Comments

This post is co-authored with Ben Garfinkel. It is cross-posted from the CEA blog. A PDF version can be found here.

Summary: Some strategic decisions available to the effective altruism m...

Summary

The U.S. workforce is shrinking due to demographic decline and no government on Earth formally tracks its robotic labor capacity. I propose the National Autonomous Work Index (NAWI) — a metric measuring total productive robot work-hours, like how we track GDP or the unemployment rate. Without it, we are flying blind into the largest labor transition in history: unable to manage displacement pace, unable to allocate energy infrastructure, and unable to direct automation toward high-impact sectors like factory farming and elder care. This post argues the physical automation transition is important, neglected, and tractable — and that the EA community is well-positioned to push for the measurement infrastructure before the window closes.

In 2025, U.S. employers announced 1.09 million job cuts — a 65% increase from 2024 — with warehousing layoffs up 378%.1 Automation was cited as the primary driver.

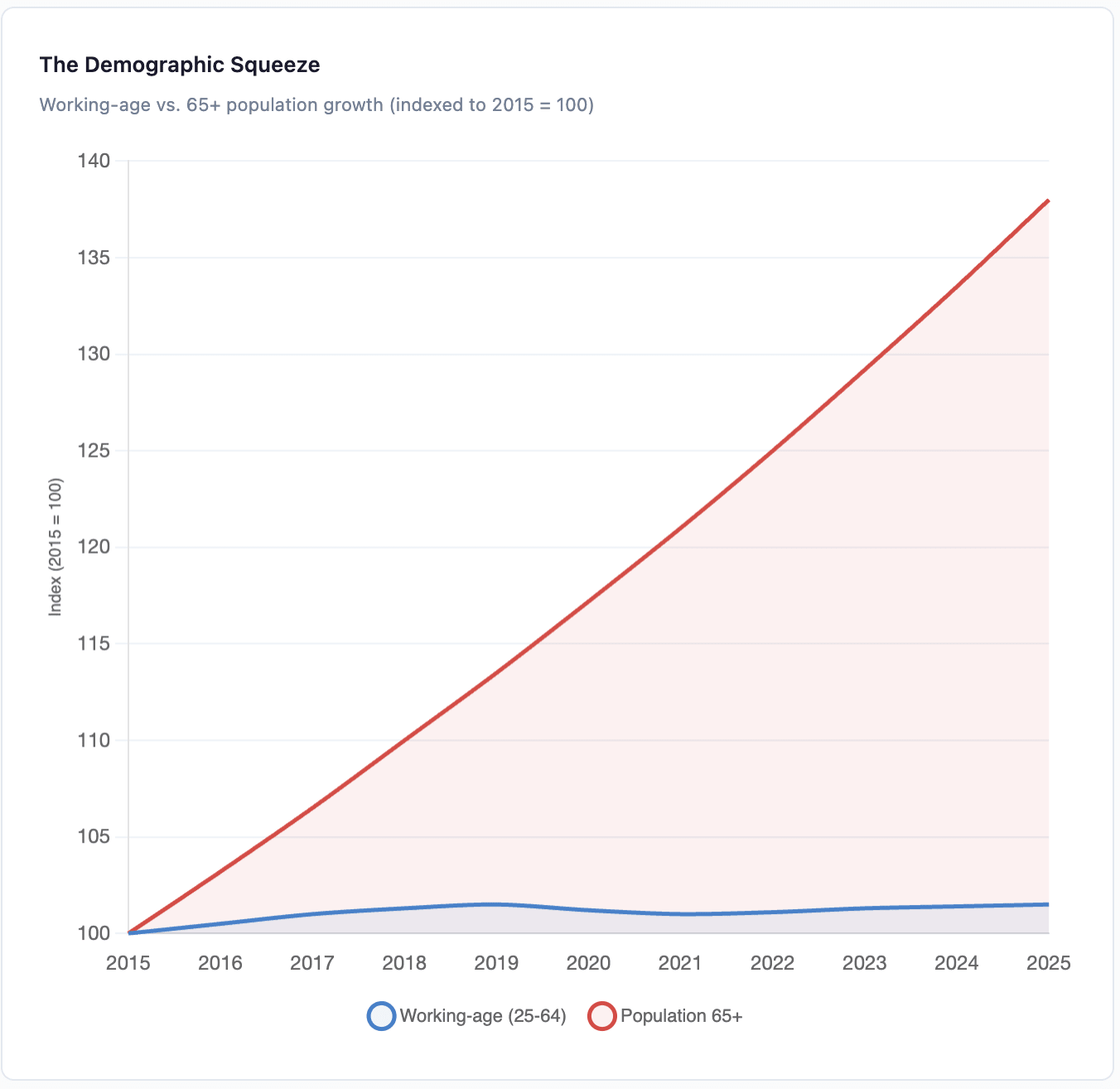

Meanwhile: workforce participation remains 1.7 million workers below pre-pandemic levels. The 65+ population is growing nearly five times faster than the working-age population. Birth rates are below replacement. Immigration has declined.2

These trends are not contradictory — they're the same phenomenon. Sectors facing acute labor shortages (warehousing, manufacturing, elder care, agriculture) are automating fastest because humans are unavailable. Automation is not primarily replacing workers. It is filling a demographic vacuum.

And yet: no government on Earth formally measures how large this robotic labor force is, how fast it's growing, or what share of the economy it can cover. Imagine trying to run monetary policy without measuring unemployment. That is where we are with the automation transition.

The EA community has built serious infrastructure for AI software risk. But the physical automation transition — robots in warehouses, on farms, in slaughterhouses, in care homes — has almost no equivalent policy infrastructure, despite affecting far more workers in the near term.

Three connections to existing EA priorities:

Animal welfare. Factory farming persists partly because alternatives can't match its cost structure. Robotic automation of protein production — from cultivated meat bioreactors to automated vertical farming — is one of the most plausible pathways to making animal agriculture economically obsolete rather than just morally unacceptable. But this requires a physical robot fleet at scale, which requires the energy and deployment infrastructure this framework addresses. If you care about reducing animal suffering, you should care about how fast the robotic labor force scales.3

Global catastrophic risk resilience. A national autonomous workforce acts as a strategic reserve — analogous to the Strategic Petroleum Reserve. During pandemics, natural disasters, or geopolitical disruptions, robotic labor capacity determines whether supply chains survive or collapse. COVID showed what happens when human labor disappears overnight. A measurable, deployable robotic workforce is a resilience asset.

AI governance. The EA community debates AI governance primarily through the lens of software capabilities — alignment, misuse, power concentration. But the physical deployment of AI through robots creates a parallel governance challenge: who controls the robot fleet controls the labor supply. Without measurement infrastructure, this concentration happens invisibly.

The proposal is simple. Just as we measure GDP, unemployment, and labor force participation, we should measure national autonomous work capacity:

NAWIt = Σ ( Ni,t × hi,t × φi,t )

| Variable | Meaning | Range |

|---|---|---|

| Ni,t | Robot stock (operational units of type i) | Count |

| hi,t | Annual utilization hours per unit | Hours/yr |

| φi,t | Task substitution factor (generality) | 0.5 – 1.0+ |

Output: autonomous work-hours, convertible to human full-time equivalents. This makes it directly comparable to labor statistics the BLS already publishes.

Concrete example:

1 million robots × 6,000 hrs/year × 0.8 task factor = 4.8 billion autonomous hours ≈ 2.5 million human FTEs. That is roughly the size of the current U.S. labor shortfall.

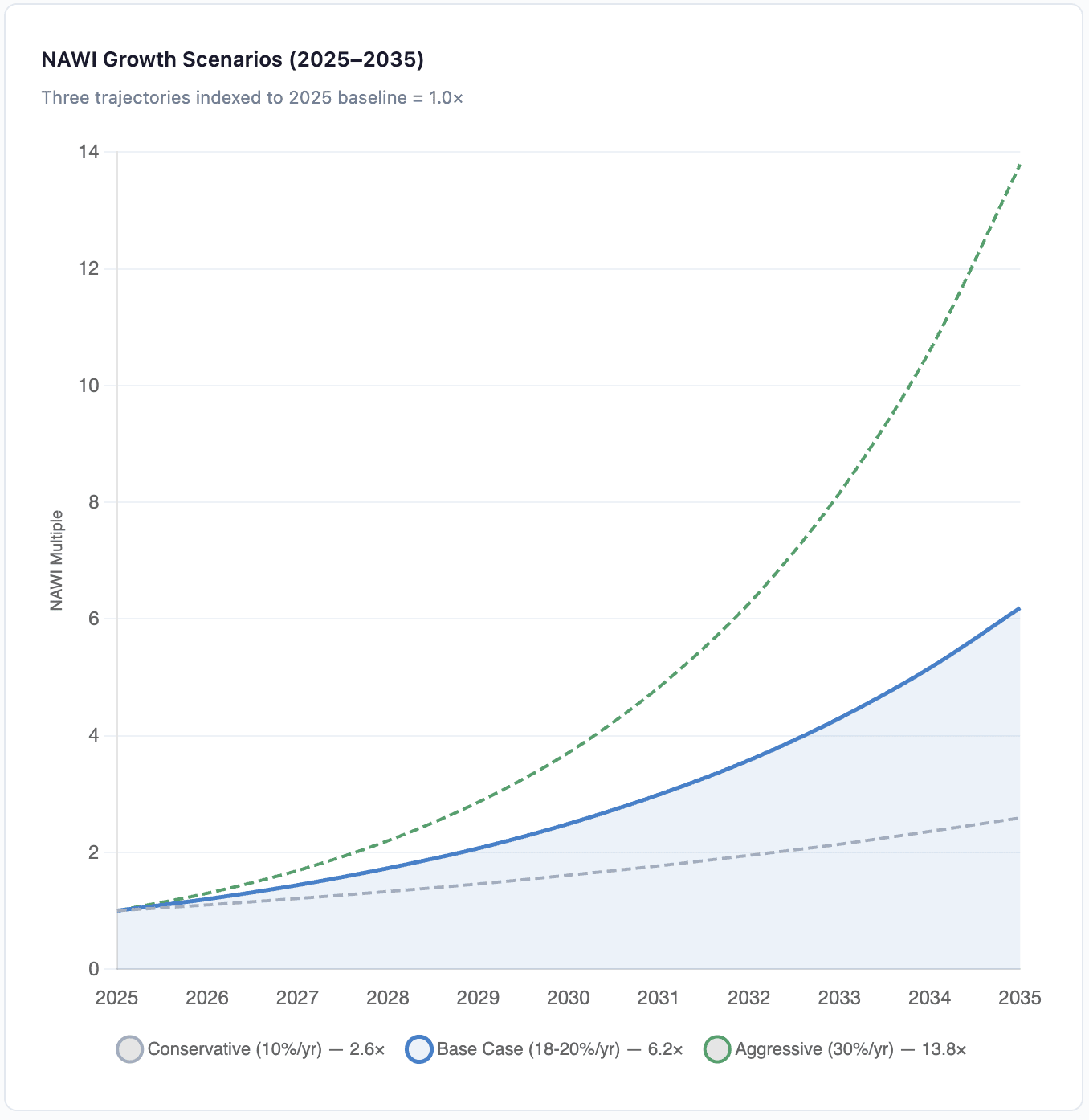

NAWI Growth Scenarios (2025–2035)

Three trajectories indexed to 2025 baseline = 1.0×

The base case (18-20% annual growth, reflecting current industry trajectories) reaches 6.2× by 2035 — enough to offset the demographic labor gap with ~1% additional GDP growth by the late 2030s. The aggressive scenario (30%/yr, requiring national-level commitment) reaches 13.8× but carries serious displacement risk. The conservative scenario (10%/yr) is insufficient to offset the aging workforce.

But these curves assume no binding constraints. Two factors can cap growth well below potential:

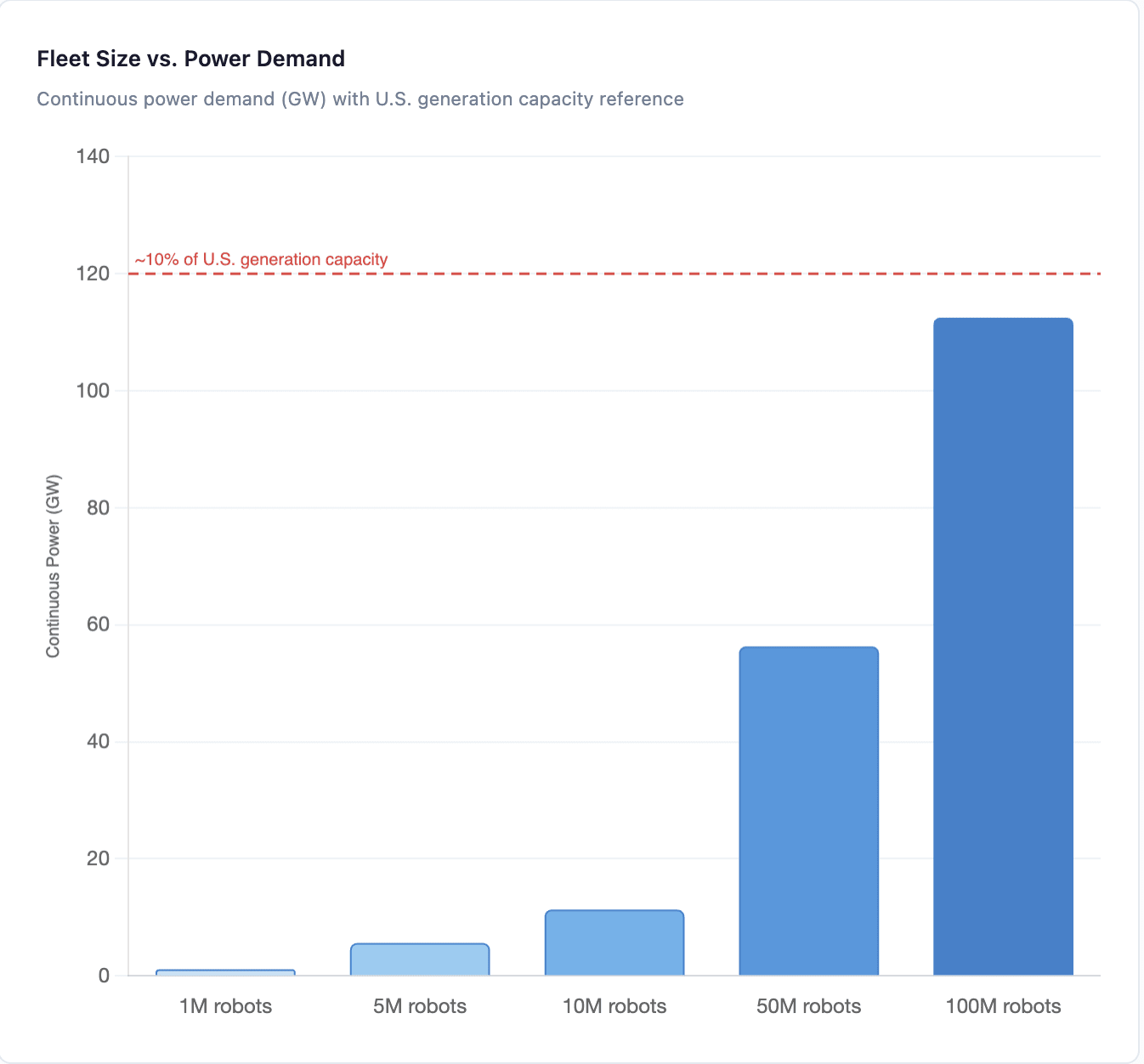

A humanoid robot draws ~1.125 kW continuously (~10 MWh/year). At 10 million robots, that's 11.3 GW — roughly 2% of U.S. generation capacity. At 100 million, it's 10%. The U.S. already faces a ~44 GW shortfall for data centers. Adding a robotic fleet compounds this.

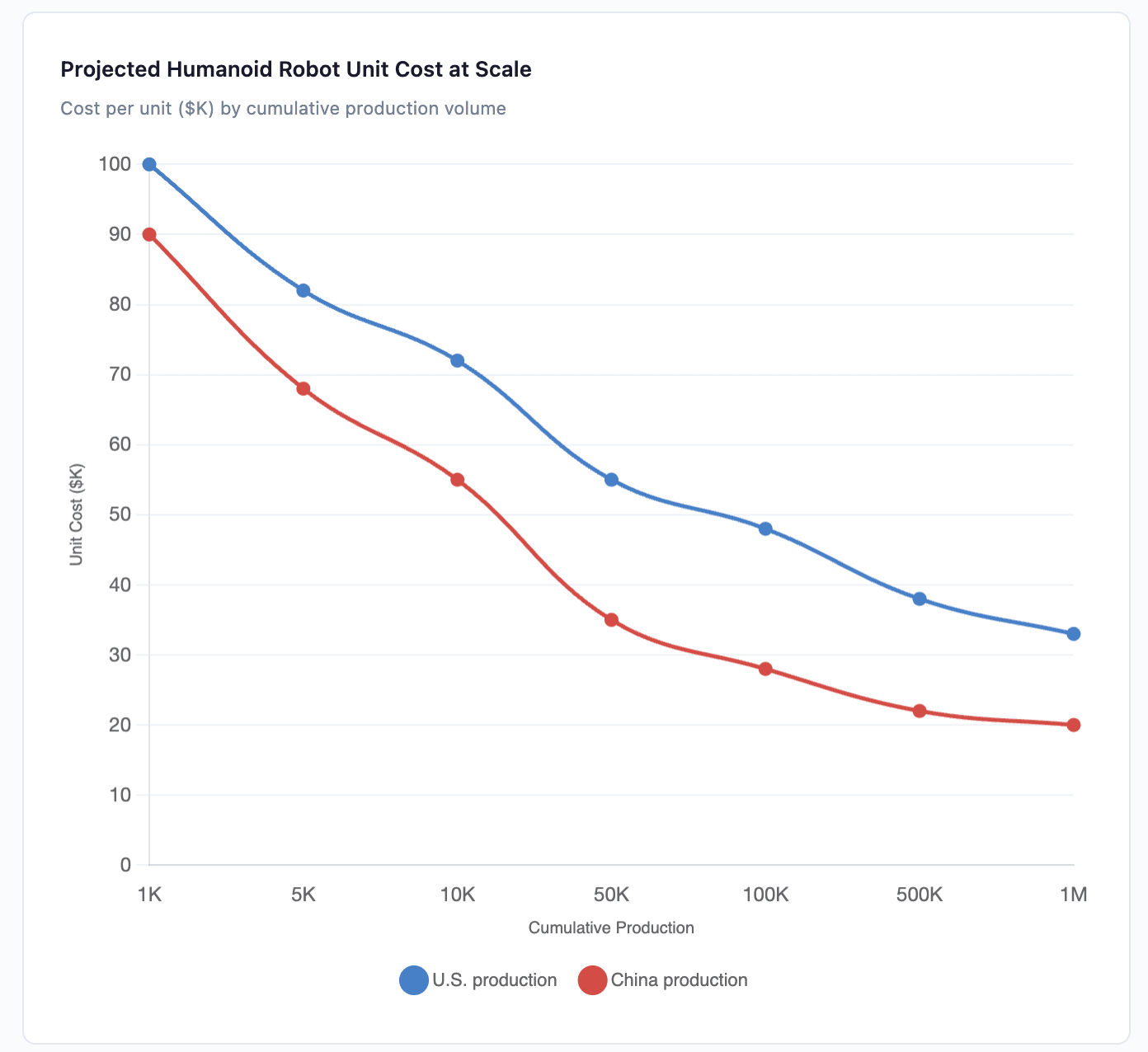

An advanced humanoid costs ~$100K today. At Chinese-scale production (1M+ units), costs could reach $20-25K — below a Chinese factory worker's annual wage. U.S. production: $60-80K at scale, competitive with U.S. labor when amortized.

| Volume | U.S. Production | China Production |

|---|---|---|

| 1K | $100K | $90K |

| 10K | $72K | $55K |

| 100K | $48K | $28K |

| 1M | $33K | $20K |

The cost trajectory matters for the U.S.-China dynamic. China is pursuing aggressive production scaling with fewer regulatory constraints and faster infrastructure buildout. The country that builds robotic labor capacity faster gains a compounding advantage in economic output and geopolitical leverage.

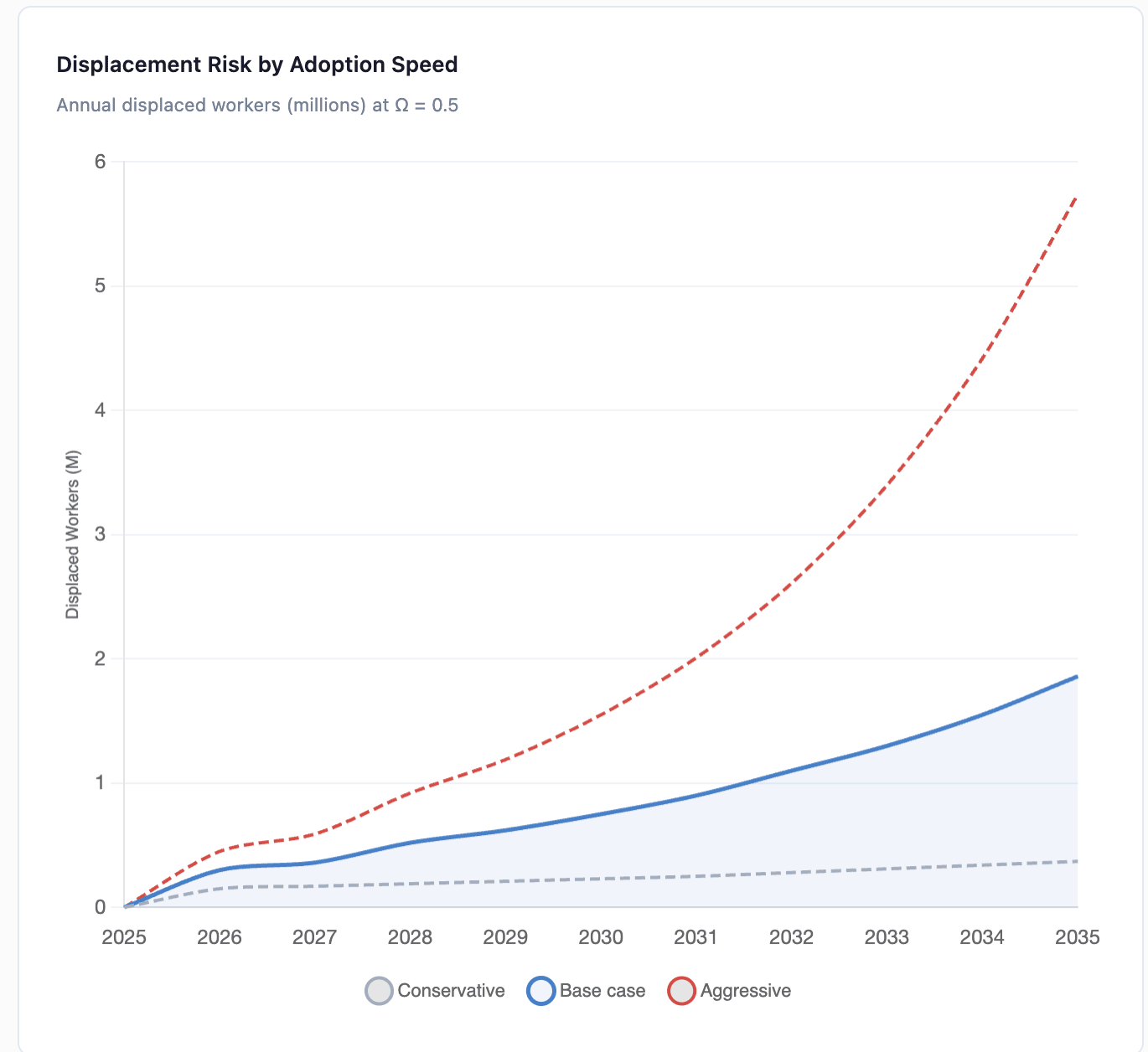

I want to be direct about something most robotics advocates understate: this transition creates real losers. The NAWI framework explicitly quantifies this through a displacement rate equation:

Dt = ( ΔAWNt × Ω ) / Ltotal

Where Ω is the task overlap coefficient (how much new robot capacity replaces vs. supplements human jobs). Natural workforce attrition absorbs ~3%/year (~4.5M workers). Stay below that threshold and the transition manages itself through retirement. Exceed ~10% annual displacement (~15M workers) and you get a destabilizing shock equivalent to COVID-era layoffs.

| Year | Conservative | Base Case | Aggressive |

|---|---|---|---|

| 2027 | 0.17M | 0.36M | 0.59M |

| 2030 | 0.23M | 0.75M | 1.55M |

| 2033 | 0.31M | 1.30M | 3.40M |

| 2035 | 0.37M | 1.86M | 5.74M |

The base case stays manageable. The aggressive case approaches danger by the early 2030s. The entire point of the NAWI is to have this data before we need it — so policymakers can throttle adoption pace deliberately rather than reacting to mass unemployment after the fact.

I also want to flag a structural risk: the depreciation trap. A humanoid robot's physical lifespan is 7-10 years, but its economic lifespan may be just 18-24 months as AI improves. This creates a treadmill where fleet operators must constantly reinvest, favoring extreme centralization. The likely outcome is "Cloud Labor" — a handful of operators serving the entire market, like AWS for physical work. The Gini coefficient of labor capital could reach levels far above today's income inequality.

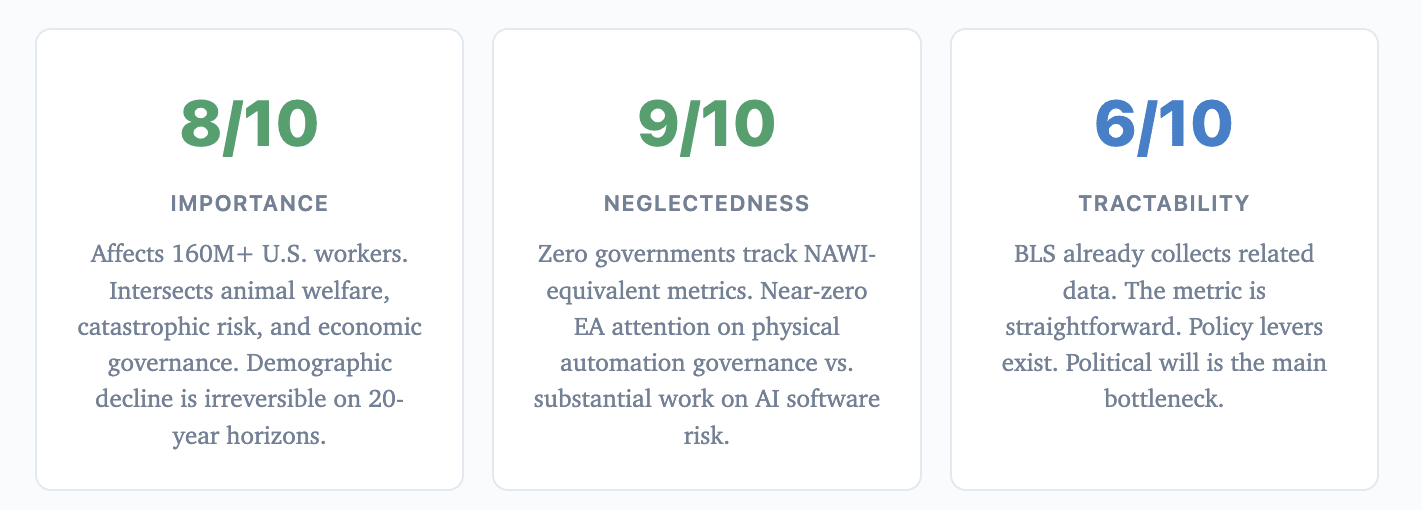

ITN assessment

The strongest case here is neglectedness. Search this forum for "robotics policy" — you will find almost nothing. Meanwhile, the physical automation transition is accelerating in real time. This is a gap where small investments in measurement and policy design could have outsized returns.

Anticipating objections

"Isn't this just industrial policy? Why does EA need to be involved?"

Industrial policy is happening regardless — see the CHIPS Act, IRA energy subsidies. The question is whether it happens with measurement infrastructure or without it. EA's comparative advantage is pushing for the metrics and evidence base that make policy less bad. The NAWI is not an argument for more spending; it's an argument for knowing what's happening.

"AGI will arrive before physical robots matter. This is moot."

Maybe. But if AGI timelines are 5-15 years (the median EA view), there is a substantial period where AI is highly capable but not superintelligent, and physical labor automation is the primary economic transformation. Even Aschenbrenner's Situational Awareness scenario describes a period where AI directs human/robot labor before full autonomy. That transition period needs governance.

"The task substitution factor (φ) is too uncertain to build policy around."

Agreed — φ is the weakest parameter. But the BLS publishes unemployment estimates with substantial measurement error and policymakers still find them useful. Imprecise measurement beats no measurement. Starting with φ = 0.5 for industrial robots and refining empirically is better than the current state (φ = undefined, N = unknown).

What should happen

Measurement first. BLS (or equivalent agencies) should publish NAWI-equivalent data quarterly. You cannot manage what you do not measure.

Displacement guardrails. Peg maximum deployment growth to a multiple of natural workforce attrition. When growth exceeds the threshold, automatically trigger transition support (wage insurance, retraining, geographic mobility subsidies) funded by a per-robot-hour actuation levy.

Energy pre-allocation. Dedicate 10-20 GW of new generation for industrial automation. Fast-track small modular reactors near industrial parks and pre-authorize "robotics corridors" with streamlined grid permits.

Direct automation toward high-impact sectors. Prioritize deployment subsidies for factory farming alternatives, elder care, and disaster response — sectors where the humanitarian and animal welfare returns are highest and labor shortages are most acute.

For people working on animal welfare: how much does the physical automation timeline matter for cultivated meat / alternative protein scaling?

The core argument is modest: we should measure national robotic labor capacity the same way we measure GDP and unemployment. The NAWI doesn't predict whether automation is net positive or negative. It is the measurement infrastructure that lets us steer the outcome. And right now, no one is building it.

The full technical framework — including energy ceiling models, RaaS valuation, depreciation dynamics, and cost elasticity analysis — is at liquid-labor.com. I welcome engagement, especially pushback.

Disclosure: I invest in robotics and energy infrastructure (including Apptronik) through Turing Strategy. The policy framework I propose would benefit the robotics industry. You should weigh my arguments accordingly.