Comments

58

Making predictions is a good practice, writing them down is even better.

However, we often make binary predictions when it is not necessary, such as

Alternatively, we could make predictions from a normal distribution, such as ('~' means ‘comes from’):

While making "Normal" predictions seems complicated, this post should be enough to get you started, and more importantly to get you a method for tracking your calibration, which is much harder with dichotomous predictions.

The key points are these:

Things this post will answer:

The normal distribution is usually written as N(,) has 2 parameters:

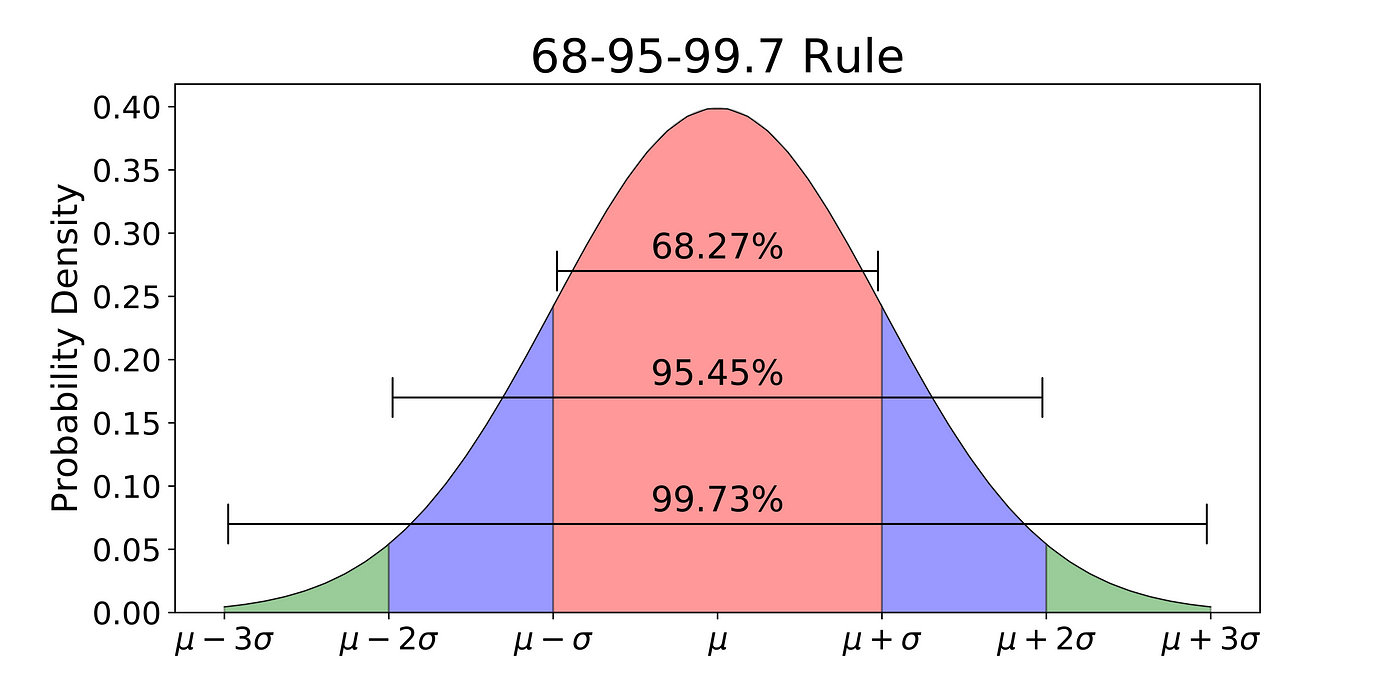

the 68-95-99.7 rule states that:

68% of your predictions should fall in

95% of your predictions should fall in

99.7% of your predictions should fall in

Finally 50% of the predictions should fall within , which can be used as a quick spot check.

To make a prediction, there are two steps. Step 1 is predicting . Step 2 is using the 68-95-99.7 rule to capture your uncertainty in .

I tried to predict Biden’s national vote share in the 2020 election. From the polls, I got 54% as a point estimate, so that seemed like a good guess for . For I used the 68-95-99.7 rule and tried to see what that would imply for different values of . Here is a table for 2-5%

| Intervals | 68% | 95% | 99.7% |

|---|---|---|---|

| 52-56% | 50-58% | 48-60% | |

| 51-57% | 48-60% | 45-63% | |

| 50-58% | 46-62% | 42-66% | |

| 49-59% | 44-64% | 39-69% |

implies a 97.5% (95% interval + tail half tail) chance that Biden would get more than 50% of the votes ); I was not that confident. implies a 84% chance that Biden would get more than 50% of the votes (68% + 32%/2), so there is 16% chance Trump wins, I likewise found this too high, so I settled on .

Biden Got 52% of the vote share, which was within 1 sigma of my prediction. There are two weak lessons that I drew from this ONE data point.

Imagine I instead had predicted Biden wins (the popular vote) 91%, well guess what he won, so I was right... and that is it. Thinking I should have predicted 80% because the pollsters screwed up seems weird, as that is a weaker prediction and the bold one was right! I would need to predict a lot of other elections to see whether I am over or under confident.

Note: In the previous section we used and for predictions. In this section we will use and where i is the index (prediction 1, prediction 2... prediction N). We will use for the calibration point estimate; this means that is a number such as 1.73. In the next post in this series, we will use for the calibration distribution, this means that is a distribution like your predictions and thus has an uncertainty.

I also made a terrible prediction, during the early lock down in 2020. I predicted N(15,000, 5,000) COVID deaths by 2022 in Denmark. It turned out to be 3,200, which is standard deviations away, so outside the 95% interval!

In this section we will transform your predictions to the Unit normal. This is called z-scoring, because if all predictions are on the same scale, then they are comparable:

Normally when you convert to z-scores you use the data itself to calculate and , which guarantee a N(0,1). Here, we will use our predicted and . This means there will be a discrepancy between and our . This discrepancy describes how under/over confident your intervals are, and thus describes your calibration, such that if = 2 then all your intervals should be twice as wide to achieve

First we z-score our data by calculating how many they are away from the observed data , using this formula:

Second we calculate as the RMSE (root mean squared error) of all predictions:

And that is, let's calculate for my two predictions, first we calculate the variances:

Then we calculate

So if these were my only two predictions, then I should widen my future intervals by 73%. In other words, because is 1.73 and not 1, thus my intervals are too small by a factor of 1.73.

Here are some bonus arguments:

Sometimes your beliefs do not follow a Normal distribution. For example, the Bitcoin prediction N(3000, 1500) implies I believe there is a 2.5% chance the price will become negative, which is impossible. There are 3 solutions in increasing order of fanciness to deal with this:

This means if it's above then , while if it's below then . If you do this, then you can use "the relevant " when calibrating and ignore the other one, so if the price of bitcoin ended up being then z becomes :

z-scoring works the same way, so if the Bitcoin price was 10.000 then:

I want you to stop and appreciate that we can get a specific actionable number after 2 predictions, which is basically impossible with binary predictions! So start making normal predictions, rather than dichotomous ones!

As a final note, keep this distinction in mind:

Getting good at 1 requires domain knowledge for each specific prediction, while getting good at 2 is a general skill that applies to all predictions.

This post we calculated the point estimate based on 2 data points. There is a lot of uncertainty in a point estimate based on two data points, so we should expect the calibration distribution over to be quite wide. The next post in this series will tackle this by calculating a Frequentest confidence interval for and a Bayesian posterior over . This allows us to make statements such as: I am 90% confident that , so it's much more likely that I am badly calibrated than unlucky. With only two data points it is however hard to tell the difference with much confidence.

Finally I would like to thank my editors Justis Mills and eric135 for making this readable.

Worth noting that Metaculus has the ability to record continuous distribution predictions, including both normal predictions and much more complicated distributions. E.g. https://www.metaculus.com/questions/5301/a-city-exodus/

If you want to record your predictions for your own questions on Metaculus you can also create private questions here. https://www.metaculus.com/questions/create/