish. It is reasonable to expect that a meat tax that only increases the price of meat from large animals would encourage people to consume more chicken and fish compared to a tax that also increases the price of chicken and fish. There is little doubt that this would increase the risk of the SARP. Therefore, if only the meat from large animals is taxed, a meat tax may be particularly likely to do more harm than good.

Several studies have examined public support for a meat tax. One highly relevant source is a report, commissioned by the UK government, called the National Food Strategy (2021). This report detailed many areas of UK food policy, and one policy under consideration was a meat tax. In the small-group "deliberative dialogues", the authors report low public support for a meat tax. The authors describe a meat tax as "politically impossible" and "by a long way … the least popular of any measure we discussed with citizens." A revealing excerpt is as follows:

"The idea of introducing a “meat tax” was a non-starter. Every time we raised it, the atmosphere would suddenly crackle with hostility. Although a minority of our panellists liked the idea, many more were vehemently opposed – and the arguments between these instantaneous tribes were fierce." (National Food Strategy, 2021)

Separately, the authors also conducted a public survey on support for a meat tax. The survey asked respondents about their support for two types of meat taxes - one for fresh meat, and one for processed meat. For fresh meat, 26% of respondents supported the tax (strongly or somewhat), 48% of respondents opposed the tax (strongly or somewhat), and 26% reported being unsure or neither. For processed meat, 48% of respondents supported the tax (strongly or somewhat), 24% of respondents opposed the tax (strongly or somewhat), and 28% reported being unsure or neither. These results appear to support the conclusions of the authors of the National Food Strategy, though support for a tax on processed meat was notably higher. One analyst, who worked on the National Food Strategy at the time, informed us via e-mail that both polls had a sample size of around 1,200 and conformed to the Market Research Society Code of Conduct. This Code of Conduct requires data collection to be fit for purpose and appropriate to the audience, implying that proper consideration was given to representativeness.

Another highly relevant source is a public opinion survey run in the UK by YouGov (2021). This survey had 2,169 respondents and included a question asking about support for a meat tax, with the results weighted to ensure that they were representative. In this survey, 20% of respondents supported a meat tax, 55% were opposed, and 25% were unsure or neutral. Interestingly, support for a meat tax in this survey appeared to be higher among Labour voters and among young people. We believe that this survey was sufficiently rigorous given the large sample size, the expertise of the company that conducted the survey, and the weighting of results to ensure representativeness.

We found one more public opinion survey that we believe deserves particular consideration. This survey was conducted in Norway in 2017, with 1,222 respondents who were approximately representative of the Norwegian population (Grimsrud et al., 2020). In this survey, 27% of respondents supported a meat tax, 57% were opposed, and 16% were unsure. We are confident in the rigour of this survey given the approximately representative sample, the large sample size, and the lack of any apparent conflicts of interest by the authors.

We are also aware of three further public opinion surveys, although we believe that the strength of the evidence from these surveys is lower. First, the True Animal Protein Price (TAPP) Coalition (2020) commissioned a survey of respondents in France (531 respondents), Germany (514), and the Netherlands (513). In those surveys, approximately 64-75% of respondents expressed support for a meat tax that was designed to improve animal welfare. In another question in those surveys, framed differently, approximately 50% of respondents expressed support. However, some scepticism about these findings may be warranted as the TAPP Coalition may have an interest in promoting the meat tax in public policy debates. In addition, while it is reported that there was an "appropriate distribution across gender, age, income and political background", it is unclear whether these distributions were representative of the national populations. Second, Yavuz (2020) reports a smaller survey in each of Sweden and Turkey. Since these surveys used non-random sampling methods and small sample sizes, it is difficult to draw generalizable conclusions. Finally, FAIRR (2017) reports a survey from Sweden where 25% of respondents supported a meat tax. However, this survey is being reported second-hand, and we cannot find the original source or any methodological details of the survey.

To summarise these quantitative measures, it appears that only a minority of the UK public are likely to support the establishment of a meat tax. There is notable agreement between the three surveys we consider particularly relevant and reliable, with 20%, 26%, or 27% of respondents in favour (Grimsrud et al., 2020; National Food Strategy, 2021; YouGov, 2021). Support may depend on demographics (YouGov, 2021) and be higher for a tax on processed meat only (National Food Strategy, 2021). Of course, these measures should not be regarded as constant since public opinion often changes as a policy or political debate develops (Adams-Cohen, 2020; e.g., Nordø, 2021).

With these findings in mind, further nuance can be added by considering several pieces of qualitative research. Focus groups conducted by Wellesley et al. (2015) revealed that participants expect the backlash from a meat tax to be short-lived, particularly if the policy and its justification were explained well. However, many people have expressed concern about the effects of a meat tax on lower-income people. Notably, this concern was also expressed by participants in the National Food Strategy (2021) report. Research has indeed identified that people's social class, education, and material resources influence their ability to change their food consumption patterns (Einhorn, 2021). In fact, some modelling studies have investigated this phenomenon explicitly in relation to a meat tax. Chalmers et al. (2016) predicted that different socioeconomic groups would respond to a meat tax differently while Kehlbacher et al. (2016) found that an emissions-focussed food tax would disproportionately penalise lower socioeconomic groups. Beyond this, the complex values surrounding the meat tax debate in the UK are analysed by Simmonds and Vallgarda (2021). This qualitative study examines public discourse in great detail, and interested readers would benefit from reading the study in full. For our purposes, the key conclusion is that there are two levels to the meat tax debate in the UK. The first centres on the question "Is meat consumption a problem in the UK?", and the second on "Is a meat tax the best way to reduce meat consumption?". Both questions are contested. A notable nuance, specific to the UK context, is that the UK's meat production is perceived by many to be "uniquely sustainable". This perception leads some to the conclusion that the UK has a responsibility to produce meat for export.

Although a meat tax appears very unpopular, there are some strategies that might be able to improve public support. A detailed review of the literature on public support for a meat tax is beyond the scope of this report, and we only offer a few select findings. We believe that delving into this literature in greater detail would be a fruitful endeavour for organisations interested in this question.

One major driver of public support is how the tax revenue would be used. In the book Meatonomics, Simon (2013) hypothesises that using the tax to provide a lump sum payment to every member of the public would substantially increase public support for the meat tax. In support of this hypothesis, studies have shown that public support for a meat tax may be increased if the revenue from the tax is used to pay for further public or environmental benefits (Wellesley, Happer and Froggatt, 2015; Grimsrud et al., 2020; TAPP Coalition, 2020; Muhammad, Mohd Hasnu and Ekins, 2021). A second major driver of public support is communication. Public support for environmental taxes is generally higher when the public is well-informed about the tax, the details of the tax, and the effectiveness of the tax (Muhammad, Mohd Hasnu and Ekins, 2021). Likewise, public support is generally higher when the policy is perceived to distribute costs and benefits fairly among members of society (Muhammad, Mohd Hasnu and Ekins, 2021). Finally, the public may offer greater support if a tax is described or framed in particular ways (Grimsrud et al., 2020).

It may be possible to enact a meat tax despite the likely low levels of public support. As Harris (2021) concludes, legislation can pass without public support, and the attitude of policymakers may be more relevant than public support in determining legislative success. As such, it is important to consider support among Members of Parliament (MPs).

Recently, senior officials in the UK government, currently led by the Conservative Party, have publicly stated that they are opposed to a meat tax. One official was quoted by newspaper The Sun: "This is categorically not going to happen." (National Food Strategy, 2021). This official was speaking in the context of media attention sparked by a leaked memo, in which the Prime Minister asked government departments to report the prices that would correspond to carbon emissions in those departments' jurisdictions (Clark, 2021). Given this public commitment, it appears unlikely that the Conservative Party's UK government would support a meat tax, although government officials do sometimes fail to fulfil pledges (Thomson et al., 2017).

Given that there appears to be a partisan divide in attitudes towards meat consumption, with support for a meat tax higher among Labour voters (YouGov, 2021), it is also worth considering the views of MPs from other parties. A comment by one Labour MP did not rule out the possibility of a meat tax (Kendal, 2019) while the party's environment manifesto does appear to support a reduced consumption of red and processed meat (Labour Party, 2019a). However, the party's environment manifesto and animal welfare manifesto both contain references to working with farmers and fishers (Labour Party, 2019a, 2019b). Given that a meat tax is likely to be opposed by farmers and fishers, it is difficult to predict whether the Labour Party would support such a tax.

There are two other parties with moderate representation in the UK Parliament: the Scottish National Party and the Liberal Democrats. We are aware of no public comments on a meat tax by MPs or representatives of either of these parties. The manifesto of the Scottish National Party contains no reference to reducing meat consumption. While the party seeks to reduce emissions, it appears to favour methods that also support farmers (Scottish National Party, 2021). Conversely, a policy paper by the Liberal Democrats on climate does state that "consumption of meat and dairy products will have to fall" (Liberal Democrats, 2019). There may also be support for a meat tax among smaller parties, such as the Green Party (Harvey and van der Zee, 2019), although such parties currently hold very few seats in the UK Parliament.

We do not consider enforcement to present any difficulties in implementing a meat tax. In New Zealand, there appears to be some indication that there are challenges with measuring and pricing greenhouse gas emissions from agriculture. Delaying implementation until 2025 was intended to allow the government and the agricultural industry to develop systems by which to measure and price agricultural emissions (FAIRR, 2020).

A separate issue is that tax policies often experience a small amount of tax evasion. However, given that a meat tax would be enforced by the government in the same way as any other tax, tax evasion is not likely to meaningfully impact animal suffering. Compared to the major challenges with enforcement of other animal campaigns, enforcement of a meat tax is likely to be a non-issue.

Bähr (2015) analysed a meat tax with regards to the several levels of legal regulation. This analysis focussed on the EU and so it is not entirely applicable to the UK. However, the analysis showed that a carefully designed meat tax is legal and consistent with the many regulations facing a state. These include the environmental legal framework of the EU, international climate change regulations, international trade law, and human rights law. A study by Arvidsson (2016), also focussing on the EU context, largely agreed with these conclusions. That study also identified several legislative mechanisms by which a meat tax could be implemented in the EU, including an excise duty, emissions taxation, or a reform of the Value Added Tax system. The latter mechanism could, specifically, involve raising the Value Added Tax on a particular set of products.

Mahoney (2007) performed a quantitative analysis of the success rates of lobbying in the US and the EU. All else being equal, the success rate for lobbying efforts that are multi-sector or system-wide appears to be 20% or lower. Moreover, the analysis also shows that lobbying efforts that have directly conflicting perspectives were "most likely to achieve none of their lobbying goals". Meanwhile, the analysis demonstrates that higher public salience of an issue is associated with a lower probability of success. Separately, Soule and Olzak (2004) showed that an issue has a particularly low probability of succeeding if public support is low.

Given this evidence, the outlook for a successful meat tax campaign appears to be pessimistic. Since a meat tax affects all agricultural producers and almost all consumers, it would be classified as multi-sector or system wide. Public opinion surveys and "deliberative dialogues" suggest low public support and fierce opposition, while the media interest sparked by a single leaked government memo (e.g., Clark, 2021) suggests that any discussion on a meat tax would experience high salience in the media. Therefore, we would expect the probability of success of a meat tax campaign to be well below the 20% figure cited above. In our detailed analysis, we have decided to use 5% as the probability of success. Regardless of the accuracy of this specific 5% figure, the tractability of a meat tax campaign appears to be very low.

To complement our review of the evidence, we interviewed one of the authors from Revoredo-Giha et al (2018), Wirsenius et al (2011) and Briggs et al (2016). This was particularly beneficial since we view these as the most important papers for our analysis. The general view from these authors was that a carbon-weighted foods tax would have a consistently good effect on environmental outcomes but that the exact changes in the consumption of different products would be difficult to predict. This was both due to the limitations of the data we have available for modelling, leading to the extrapolation of findings far outside their original context, and because of the complexity of the interactions between different products. This is a particular problem outside of the United Kingdom where most research up to now has taken place. In a global context, the elasticity of goods may only be tracked as a commodity rather than a product, making it even more difficult to project real-world outcomes from these models.

Overall, our interviews with experts highlighted the empirical and theoretical uncertainty with these sorts of models and within any tax policies on food. The effects of any tax policy will be difficult to project in advance and will likely lead to unforeseen consequences in the food system. The most likely of these is an increase in chicken and pork consumption which experts commented that there is a significant chance there will be an increase. An exception to this was a flat tax on all meat or animal products where the relative price of these products did not change. If this came into effect, the models we reviewed predict that overall consumption of these products would decrease as consumers shift to more vegetables and grains. The proportion of each type of food within consumers' overall purchases would likely stay the same, thus avoiding the SARP. Although their were doubts over the political feasibility of such a policy.

We performed a detailed analysis in which we modelled the effects of a meat tax on the lives of animals.

When concluding whether a meat tax will improve the lives of animals, there are many important factors to consider, including the set of food products being taxed, the cross-price elasticities of those products, and the size of the tax on each product. Therefore, to get an idea of the variance in predictions from different studies, we have modelled nine scenarios. Each scenario is derived from one of six studies:

The decision to use these plausible, off-the-shelf scenarios avoids the need to estimate the taxes and model the subsequent changes in consumption ourselves. Our literature review identified many studies that modelled the effects of a meat tax on consumption (see Appendix). From those studies, we selected the six studies above for two reasons. Firstly, these studies each include a wide range of meat and animal products, which is important for understanding the overall effect of a tax across many animal species. Secondly, these studies are relevant to the context of the UK or the EU. Where the studies modelled both uncompensated (i.e., a revenue-positive tax) and compensated (i.e., a revenue-neutral tax) scenarios, we used the compensated scenario. These scenarios tended to give similar changes in consumption, and we feel that a compensated, revenue-neutral tax is more politically plausible.

Each of the selected studies conducts an economic model of the effects of a tax on consumption changes across many different types of meat and animal products. In all of the selected studies, the taxes for each product were determined according to the greenhouse gas emissions of that product. We believe that this is an appropriate choice, as the conversation on the meat tax has been dominated by environmental concerns (see ‘Tractability’ above). Notably, there is also public discussion on a meat tax for health reasons. However, fewer studies appear to model the effects of a meat tax for health, and the ones that do are both less specific to the UK context and consider far fewer products (see Appendix). One exception to this is Briggs et al. (2016) which considers how the emissions-focused tax subsequently affects health.

In our analysis, we considered pigs, finfish (both wild-caught and farmed), poultry animals (including chickens and turkeys), and ruminant animals (including cows and sheep). We considered cows bred for meat and for dairy, and chickens for meat and for eggs. We calculated the effects of a meat tax on the suffering of these animals as follows. Firstly, we calculated how many animals of each group are consumed in the UK each year. We then obtained the percentage changes in consumption of each of these animals, as predicted by each scenario outlined above. From here, we calculated how many animals of each group would no longer be consumed under each scenario. We also incorporated information on the average lifespans of each group of animals. This allowed us to report the number of animals, adjusted for lifespan, saved each year by a meat tax.

We express our results as the change in animal-years consumed. "Animal-years consumed" are defined as the number of animals consumed multiplied by the average lifespans of those animals. A decrease in animal-years consumed represents an overall benefit for animals, while an increase represents overall harm to animals.

We should note that the study by Revoredo-Giha et al. (2018) models 32 scenarios. Only sixteen of these are based on a compensated (revenue-neutral) tax. Of those sixteen, we chose the four with a medium tax rate. The other 12 scenarios, when modelled alongside our analysis, mostly give results that are more or less extreme versions of the four scenarios that we did choose - a higher tax rate makes the overall harmful scenarios more harmful, and the overall beneficial scenarios more beneficial. Notably, the ad-valorem tax scenario in that study does work slightly differently. However, that scenario is less comparable to the other studies and its inclusion would not meaningfully change our overall results.

The results showed that there was an extreme variance in the effects of a meat tax on the lives of farmed animals (Table 1). These results indicate that the potential outcomes of a meat tax span a considerable scale, from extremely harmful to animals to extremely beneficial to animals.

Five of the studies predicted that a meat tax would cause a net decrease in animal-years consumed, which represents an overall benefit for farmed animals (Studies 1, 3, 5, 6C, and 6D). The decrease in annual consumption ranged from 2.28 to 18.4 million animal-years.

Conversely, four of the studies predicted that a meat tax would cause a net increase in animal-years consumed, representing overall harm to farmed animals (Studies 2, 4, 6A, 6B). The increase in annual consumption ranged from 1.55 to 15.0 million animal-years.

In other words, the SARP was observed in four of the nine studies that were included in this analysis. This indicates that causing a large overall increase in the consumption of farmed animals is a genuine risk of a meat tax.

The most salient finding from our detailed analysis is that the predicted outcome of a meat tax can vary significantly. Some of the modelling studies predict that a meat tax would result in overall benefits to farmed animals, and some predict that a meat tax would result in overall harm to farmed animals. Moreover, there is no obvious pattern that governs which studies predict which outcome.

Our interpretation is that meat tax models act as something like a chaotic system. That is, a particular model involves many choices - which country or community, which products to tax, which data sources, which elasticities, which tax rates, and so on - that cumulatively determine the outcome. Importantly, these choices interact in complex ways, making it impossible to predict the outcome of any meat tax model just by looking at the choices made.

Therefore, it is implausible to say in advance whether a meat tax model predicts overall benefits or overall harm to farmed animals. By extension, it is implausible to say whether a meat tax in reality would bring overall benefits or overall harm to farmed animals. This indicates that the animal advocacy movement should probably stay away from campaigning for a meat tax since it is too difficult to know whether such a campaign would be good or bad for animals. Considering there are many campaigns that have robust evidence in favour of them, dedicating a campaign to a meat tax seems ill-advised.

Evidence against this chaotic view comes from Jansson and Säll (2018), who point out that they observed cross-country differences in consumption changes due to different levels of production, consumption, and elasticity. This might increase the credibility of a claim that the country in which a meat tax is implemented matters significantly. Nevertheless, in our detailed analysis, even the studies that focused purely on the UK (Studies 1-3, 6) showed substantial variation in results. Therefore, while the location of the study may have some effect on the outcome, it is still too difficult to predict the outcome of the study purely on the basis of country.

There are some possible exceptions to this chaotic view. For example, a meat tax levied on animal suffering would be tailor-made to prevent the SARP (see ‘The type of meat tax might matter’ above). This type of meat tax would almost certainly bring overall benefits for farmed animals. However, we feel strongly that this type of meat tax would be unrealistic to implement. Given that there is very low public support for a meat tax levied for environmental or health reasons, it seems near impossible to gain support for a meat tax levied for a justification (preventing animal suffering) with even lower public support.

Table 1. Results of our effectiveness analysis, in which we consider the effects of a meat tax on farmed animals in the UK. We considered nine scenarios. An overall benefit for animals is represented by a decrease in animal-years consumed.

A meat tax would also cause many effects that have not been included in our model. In this section, we will briefly describe the most significant of these.

During egg production, male chicks are considered a waste product and are killed in large numbers (Reithmayer, Mußhoff and Danne, 2020). Therefore, a change in egg production is likely to cause a change in the number of male chicks bred and killed during egg production. It seems reasonable to assume that there is a positive relationship between egg production and the number of male chicks killed, although we haven't tested this assumption. Six studies (Studies 1-4, 6C, 6D) predict a decrease in egg consumption, so it is reasonable to expect that those six studies would result in fewer male chicks being bred and killed. Two studies (Studies 6A, 6B) predict an increase in egg consumption, so it is reasonable to expect that those six studies would result in more male chicks being bred and killed. There is substantial variance in the magnitude of the predicted change in egg consumption across all studies.

Notably, it appears that some male chicks bred by the egg industry are killed to produce food for pet snakes (Wills, 2021). Therefore, a decrease in the number of male chicks bred and killed may also cause an increase in the number of rats and mice to be bred and killed to meet this demand for pet food, and vice-versa (Šimčikas, 2019).

A change in farmed fish production is likely to cause a change in the number of farmed fish who are bred but die before slaughter. It is reasonable to assume that there is a positive relationship between farmed fish production and the number of farmed fish who die before slaughter, although we haven't tested this assumption. For Scottish farmed salmon, up to a quarter may die before slaughter (Ellis et al., 2016) and this figure does not count fish that die in the very early stages of production. Three studies (Studies 1, 3, 6D) predict a decrease in the consumption of farmed fish, and we would expect this to translate to a decrease in the number of farmed fish who are bred but die before slaughter. Four studies (Studies 2, 6A-6C) predict an increase in the consumption of farmed fish, and we would expect this to translate to an increase in the number of farmed fish who are bred but die before slaughter. There is substantial variance in the magnitude of the predicted change in farmed fish consumption across all studies. Notably, two studies (Studies 5, 6) excluded fish in their analysis.

A change in farmed animal consumption is likely to cause a change in the number of wild fish caught for fishmeal production. In the UK, fishmeal is used in the diet of farmed fish, poultry, and pigs (Seafish, 2016). It seems reasonable to assume that there is a positive relationship between the production of farmed fish, poultry, and pigs and the production of fishmeal, although we haven't tested this assumption. Three studies (Studies 1, 3, 6D) predict a decrease in the consumption of farmed fish, poultry, and pigs, and we would expect this to translate to a decrease in fishmeal production. Two studies (Studies 2, 6A) predict an increase in the consumption of farmed fish, poultry, and pigs, and we would expect this to translate to an increase in fishmeal production. There is substantial variation in the magnitude of the predicted change in consumption of farmed fish, poultry, and pigs across all studies. Four studies either predicted a different direction of consumption change between farmed fish, poultry, and pigs (Studies 6B, 6C), or excluded fish from the analysis (Studies 4, 5).

A change in dairy consumption is likely to cause a change in the number of calves who are bred by the dairy industry and slaughtered for veal. It is unclear whether veal consumption is driven primarily by supply from producers or demand from consumers. It is possible that a decrease in veal supply would simply encourage consumers to purchase other types of meat. As such, we are hesitant to speculate on the effects of a meat tax on calves who are bred by the dairy industry and slaughtered for veal.

A meat tax would, almost certainly, reduce the production and consumption of red meat. A reduced production of red meat is likely to reduce the greenhouse gas emissions from agriculture (Revoredo-Giha, Chalmers and Akaichi, 2018). Lower greenhouse gas emissions would help in humanity's battle against climate change. However, the effects of climate change on animal suffering are unclear (Brian Tomasik, 2018). Separately, the reduced consumption of red meat is likely to improve human health, at least among privileged socio-economic groups (Briggs et al., 2013). However, a meat tax may cause overall harm to human health among less privileged socio-economic groups (Kehlbacher et al., 2016).

There is a risk that a poorly designed meat tax could cause demand to shift from domestically produced meat to imported meat. If the tax is levied on production, rather than consumption, then the price of domestically produced meat would increase, but the price of imported meat would not (Wirsenius, Hedenus and Mohlin, 2011; García-Muros et al., 2017). This would incentivise consumers to substitute domestically produced meat for imported meat. The result of such a policy may be that animal suffering is not necessarily reduced, but merely displaced to a different country. Animal suffering may even increase overall, as farmed animal welfare in the UK appears to be better than average (World Animal Protection, 2020). To avoid merely shifting animal suffering to a different country, a meat tax would ideally be levied on consumption rather than production (Wirsenius, Hedenus and Mohlin, 2011; García-Muros et al., 2017). Levying the tax on consumption would increase the price of both domestically produced and imported meats, thus eliminating the incentive for consumers to substitute towards imported meat.

It is possible that a meat tax would raise revenue for the government. This revenue can be used to deliver further benefits. For example, the government could use the revenue to reduce other taxes, such as income tax or value-added tax (Grimsrud et al., 2020; Muhammad, Mohd Hasnu and Ekins, 2021). This may deliver economic benefits and improve human wellbeing, although that hypothesis depends on context and is debated in the literature (Freire-González, 2018). An example of this is found in several of the modelling studies we reviewed that explicitly consider scenarios where the tax revenue is used to subsidise low-emission foods (Briggs et al., 2013, 2016; Edjabou and Smed, 2013). Similarly, the government could use the revenue to deliver public benefits such as lump-sum payments (Simon, 2013) or reduced university tuition fees (Muhammad, Mohd Hasnu and Ekins, 2021), each of which may have positive social effects. Alternatively, the government could deliver environmental benefits, such as habitat protection or the further development of renewable energy (Grimsrud et al., 2020; Muhammad, Mohd Hasnu and Ekins, 2021). These measures would likely improve environmental sustainability and human wellbeing. However, environmental benefits may cause greater suffering to animals, depending on the context and given some strong assumptions (e.g., Tomasik, 2017; Brian Tomasik, 2018).

A meat tax may affect the animal advocacy movement in the long-term, although it is difficult to predict whether this effect would be good or bad. Simon (2013) argues that a meat tax would lead to large-scale system change, thus contributing towards the eventual abolition of commercial animal exploitation. However, it is also plausible that a meat tax would lead people to believe that it is acceptable to exploit animals, as long as the cost of doing so is high enough. This could make people feel less complicit in animal exploitation, potentially contributing to the "psychological refuge effect" (Anthis, 2017). This may reduce public support for further animal advocacy campaigns.

In conclusion, we do not recommend a meat tax as a campaign for animal advocacy organisations. While a meat tax could reduce the number of animals killed for food, the tax also carries a substantial risk of increasing this number and thus causing overall harm. The probability of this risk is very difficult to calculate. However, as shown in our detailed analysis, many modelling studies do indeed predict an overall increase in the number of animals killed for food. In particular, many environmental- and health-motivated policies would place higher taxes on beef than chicken or fish, exacerbating this risk. Furthermore, public support for a meat tax is very low meaning any campaign would have a low probability of success. For this reason, we do not recommend campaigning for a meat tax. We instead encourage animal advocacy organisations to select an ask that has a more robust and favourable base of evidence.

Table A1. Modelling studies identified in our literature review on the effects of a meat tax on consumption. Note that we only included studies in this table if they modelled and reported the percentage change in consumption for at least one type of meat.

Source | Products considered | Location | Taxes determined by… | Used in our model? |

(Briggs et al., 2013) | Many groups of food including meat, non-meat, and drinks | UK | Greenhouse gas emissions | Yes (Study 1) |

(Briggs et al., 2016) | Many groups of food including meat, non-meat, and drinks | UK | Greenhouse gas emissions | Yes (Study 2) |

(Kehlbacher et al., 2016) | Many groups of food including meat, non-meat, and drinks | UK | Greenhouse gas emissions | Yes (Study 3) |

(Wirsenius, Hedenus and Mohlin, 2011) | Ruminant meat, pig meat, poultry, meat, eggs | EU | Greenhouse gas emissions | Yes (Study 4) |

(Jansson and Säll, 2018) | Beef, pork, sheep and goat, poultry, eggs, and numerous dairy products | EU | Greenhouse gas emissions | Yes (Study 5) |

(Revoredo-Giha, Chalmers and Akaichi, 2018) | Many groups of food including meat, non-meat, and drinks | UK | Greenhouse gas emissions | Yes (Study 6) |

(Edjabou and Smed, 2013) | Many groups of food including meat and non-meat | Denmark | Greenhouse gas emissions | No |

(Abadie et al., 2016) | Many groups of food including meat, non-meat, and drinks | Norway | Greenhouse gas emissions | No |

(Springmann et al., 2016) | Many groups of food including meat and non-meat | Global | Greenhouse gas emissions | No |

(Springmann, Mason-D’Croz, et al., 2018) | Red meat, processed meat | Global | Health (healthcare costs of consumption) | No |

(Broeks et al., 2020) | All meat | Netherlands | Arbitrarily determined | No |

(Lee et al., 2021) | Meat and dairy | UK | Greenhouse gas emissions | No |

(Roosen, Staudigel and Rahbauer, 2022) | Poultry, pork, and beef and veal | Germany | Greenhouse gas emissions, ad valorem tax | No |

(Schmidt et al., 2021) | Many groups of food including meat and non-meat | Switzerland | Nitrogen pollution | No |

(Chalmers, Revoredo-Giha and Shackley, 2016) | Beef, chicken, pork, sheep, turkey | Scotland | Greenhouse gas emissions | No |

(Springmann, Sacks, et al., 2018) | Many groups of food including meat, non-meat, and drinks | Australia | Greenhouse gas emissions | No |

(Dogbe and Gil, 2018) | Many groups of food including meat, non-meat, and drinks | Catalonia | Greenhouse gas emissions | No |

(Kotakorpi et al., 2011) | Meat, fish, and some non-animal foods | Finland | Health (sugar content) | No |

(Gren, Höglind and Jansson, 2021) | Many groups of food including meat and non-meat | Sweden | Greenhouse gas emissions | No |

Abadie, L.M. et al. (2016) ‘Using food taxes and subsidies to achieve emission reduction targets in Norway’, Journal of cleaner production, 134, pp. 280–297. doi:10.1016/j.jclepro.2015.09.054.

Adams-Cohen, N.J. (2020) ‘Policy Change and Public Opinion: Measuring Shifting Political Sentiment With Social Media Data’, American Politics Research, 48(5), pp. 612–621. doi:10.1177/1532673X20920263.

Animal Charity Evaluators (2020) Farmed Fish Welfare Report, Animal Charity Evaluators. Available at: https://animalcharityevaluators.org/research/other-topics/farmed-fish-welfare-report/#full-report.

Anthis, J.R. (2017) Survey of US Attitudes Towards Animal Farming and Animal-Free Food, Sentience Institute. Available at: https://www.sentienceinstitute.org/animal-farming-attitudes-survey-2017.

Arvidsson, J. (2016) Getting the price right - Exploring the legal possibilities of taxing meat and dairy consumption in the EU on environmental grounds. Master of Laws. Faculty of Law, Lund University. Available at: https://lup.lub.lu.se/student-papers/record/8875289 (Accessed: 22 December 2021).

Bähr, C.C. (2015) ‘Greenhouse Gas Taxes on Meat Products: A Legal Perspective’, Transnational Environmental Law, 4(1), pp. 153–179. doi:10.1017/S2047102515000011.

Barreiro Hurle, J. et al. (2021) Modelling environmental and climate ambition in the agricultural sector with the CAPRI model. Publications Office of the European Union. doi:10.2760/98160.

Bonnet, C., Bouamra-Mechemache, Z. and Corre, T. (2018) ‘An Environmental Tax Towards More Sustainable Food: Empirical Evidence of the Consumption of Animal Products in France’, Ecological economics: the journal of the International Society for Ecological Economics, 147, pp. 48–61. doi:10.1016/j.ecolecon.2017.12.032.

Borenstein, M. et al. (2021) Introduction to Meta-Analysis. John Wiley & Sons. Available at: https://play.google.com/store/books/details?id=pdQnEAAAQBAJ.

Briggs, A.D.M. et al. (2013) ‘Assessing the impact on chronic disease of incorporating the societal cost of greenhouse gases into the price of food: an econometric and comparative risk assessment modelling study’, BMJ open, 3(10), p. e003543. doi:10.1136/bmjopen-2013-003543.

Briggs, A.D.M. et al. (2016) ‘Simulating the impact on health of internalising the cost of carbon in food prices combined with a tax on sugar-sweetened beverages’, BMC public health, 16, p. 107. doi:10.1186/s12889-016-2723-8.

Broeks, M.J. et al. (2020) ‘A social cost-benefit analysis of meat taxation and a fruit and vegetables subsidy for a healthy and sustainable food consumption in the Netherlands’, BMC public health, 20(1), p. 643. doi:10.1186/s12889-020-08590-z.

Chalmers, N.G., Revoredo-Giha, C. and Shackley, S. (2016) ‘Socioeconomic Effects of Reducing Household Carbon Footprints Through Meat Consumption Taxes’, Journal of Food Products Marketing, 22(2), pp. 258–277. doi:10.1080/10454446.2015.1048024.

Charity Entrepreneurship (2018) Small animal replacement problem, Charity Entrepreneurship. Available at: charityentrepreneurship.com/post/small-animal-replacement-problem.

Clark, N. (2021) HANDS OFF OUR SAUSAGES No10 slaps down plans for ‘meat tax’ after outrage from MPs over green agenda, The Sun. Available at: https://www.thesun.co.uk/news/politics/13949302/meat-tax-boris-johnson-green-agenda/.

Climate Change Committee (2020) Land use: Policies for a Net Zero UK. Climate Change Committee. Available at: https://www.theccc.org.uk/publication/land-use-policies-for-a-net-zero-uk/.

Deutsche Welle (2019) Germany: ‘Meat tax’ on the table to protect the climate, Deutsche Welle. Available at: https://www.dw.com/en/germany-meat-tax-on-the-table-to-protect-the-climate/a-49924795.

Dhont, K., Piazza, J. and Hodson, G. (2021) ‘The role of meat appetite in willfully disregarding factory farming as a pandemic catalyst risk’, Appetite, 164, p. 105279. doi:10.1016/j.appet.2021.105279.

Dogbe, W. and Gil, J.M. (2018) ‘Effectiveness of a carbon tax to promote a climate-friendly food consumption’, Food policy, 79, pp. 235–246. doi:10.1016/j.foodpol.2018.08.003.

Edjabou, L.D. and Smed, S. (2013) ‘The effect of using consumption taxes on foods to promote climate friendly diets – The case of Denmark’, Food policy, 39, pp. 84–96. doi:10.1016/j.foodpol.2012.12.004.

Einhorn, L. (2021) ‘Meat consumption, classed?’, Österreichische Zeitschrift für Soziologie, 46(2), pp. 125–146. doi:10.1007/s11614-021-00452-1.

Ellis, T. et al. (2016) ‘Trends during development of Scottish salmon farming: An example of sustainable intensification?’, Aquaculture , 458, pp. 82–99. doi:10.1016/j.aquaculture.2016.02.012.

Epstein, L.H. et al. (2012) ‘Experimental research on the relation between food price changes and food-purchasing patterns: a targeted review’, The American journal of clinical nutrition, 95(4), pp. 789–809. doi:10.3945/ajcn.111.024380.

Eurogroup for Animals (2019) Germany’s meat tax: Would it work? Has it been considered elsewhere in Europe?, Eurogroup for Animals. Available at: https://www.eurogroupforanimals.org/news/germanys-meat-tax-would-it-work-has-it-been-considered-elsewhere-europe.

European Parliament (2021) New EU farm to fork strategy to make our food healthier and more sustainable, News: European Parliament. Available at: https://www.europarl.europa.eu/news/en/press-room/20211014IPR14914/new-eu-farm-to-fork-strategy-to-make-our-food-healthier-and-more-sustainable.

FAIRR (2017) The Livestock Levy: Are regulators considering meat taxes? FAIRR. Available at: https://www.fairr.org/article/livestock-levy-regulators-considering-meat-taxes/.

FAIRR (2020) The Livestock Levy: Progress Report. Farm Animal Investment Risk & Return.

Forero-Cantor, G., Ribal, J. and Sanjuan, N. (2020) ‘Levying carbon footprint taxes on animal-sourced foods. A case study in Spain’, Journal of cleaner production, 243. doi:10.1016/j.jclepro.2019.118668.

Freire-González, J. (2018) ‘Environmental taxation and the double dividend hypothesis in CGE modelling literature: A critical review’, Journal of Policy Modeling, 40(1), pp. 194–223. doi:10.1016/j.jpolmod.2017.11.002.

García-Muros, X. et al. (2017) ‘The distributional effects of carbon-based food taxes’, Journal of cleaner production, 140, pp. 996–1006. doi:10.1016/j.jclepro.2016.05.171.

Garnett, E.E. et al. (2021) ‘Price of change: Does a small alteration to the price of meat and vegetarian options affect their sales?’, Journal of environmental psychology, 75, p. 101589. doi:10.1016/j.jenvp.2021.101589.

Godfray, H.C.J. et al. (2018) ‘Meat consumption, health, and the environment’, Science, 361(6399). doi:10.1126/science.aam5324.

de Graad, F. (2020) ‘Exploring the possibility of a meat tax’, in Sustainable Development and Resource Productivity. Routledge, pp. 329–336. Available at: https://library.oapen.org/bitstream/handle/20.500.12657/42894/9781000213645.pdf?sequence=1#page=348.

Green, J.F. (2021) ‘Does carbon pricing reduce emissions? A review of ex-post analyses’, Environmental research letters: ERL [Web site], 16(4), p. 043004. doi:10.1088/1748-9326/abdae9.

Gren, I.-M., Höglind, L. and Jansson, T. (2021) ‘Refunding of a climate tax on food consumption in Sweden’, Food policy, 100, p. 102021. doi:10.1016/j.foodpol.2020.102021.

Grimsrud, K.M. et al. (2020) ‘Public acceptance and willingness to pay cost-effective taxes on red meat and city traffic in Norway’, Journal of Environmental Economics and Policy, 9(3), pp. 251–268. doi:10.1080/21606544.2019.1673213.

Harris, J. (2020) Health Behavior Interventions Literature Review, Sentience Institute. Available at: https://www.sentienceinstitute.org/health-behavior.

Harris, J. (2021) Key Lessons From Social Movement History, Sentience Institute. Available at: https://www.sentienceinstitute.org/blog/key-lessons-from-social-movement-history.

Harvey, F. and van der Zee, B. (2019) Caroline Lucas urges parliament to ‘seriously consider’ tax on meat, The Guardian. Available at: https://www.theguardian.com/environment/2019/jan/04/caroline-lucas-green-mp-meat-tax-oxford-farmers-conference-prioritise-sustainability.

Hiscock, R. et al. (2017) ‘Tobacco industry strategies undermine government tax policy: evidence from commercial data’, Tobacco control [Preprint]. doi:10.1136/tobaccocontrol-2017-053891.

International Carbon Action Partnership (2021) New Zealand Emissions Trading Scheme. International Carbon Action Partnership. Available at: https://icapcarbonaction.com/en/?option=com_etsmap&task=export&format=pdf&layout=list&systems%5B%5D=48.

Jansson, T. and Säll, S. (2018) ‘Environmental Consumption Taxes on Animal Food Products to Mitigate Greenhouse Gas Emissions from the European Union’, Climate Change Economics, 09(04), p. 1850009. doi:10.1142/S2010007818500094.

Jensen, J.D. et al. (2016) ‘Effects of the Danish saturated fat tax on the demand for meat and dairy products’, Public health nutrition, 19(17), pp. 3085–3094. doi:10.1017/S1368980015002360.

Kehlbacher, A. et al. (2016) ‘The distributional and nutritional impacts and mitigation potential of emission-based food taxes in the UK’, Climatic change, 137(1), pp. 121–141. doi:10.1007/s10584-016-1673-6.

Kendal, L. (2019) Could Meat be Made Illegal?, Viva! Available at: https://viva.org.uk/blog/could-meat-be-made-illegal/.

Kotakorpi, K. et al. (2011) The Welfare Effects of Health-based Food Tax Policy. 3633. CESifo. Available at: https://ideas.repec.org/p/ces/ceswps/_3633.html (Accessed: 31 December 2021).

Labour Party (2019a) A Plan for Nature: Our Manifesto for the Environment. Labour Party. Available at: https://labour.org.uk/wp-content/uploads/2019/11/FINAL-FOR-WEB_13172_19-Environment-Manifesto.pdf.

Labour Party (2019b) Labour’s Animal Welfare Manifesto. Labour Party. Available at: https://labour.org.uk/wp-content/uploads/2019/11/13073_19-ANIMAL-WELFARE-MANIFESTO-Update-2.pdf.

Lee, M.R.F. et al. (2021) ‘Nutrient provision capacity of alternative livestock farming systems per area of arable farmland required’, Scientific reports, 11(1), p. 14975. doi:10.1038/s41598-021-93782-9.

Liberal Democrats (2019) Tackling the Climate Emergency. Policy Paper 139. Liberal Democrats. Available at: https://d3n8a8pro7vhmx.cloudfront.net/libdems/pages/46346/attachments/original/1564404765/139_-_Tackling_the_Climate_Emergency_web.pdf?1564404765.

Mahoney, C. (2007) ‘Lobbying Success in the United States and the European Union’, Journal of public policy, 27(1), pp. 35–56. doi:10.1017/S0143814X07000608.

Ministry for Primary Industries (2021) Climate change and the primary industries, Ministry for Primary Industries. Available at: https://www.mpi.govt.nz/funding-rural-support/environment-and-natural-resources/climate-change-primary-industries/.

Mosca, J. (2020) ‘Taxing meat: An analysis of narratives from Swedish news articles (Trabajo Final de Máster). Uppsala University’.

Muhammad, I., Mohd Hasnu, N.N. and Ekins, P. (2021) ‘Empirical Research of Public Acceptance on Environmental Tax: A Systematic Literature Review’, Environments, 8(10), p. 109. doi:10.3390/environments8100109.

National Food Strategy (2021) National Food Strategy: Independent Review. National Food Strategy. Available at: https://www.nationalfoodstrategy.org/wp-content/uploads/2021/10/25585_1669_NFS_The_Plan_July21_S12_New-1.pdf.

Nordø, Å.D. (2021) ‘Do voters follow? The effect of party cues on public opinion during a process of policy change’, Scandinavian political studies, 44(1), pp. 45–66. doi:10.1111/1467-9477.12187.

Orzechowski, K. (2020) Deaths Per Calorie & Effective Advocacy: A Case For Standardization, Faunalytics. Available at: https://faunalytics.org/deaths-per-calorie-and-effective-advocacy-a-case-for-standadization/.

Partos, T.R. et al. (2020) Impact of tobacco tax increases and industry pricing on smoking behaviours and inequalities: a mixed-methods study. Southampton (UK): NIHR Journals Library. doi:10.3310/phr08060.

Pell, D. et al. (2021) ‘Changes in soft drinks purchased by British households associated with the UK soft drinks industry levy: controlled interrupted time series analysis’, BMJ , 372, p. n254. doi:10.1136/bmj.n254.

Petermann-Rocha, F. et al. (2021) ‘Vegetarians, fish, poultry, and meat-eaters: who has higher risk of cardiovascular disease incidence and mortality? A prospective study from UK Biobank’, European heart journal, 42(12), pp. 1136–1143. doi:10.1093/eurheartj/ehaa939.

Reithmayer, C., Mußhoff, O. and Danne, M. (2020) ‘Alternatives to culling male chicks--the consumer perspective’, British Food Journal [Preprint]. Available at: https://www.emerald.com/insight/content/doi/10.1108/BFJ-05-2019-0356/full/html.

Revoredo-Giha, C., Chalmers, N. and Akaichi, F. (2018) ‘Simulating the Impact of Carbon Taxes on Greenhouse Gas Emission and Nutrition in the UK’, Sustainability: Science Practice and Policy, 10(1), p. 134. doi:10.3390/su10010134.

Rioja-Lang, F.C. et al. (2019) ‘Prioritization of Farm Animal Welfare Issues Using Expert Consensus’, Frontiers in veterinary science, 6, p. 495. doi:10.3389/fvets.2019.00495.

Ritchie, H. (2021) You want to reduce the carbon footprint of your food? Focus on what you eat, not whether your food is local, Our World in Data. Available at: https://ourworldindata.org/food-choice-vs-eating-local.

Roosen, J., Staudigel, M. and Rahbauer, S. (2022) ‘Demand elasticities for fresh meat and welfare effects of meat taxes in Germany’, Food policy, 106, p. 102194. doi:10.1016/j.foodpol.2021.102194.

Ryan, C. (2015) Petition launched for meat tax in Sweden, Food Navigator. Available at: https://www.foodnavigator.com/Article/2015/07/22/Petition-launched-for-meat-tax-in-Sweden.

Sacks, G., Kwon, J. and Backholer, K. (2021) ‘Do taxes on unhealthy foods and beverages influence food purchases?’, Current nutrition reports, 10(3), pp. 179–187. doi:10.1007/s13668-021-00358-0.

Sanders, B. (2020) Global Animal Slaughter Statistics & Charts: 2020 Update, Faunalytics. Available at: https://faunalytics.org/global-animal-slaughter-statistics-and-charts-2020-update/.

Scarborough, P. et al. (2020) ‘Impact of the announcement and implementation of the UK Soft Drinks Industry Levy on sugar content, price, product size and number of available soft drinks in the UK, 2015-19: A controlled interrupted time series analysis’, PLoS medicine, 17(2), p. e1003025. doi:10.1371/journal.pmed.1003025.

Schmidt, A. et al. (2021) ‘A food tax only minimally reduces the N surplus of Swiss agriculture’, Agricultural systems, 194. doi:10.1016/j.agsy.2021.103271.

Scottish National Party (2021) SNP Manifesto 2021: Scotland’s Future. Scottish National Party. Available at: https://www.snp.org/manifesto/.

Šimčikas, S. (2019) Rodents farmed for pet snake food, Effective Altruism Forum. Available at: https://forum.effectivealtruism.org/posts/pGwR2xc39PMSPa6qv/rodents-farmed-for-pet-snake-food.

Simmonds, P. and Vallgårda, S. (2021) ‘“It”s not as simple as something like sugar’: values and conflict in the UK meat tax debate’, International Journal of Health Governance, 26(3), pp. 307–322. doi:10.1108/IJHG-03-2021-0026.

Simon, D.R. (2013) Meatonomics: How the Rigged Economics of Meat and Dairy Make You Consume Too Much–and How to Eat Better, Live Longer, and Spend Smarter. Conari Press. Available at: https://play.google.com/store/books/details?id=PY0KUnaIU5AC.

Singer, P. (2009) Make meat-eaters pay: Ethicist proposes radical tax, says they’re killing themselves and the planet, NY Daily News. Available at: https://www.nydailynews.com/opinion/singer-meat-eaters-pay-article-1.382901.

Smed, S. et al. (2016) ‘The effects of the Danish saturated fat tax on food and nutrient intake and modelled health outcomes: an econometric and comparative risk assessment evaluation’, European journal of clinical nutrition, 70(6), pp. 681–686. doi:10.1038/ejcn.2016.6.

Soule, S.A. and Olzak, S. (2004) ‘When Do Movements Matter? The Politics of Contingency and the Equal Rights Amendment’, American sociological review, 69(4), pp. 473–497. doi:10.1177/000312240406900401.

Springmann, M. et al. (2016) ‘Mitigation potential and global health impacts from emissions pricing of food commodities’, Nature climate change, 7(1), pp. 69–74. doi:10.1038/nclimate3155.

Springmann, M., Sacks, G., et al. (2018) ‘Carbon pricing of food in Australia: an analysis of the health, environmental and public finance impacts’, Australian and New Zealand journal of public health, 42(6), pp. 523–529. doi:10.1111/1753-6405.12830.

Springmann, M., Mason-D’Croz, D., et al. (2018) ‘Health-motivated taxes on red and processed meat: A modelling study on optimal tax levels and associated health impacts’, PloS one, 13(11), p. e0204139. doi:10.1371/journal.pone.0204139.

TAPPC (2021) Increasing number of countries start taxing meat and dairy, True Animal Protein Price Coalition. Available at: https://www.tappcoalition.eu/nieuws/16831/increasing-number-of-countries-start-taxing-meat-and-dairy-.

TAPP Coalition (2020) European consumers support higher meat prices True Price Consumer Research Survey Results: France, Germany, The Netherlands. TAPP Coalition. Available at: https://tappcoalitie.nl/images/TAPP-Coalition-Consumer-Research-Survey-Results-1606202904.pdf.

The Danish Council on Ethics (2016) The Ethical Consumer: Climate Damaging Foods. The Danish Council on Ethics. Available at: https://www.etiskraad.dk/~/media/Etisk-Raad/en/Publications/Climate-damaging-foods-2016.pdf?la=da.

Thomson, R. et al. (2017) ‘The fulfillment of parties’ election pledges: A comparative study on the impact of power sharing’, American journal of political science, 61(3), pp. 527–542. doi:10.1111/ajps.12313.

Thow, A.M., Downs, S. and Jan, S. (2014) ‘A systematic review of the effectiveness of food taxes and subsidies to improve diets: understanding the recent evidence’, Nutrition reviews, 72(9), pp. 551–565. doi:10.1111/nure.12123.

Tomasik, B. (2017) Habitat Loss, Not Preservation, Generally Reduces Wild-Animal Suffering, Reducing Suffering. Available at: https://reducing-suffering.org/habitat-loss-not-preservation-generally-reduces-wild-animal-suffering/.

Tomasik, B. (2018) Climate Change and Wild Animals, Reducing Suffering. Available at: https://reducing-suffering.org/climate-change-and-wild-animals/.

Tomasik, B. (2018) How Much Direct Suffering Is Caused by Various Animal Foods?, Reducing Suffering. Available at: https://reducing-suffering.org/how-much-direct-suffering-is-caused-by-various-animal-foods/ (Accessed: 5 October 2021).

Wellesley, L., Happer, C. and Froggatt, A. (2015) Changing Climate, Changing Diets: Pathways to Lower Meat Consumption. Chatham House. Available at: https://www.chathamhouse.org/2015/11/changing-climate-changing-diets-pathways-lower-meat-consumption.

Wills, L. (2021) What happens to male chicks in the egg industry?, The Humane League. Available at: https://thehumaneleague.org.uk/article/what-happens-to-male-chicks-in-the-egg-industry.

Wirsenius, S., Hedenus, F. and Mohlin, K. (2011) ‘Greenhouse gas taxes on animal food products: rationale, tax scheme and climate mitigation effects’, Climatic change, 108(1), pp. 159–184. doi:10.1007/s10584-010-9971-x.

World Animal Protection (2020) Animal Protection Index (API) 2020, United Kingdom of Great Britain and Northern Ireland: Ranking B. World Animal Protection. Available at: https://api.worldanimalprotection.org/sites/default/files/api_2020_-_uk_0.pdf.

Yavuz, E. (2020) The Role of Political Trust on Policy Acceptability and Public Support for a Climate Tax on Meat Consumption: A Survey Experiment in Sweden and Turkey. Master’s Programme in Political Science. gupea.ub.gu.se. Available at: https://gupea.ub.gu.se/handle/2077/65475.

YouGov (2021) YouGov / Lexington Communications Survey Results. YouGov. Available at: https://docs.cdn.yougov.com/z1mtmetxbm/LexComm_PlantbasedFoods_210812_W.pdf.

The literature review was not systematic, and it was limited to English-language studies. So, there may be relevant studies that we have missed. We used both Web of Science and Google Scholar.

One exception may be Spain, which in 2011 appears to have slightly increased the value-added tax on meat and slightly decreased that tax on fruit and vegetables (TAPPC, 2021).

This Council is a body tasked with providing advice to the Danish government.