For this post I sought help with the title. The advice I was given was:

Don't mention "Universal Ownership" in the title -- that term is meaningless to people; it should be mentioned and explained in the article itself

The title should make one clear point

This post talks about really exciting ambitious ideas and the title should convey that, since the ambitiousness of the potential impact is the one thing that someone should take away from this, that's what the title should convey

Someone suggested that wording to me and but it was I who opted to use it. So if the title is a mistake, it's my mistake.

People of the same trade seldom meet together, even for merriment and diversion, but the conversation ends in a conspiracy against the public, or in some contrivance to raise prices.

It is impossible indeed to prevent such meetings, by any law which either could be executed, or would be consistent with liberty and justice. But though the law cannot hinder people of the same trade from sometimes assembling together, it ought to do nothing to facilitate such assemblies; much less to render them necessary. A regulation which obliges all those of the same trade in a particular town to enter their names and places of abode in a public register, facilitates such assemblies. . . . A regulation which enables those of the same trade to tax themselves in order to provide for their poor, their sick, their widows, and orphans, by giving them a common interest to manage, renders such assemblies necessary. An incorporation not only renders them necessary, but makes the act of the majority binding upon the whole.

– The Wealth of Nations, Book I, Chapter X.

I think this post misses the largest downside of the proposal, which is the undermining of competition.

At the moment, companies generally attempt to maximize their own profits. This means trying to operate as efficiently as they can, attract talented workers, and sell products that people want to buy. Competition between firms helps ensure that we minimize the use of costly inputs, pay workers concordant with their marginal product, and design new products that match what consumers want. It is, in general, a naturally regulating system that produces largely good outcomes without the need for external micro-management.

The Universal Ownership proposal is that firms should try to maximize the profitability, not just of themselves, but of the entire portfolio that their investors own.

I am skeptical of many of your proposed benefits. For example, you suggest that "investors ... owning the coal companies [would get] them to implement a policy of no new plants." But coal companies, which are responsive (at least in theory) to investors typically do not run power plants, and they sell a commodity. Power plants are run by electric utility companies, who are highly regulated. It does not matter if 100% of the investors in a utility demand it close down a coal plant: if their regulator likes the coal plant, they must keep it running. Worse, almost half the new coal plants being built are in China, a country where western investors have few rights and almost no influence.

But more importantly, I think you miss that the most obvious action if companies were to try to boost their collective, not individual, profitability: collusion. The largest externality companies have is their pecuniary externality on competitors. In an industry with 10% margins, if all the competitors decided to work together to raise prices by 'just' 10%, profits would double. Similarly, they could agree to not bid up wages, or to all ease up on R&D. Normally, they wouldn't be able to do this, because they're each incentivised to 'defect', cut prices, and gain market share - but that protection is gone if they are effectively all working together. This seems like a much more significant benefit to the investor that the somewhat nebulous and second-order impact of reduced CO2 emissions, where they capture only a small fraction of the benefit.

Of course, if this were to happen, I would expect governments to impose new regulations. Governments tolerate free markets largely not because of an ideological belief in liberty but because they think that companies competing produces good outcomes. If we replace this with a cartel system, where companies work together to promote the interests of their owners as a class, this will change. (I also think more founders would refuse to allow public investors control over their firms).

Overall, I think this proposal is basically trying to abuse a possible flaw in our system of economic governance, and only appears attractive by focusing the less likely but more desirable outcomes that motivated it, rather than the outcomes which have the strongest economic link to the proposal. But if people start to abuse this flaw en masse I would expect regulations to close it anyway.

Thank you for this -- I have discussed this with many people and not heard this competition critique before, and I'm always glad to encounter a novel critique.

I'm not sure I understand it though.

Are you saying that if Universal Ownership took hold, companies would collude to raise prices (or otherwise damage customers for their own benefit)?

I'm not clear on why Universal Ownership makes a difference here -- it's already in companies' interests to form cartels, and there's already regulation to stop it.

I have discussed this with many people and not heard this competition critique before

I'm surprised to hear that. This is an economics 101 level critique. You are proposing moving from a competitive situation to something equivalent to a monopoly, and it is basic microeconomics that monopolies charge higher than other market structures. Their redeeming feature is economies of scale, but that is not present when it is just rival firms colluding to act as if they are a monopoly without actually combining their supply chains.

I'm not clear on why Universal Ownership makes a difference here -- it's already in companies' interests to form cartels,

If each company is maximising its own profit, when raising prices they have to balance an increase in profit-per-unit against a reduction in total units sold from competitors taking share. This is a natural check against the tendency to raise prices.

However, if they are instead maximizing profit for the industry (or the universe of public companies) as a whole, this is not the case: they still get the benefit of higher profit-per-unit, but the loss of market share is instead neutral, because competitors will benefit. As such, companies will raise profits until consumers stop buying units from anyone at all, a much higher price level. As such the incentive to increase prices like a cartel is increased.

If you want you can show this using standard supply-and-demand diagrams.

and there's already regulation to stop it.

Many existing regulators will generally not work against the sort of advanced collusion you are recommending. Your proposed system does not, for example, require any mergers, or agreements between competitors, or exclusive dealing, or many other standard techniques that antitrust goes after. This is why competition regulators have been concerned about the dangers of this approach.

As I've alluded to in another comment, I think you're missing part of the model. If you incorporate UO considerations, you would have two further perspectives to incorporate:

Your model now includes the company's competitors, who also benefit from collusion

Your model also includes the rest of the economy, which is damaged by the collusion

It is not immediately clear to me which of these would win. To a first-order approximation, it may appear that the two effects are roughly offsetting, since the cartel likely moves money from the rest of the economy to the cartel members in what might simplistically be treated as a zero sum game. To add more detail to the model, it would be worth considering that the cartel essentially constitutes a form of rent-seeking, which is generally considered by economists to be bad for the economy, which suggests that item 2 likely outweighs item 1 (i.e. maybe makes the Universal Owner less keen to take part in a cartel). I won't keep on adding more and more details to the putative model.

I think the bottom line here is that companies currently have incentives to collude, and those incentives may still survive under a Universal Ownership system.

Your point about the mechanism of that collusion is a good one. Regulations currently anticipate ways to forbid anti-competitive behaviour, and likely don't already anticipate a UO-driven mechanism, so the regulations would have to evolve. It's worth bearing in mind that if this concept does reach the companies themselves (not just investors) then it will take many years, and so there will be plenty of time for this regulatory adaptation to occur.

Thanks for writing this up, I've been super interested in this since Matt Levine started discussing asset managers like BlackRock having an impact through their climate related investing strategies. It would be so great if this would turn out to be a mechanism to coordinate patient and safe AI development among AI companies and governments.

Random things:

recent working paper finding that big asset managers are currently voting against environmentally friendly actions [Tweet] (I suppose it's likely that with discount rates & predominant investment in regions relatively less affected by climate change, this might be profit maximizing even as a relatively universal owner)

A fine-gained analysis shows that the combined voting decisions of the Big Three are more likely to lead to the failure of environmental resolutions and that, whether they succeed or fail, these resolutions tend to be narrow in scope and piecemeal in nature

somebody mentioned that it might be surprising that those big money asset managers didn't seem to get much involved in Covid, e.g. by making investments in vaccine research and rollouts, as they internalized a big chunk of the economic fallout

I wondered how much less promising this strategy is for coordinating with Chinese firms, as I have the superficial impression that investors have much less influence there

The tweet you linked to cites a paper which looks really good and highlights the fact that ESG is not high impact now. Thanks.

I think your point around COVID is an interesting one. I guess one of the complications with COVID is that it initially did cause markets to tumble, but they then recovered rather handsomely, which risks skewing the incentives. (I discussed why this might have happened in sections 4.3 and repeated this in section 11.3 of this post).

Your query about China is a good one. In principle, UO should be appealing to Chinese investors too -- it requires no altruism on the part of the investor, it only requires the investor to want to maximise the returns across the whole portfolio... that said, I suspect it may well fail to reach certain corners of the investor universe, and China may well be one of them. In section 6, I discuss the extent to which this concept may work without covering all investors. I was going to add more in there about the international dimensions to this, but the post is long enough as it is! It's interesting to note though, that at least with regard to coal, the biggest sources of lending finance to new coal plants are Japanese (source: p8 of this Boston Uni report) My intuitive guess is that it would be easier to get these ideas to take hold in Japan than in China (indeed, I believe that Japan's government pension scheme is already interested in Universal Ownership)

As MaxRa suggest MattLevine has been speaking about this idea from time to time * and so I do think mainstream finance is at least some what aware.

I feel sure you are aware, but in case not, Ellen Quigley has written about this alot (Cambridge centre for existential risks). (I didn't see her work mentioned as I read your paper, but I read it quite quickly).

Thanks for writing up this idea! I think the risk management aspect of ESG is important, and this could definitely be a step in the right direction.

My main concern is that I am not sure how likely it is that there is a clear path to get investors to adopt Universal Ownership, it is not something I had heard of before. It seems to me the amount of risk reduction in the portfolio a single investor, caused by their individual marginal divestment/shareholder activism from a company with negative externalities would be quite small, so it would really only work if at least a majority of investors adopted a Universal Ownership model. Are there many investors who are adopting or taking this seriously already?

Also, to get a truly accurate pricing of externalities to maximize public/social good, each investor would ideally model and internalize the effects of externalities on ALL of society, not just their own portfolio, which would only incentivize them to consider a small fraction of the actual value investors and companies could provide to society. I realize this would be an even bigger ask of investors, but my hope is that there is an alternative social stock market or public goods market that systemically, financially rewards positive externalities and taxes negative externalities by design.

That said I could be wrong, would definitely be excited to see something like this gain more traction as it would be much better than what we currently have and I think it is possible something like this could gradually become more popular, especially if there was at least a small but reliable increase in value for investors by better accounting for risk which outweighs costs of modeling and is not countered by displacement effects.

Thanks for this. Your main concern is a very reasonable one.

To my mind, there is (at the moment) no clear path to get investors to adopt UO, and most of them have not heard of it before. There are someasset owners who have adopted it, but they are very much the exception, not the rule.

While these challenges definitely do reduce the probability of success of this project, it also increases the impact.

The counterfactual is that without this work, it would be highly unlikely that this would happen anyway.

I also agree that pricing externalities well is really hard.

Things that help here are:

the standard approach to modelling externalities is to do no modelling at all -- so if we aim to outperform the existing models, we only have to produce a model which is better than nothing;

the financial system has successfully attracted lots of talented people -- with enough time, getting lots of talented people to think about these problems should hopefully allow us to do a better job (maybe even a good job) of creating such models

having a group of people with their fingers in every pie is good because it makes them care about the whole world.

and having a group of people with their fingers in every pie is bad because it will lead to anti-consumer anti-competitive corporate governance interventions.

having a group of people with their fingers in every pie is bad because it will lead to anti-consumer anti-competitive corporate governance interventions.

It's not clear to me that this is true.

If an investor has a finger in every pie, then it will mean that they are invested in a company and also that company's competitors...

... but this doesn't seem that important -- they had an incentive to create cartels, Universal Owner or no.

What it does mean is that they are also invested in the company's consumers -- i.e. if one company acts to harm all consumers, this too will harm the wider economy and hence (for a universal owner) the wider portfolio.

So if anything, it seems that the opposite is true.

What it does mean is that they are also invested in the company's consumers

No, public markets investors are not invested in e.g. McDonald's consumers, because McDonald's customers are natural persons and slavery is illegal. Since natural persons are the end point of consumption this is a very large omission. Less importantly, private companies, state owned enterprises, co-ops, sole proprietorships are also excluded.

I fear there may be a misunderstanding here, let me try to explain this more clearly.

Public markets investors largely are invested in the company's customers.

There are two cases:

The customers are corporate bodies

The customers are individuals

If the customers are corporate bodies, then a universal owner almost certainly is directly invested in them.

If the customers are individuals, then a universal owner is invested in them in a natural language sense, rather than a finance sense. I.e. they don't own a legal stake in the person, but they are invested in them in the sense that they have incentives to see them being better off.

Why?

Let's illustrate with the McDonald's example

Imagine that McDonald's decided to conspire to ensure that they somehow got the same number of meals sold, but everyone had to pay more (e.g. by some sort of collusion with other food/restaurant providers).

Then everyone outside of the restaurant/food sector would be worse off (this is the heart of your concern).

If they are worse off, they have less savings (bad for the banking sector) and spend less on trinkets/holidays/other things (bad for the trinkets/holidays/other things sectors).

In other words, benefiting McDonald's at the expense of the wallets of the general public is bad for the wider economy.

The upshot: the impact on the wider economy may make Universal Owners less likely to want to form cartels

If I think of myself as being purely an investor in McDonald's (i.e. no UO thinking):

A McDonald's cartel means more money comes to McDonald's --> MORE PROFIT

If I employ UO thinking, then there's two factors:

A McDonald's cartel means more money comes to McDonald's and the other cartel members --> MORE PROFIT

A McDonald's cartel means the wider economy is worse off, which means the other companies in my portfolio perform worse --> LESS PROFIT

Is item 2 big enough to outweigh item 1? I don't know -- I haven't done the modelling. But what I can say is:

Without UO, the incentive to form a cartel is still there

With UO, investors now incorporate factors which may push in the direction against cartels

Cartels are an example here, and could be substituted with anything that has the property that collusion between companies leads to benefits to them at the expense of the economy as a whole

If an investor has a finger in every pie, then it will mean that they are invested in a company and also that company's competitors...

Blackrock generally are that way, although I don't know whether they actually intervene in governance decisions as often as people sometimes fear. I'd guess there are a lot of industry-specific ETFs that intervene more often than they do though?

... but this doesn't seem that important -- they had an incentive to create cartels, Universal Owner or no.

Yeah I guess I'm not saying UO will make this worse, more that there could be a deeper problem that also afflicts UO.

What it does mean is that they are also invested in the company's consumers

Every industry is aligned with its consumers' interests in some ways and opposed in others. I wasn't denying the presence of aligned incentives... it's not obvious to me which is the stronger force and in what circumstances.

This is a crosspost from the new Animal Welfare Alignment Newsletter by Anima International. You can subscribe on Substack if you are interested in following these efforts. Audio reading also available on Substack.

The goals of this post are to:

1. Raise a question I see as crucially important to the goal of aligning AI to animal welfare...

“How long have you been v*g*n?”

This is one of the most common icebreakers at animal protection events. It’s a baseline assumption, and it mostly holds true: if you’re out advocating for animals not to be tortured or abused, realistically these days you are v**n, or close. And it makes for good conversation. It seems fairly safe to assume when you meet strangers.

But this assumption is hurting the movement in a way which we don’t always notice: someone new comes into the sp...

Summary

Back in November 2023 I posted here to launch Spiro and raise our first $198k. Two and a half years later this is an update and a fundraiser for the next step.

The short version: we've now reached over-5,900 people with TB preventive medicine, including over 3,000 children under five years old. Our early results have held up well an...

[All views are my own, and not necessarily those of any organisation I'm affiliated with]

0. Intro vignette

Imagine the year is 2045. Humanity has:

Solved the technical aspects of AI alignment, and most of the major companies developing AI are fully bought into ensuring that those solutions are built into any AI they produce;

Massively improved the safety of BSL4 biosecurity labs, and taken other measures to significantly reduce the risk of pandemics, especially the most severe ones;

Mostly halted fossil fuel usage, and made massive investments in clean energy.

In this post, I argue that we might be able to achieve outcomes as good as this by working on the financial system. Specifically, I believe an outcome like this is the 95th percentile outcome (i.e. realistic best case scenario) for some work relating to a concept called “Universal Ownership”, which relates to an area of finance called “ESG”, which stands for Environmental, Social and Governance.

1. Background

The financial markets have the potential to be incredibly important for the future of humanity and non-human animals.

At the moment, when investors from the world of mainstream finance make investment decisions, they are mostly deciding based on the amount of profit to be made. It is unheard of for substantial asset owners like life insurers or pension schemes to quantitatively model the externalities of companies they invest in (e.g. they don’t model the social cost of carbon). They don’t use those externality models to guide decisions about which assets to invest in or how to steward those assets.

There are reasons for this. Institutional asset owners are obliged to consider their fiduciary duties, which is often interpreted to mean that they are obliged to maximise financial returns.

This makes it harder to have a trade-off between financial returns and real-world impacts.

However, even considering these fiduciary duties, it is possible to model and incorporate externalities, *and* provide incentives for asset owners to take strong action to achieve real world impact.

This can be done using a concept called Universal Ownership. This concept is novel to most people in mainstream finance today.

Under this Universal Ownership approach, asset owners model the externalities from the companies/assets they invest in, ignore the lion's share of those externalities, but at least consider the extent to which the externalities will impact *the rest of the asset owner's own portfolio*.

This approach has a number of interesting features:

- although this model does ignore most of the externalities, it can still be sufficient to justify taking strong actions, especially for the most material risks

- the approach involves actually modelling and quantifying externalities; this sort of modelling is not currently standard

- the incentives are aligned: the approach motivates asset owners to actually have impact and change companies/entities for the better; if they only paid lip service to doing good ("greenwashing") then this would violate the assumptions of their models, and the “greenwashers” would pay for their error.

This document will echo a number of concepts outlined in earlierposts. The core of the ideas is essentially unchanged since then; this post aims to further elaborate on that thinking. Specifically it will:

Reiterate the core concept outlined in the earlier posts

Set out more detail about what the models might look like in practice

Explore in more detail some of the potential failure modes

Set out next steps, including the further research needed

There is currently a funding gap to conduct the research that is still needed.

2. Why is now the right time to act

At the moment the concept referred to as “ESG” (which stands for Environmental, Social and Governance factors in finance) has absolutely mushroomed. As someone currently working in finance in London, I know that ESG is currently very topical.

Examples, mostly based on my experience in the UK:

Major financial institutions are being required to take part in TCFD, which is a set of requirements around climate disclosures

The Bank of England has released a set of requirements for some of the larger financial institutions to take part in CBES or Climate Biennial Exploratory Scenarios

The Bank of England has also set out several regulatory requirements on the topic of ESG/climate

I have been working in finance since 2003, and I judge this moment to be particularly “hingey”. The concept of ESG is still new to many asset owners, and they are still open to alternative ideas. In a few years’ time, I expect many of the systems and processes will have been bedded down. There will be new priorities, and people’s capacity to adopt new approaches to ESG will be diminished.

3. How does Universal Ownership work

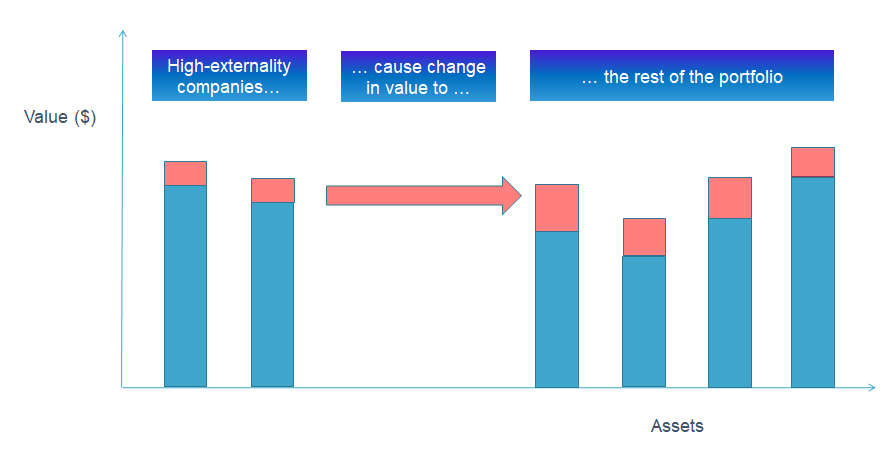

In the diagram below, each column represents an asset in your portfolio. “You” could be any materially sized asset owner, e.g. a pension scheme or a life insurer (or conceivably an ultra high net worth individual).

For example, one column might be shares in Walmart, another might be shares in Facebook, another might be bonds (i.e. lending) to a company or a sovereign (i.e. a government).

The pale red elements represent risks which are depressing the true value of your portfolio. For example, risks such as climate change, pandemic risks, or the risks from unaligned AI. Although I’ve presented this as though those externalities are negative, the principles work just as well the other way round (i.e. for companies or entities with positive externalities that increase value)

In the left-hand side, we see certain companies which have particularly large externalities. These could be particularly significant negative externalities from, say, fossil fuel companies, animal agriculture companies, or those who are developing (potentially misaligned) artificial intelligence. The concept also applies to particularly significant positive externalities (e.g. green tech companies, cellular agriculture companies, companies developing AI alignment approaches)

As an investor, if we influence the high-externality companies to make their externalities better, we can model the extent to which this improves the profitability of the rest of the portfolio – i.e. the investor can regain the red chunks in the diagram.

Using this, we can back-calculate a loss appetite: the amount we’re willing to lose on the high-externality investments (i.e. those on the left) is less than or equal to the amount gained on the rest of the portfolio (i.e. the sum of the red bits).

This loss appetite is at the heart of why this concept is so powerful.

If the investor is trying to maximise the company’s profit, and the company’s management is trying to maximise the company’s profit, then the investor is likely to have no impact.

The investor can have impact if they are willing to achieve below-market returns (i.e. have a loss appetite) on that asset. And because the asset generates externalities which hit the rest of the portfolio, tactically incurring below-market returns on that asset may lead to externalities across the rest of the portfolio which lead to greater returns on a portfolio-wide basis.

A note on terminology: I developed this concept independently and only later discovered that the concept had already been discovered by others and had been given the name Universal Ownership. I have now had several conversations with people who have a niche interest in this concept. As far as I’m aware the concept as outlined here agrees with the consensus view on what Universal Ownership is, but haven't checked that everyone would agree with each detail in this description.

Those highly familiar with the world of finance may prefer to skip this section.

The financial system aggregates money from individual investors and invests that money.

Individual asset owners mean “normal people” who have savings. For example, they might be people who work for an employer and have a company pension scheme.

Institutional asset owners include pension schemes and insurance companies. For historical reasons, life insurers offer savings products, including savings where there is some sort of tax benefit. This includes pensions. These organisations do a lot of work around administering the pension scheme/insurance product/whatever they are offering.

Asset managers may mean a company like BlackRock, Vanguard, State Street or Fidelity. Some insurers have in-house asset management companies. These companies do the work of managing the assets. This includes offering a fund that an individual or an institutional asset owner can invest in. It also includes deciding whether that fund should be underweight or overweight in a given asset (i.e. should be more or less willing to hold that asset). An employee of the asset manager will likely be in direct contact with the CEO/CFO of all the major companies they are invested in, and the asset manager is well positioned to perform engagement/stewardship to influence companies/entities in the real economy.

Firms/issuers refer to entities issuing financial products. Most obviously, this refers to any major company, or even mid-cap companies. Examples include Alphabet, Meta, Microsoft, Amazon, Yum Brands (which owns KFC, Taco Bell, etc), Exxon, Shell. Although providers of finance have traditionally focused their influence on companies, it’s worth bearing in mind that investors invest in government (aka sovereign) and local government debt as well.

Needless to say, the above is a simplification.

I have focused here on the “buy side” of the financial world, which I believe is most important for this write-up. I am not focusing on the “sell side” which is where financial instruments/securities are born; this is largely the world of investment banking.

The examples below follow the formula set out in this box:

Step 1: select an action that you want a company/entity to take/not take

Step 2: model the impact and the externalities

step 2a: model the asset-specific losses due to the loss appetite;

step 2b: model the positive externalities and their impact on the whole portfolio

Step 2c: apply intergenerational equity adjustment (this concept is described later)

Step 3: if the externality benefits outweigh the asset-specific losses, the asset owner is now empowered to take strong action to achieve that real world impact

The examples are included partly because making the ideas concrete makes it easier to understand what this concept is all about.

4.1 Example 1: Climate change

The concepts can be applied to any sufficiently high impact cause areas, but climate is a good example because climate is getting a lot of attention in the world of finance at the moment.

Step 1: select an action:

e.g. stopping companies from developing new fossil fuel facilities or exploration

Step 2: model the impact and the externalities

Step 2a: model the fossil fuel sector and understand how much lower profitability would be if the fossil fuel sector stopped new fossil fuel facilities.

Step 2b: model the externalities, specifically the extent to which the creation of new fossil fuel facilities or exploration would lower investment returns across the rest of the portfolio.

Step 2c: adjust for intergenerational inequity (this concept is described in section 9.1)

If the benefits across the rest of the portfolio (Step 2b), adjusted for intergenerational inequity (Step 2c; for an explanation of what this is about, see section 9.1) are greater than the losses incurred (Step 2a) then the action is warranted.

Step 3:

If the benefits outweigh the costs, the asset owner is now empowered to take strong action to achieve that real world impact, even if achieving positive impact for the world means reduced or even negative returns on the specific asset

Status: I have a draft model which suggests that benefits likely would outweigh the costs. At time of writing this model includes several inputs which are highly uncertain. In particular, a lot more work is needed on the social cost of carbon.

Here is a very high level summary of what’s in the spreadsheet model:

Step

Description

Comment

1

Select an action for investors to take: Use forceful engagement techniques to stop the building of new thermal coal plants

The specific action involves owning the coal companies and getting them to implement a policy of no new plants.

The model assumes this leads to 100 coal plants not being built. This is just one of many possible actions. Others include setting an appetite to avoid debt investment in coal, or influencing banks to not provide lending for new coal/fossil fuel facilities.

2a

Loss incurred by taking this action: This might reduce returns on the fossil fuel sector by c3.7% (e.g. the rate of return on the fossil fuel sector goes from 8% to 4.3%). This may translate to a reduction in returns of 0.09% across the portfolio.

Several elements of this are calculated in a conservative way; in particular it ignores the fact that shutting down X Watts of coal power production should lead to another X Watts of (nuclear? gas?) power production, which should generate returns which may also feed through to the portfolio. Some elements need substantially more effort to justify them robustly, however the calculation approach does include areas of conservativism.

2b

Benefits to the portfolio from this action: The reduction in greenhouse gas emissions leads to an extra c$10trn (or $0.1trn per plant).

An important assumption is the social cost of carbon. The estimates I’ve seen for this range from -$13/tCO2 (i.e. climate change is good; source is a 2019 meta-study) through to $3000 (source: UCL). The choice of a relatively high figure ($2,387) reflects the impression that I’ve garnered from conversations with climate academics and my reviews of climate models, suggesting that models do not explicitly capture tail risks. My view on this is very tentative; further research is needed on this.

The calculation assumes that the overall energy demand is not changed, and so the power still needs to be generated by someone; the model assumes that this comes from a nuclear plant; this is possibly a favourable assumption, but to account for this the action could be adapted to specify that the use of nuclear is actively encouraged (possibly incurring further costs to do so).

2c

Intergenerational inequity

For brevity, this is not discussed in more detail here. The concept is described in section 9.1. For more detail on how this is implemented, see rows 127-135 of the model. This element of the model may evolve in light of further research on this topic.

3

Conclusion: The benefits outweigh the downsides

The model considers the global $10trn benefits, and ignores all the benefits accruing outside the portfolio. Despite ignoring so much of the benefit of this action, the benefits still outweigh the costs incurred.

Note: one of the reasons for wanting to keep fossil fuels in the ground is that in case of future civilisational collapse, it will be easier to reindustrialise if there are still fossil fuels left. I don't think there's any way to explicitly incorporate this consideration into this sort of model, since it refers to events after a likely collapse of the financial system. So this reindustrialisation benefit would likely be a positive side effect.

Review of possible actions that investors could push for: the model above is based on stopping new coal plants (or new fossil fuel infrastructure); the aim is to identify a list of other actions which are impactful enough that they will go above and beyond what might happen naturally, but not so costly that they cost more than the benefits accrued under the UO model.

An important part of this is the social cost of carbon: the research will need to set out how climate academics have tended to model this; the next stage will be to build out the damage function more explicitly, by setting out a number of explicit mechanisms for how climate change might lead to catastrophic outcomes or damages.

4.2 Example 2: Unaligned artificial general intelligence

Unlike climate change, the concepts relating to unaligned AGI are still novel to most people in finance. Assuming that further research concludes that tackling unaligned AGI is a helpful thing for the financial system to do, a good time to introduce novel ideas might be now, while the whole area of ESG is still new and being developed. (Note, it might also be a bad idea in the context of AGI – the reasons for this are explored later in this post)

Step 1: select an action:

e.g. getting major AI firms (Facebook/Meta, Google/Alphabet, Amazon, Microsoft etc) to do substantially more to ensure AI is developed safely; this could include redirecting existing AI engineers to focus more on AI alignment work

Step 2: model the impact and the externalities

Step 2a: model the costs incurred by the firm in doing this. This may include direct costs -- e.g. hiring extra staff to work on alignment. It could also include the costs of redirecting some of their current staff to focus more on alignment and safety and less on developing new innovations/products. In principle also any indirect costs should be included, e.g. if an AI safety mindset causes them to develop AI in a slightly different (safer) way which means that they lose out on some short term profit.

Step 2b: invest in understanding the extent to which unaligned AI could cause harm. This includes modelling AI timelines (how long until we develop smarter-than-human artificial general intelligence) and how likely is it that the AGI is unaligned/orthogonal, and to what extent would a portfolio’s assets lose value in that scenario.

Step 2c: adjust for intergenerational inequity (this concept is described later)

If the benefits across the rest of the portfolio (Step 2b), adjusted for intergenerational inequity (Step 2c) are greater than the losses incurred (Step 2a) then the action is warranted.

Step 3:

If the benefits outweigh the costs, the asset owner is now empowered to take strong action to achieve that real world impact, even if achieving positive impact for the world means reduced or even negative returns on the specific asset

Status: I haven’t done any formal modelling to confirm that the benefits across the whole portfolio outweigh the costs. Here is an off-the-cuff model:

Not at all rigorous, quick and dirty AI/Universal ownership model

(A)

Probability that AGI is developed in the coming decades

20%

(B)

Given that AGI is developed, probability that it is not aligned (assuming no extra push in alignment work)

50%

(C)

Probability that asset owners lose all the value in their assets, given that there is an unaligned AGI

50%

(D)

Portfolio-wide loss appetite (= (A)*(B)*(C))

5%

(E)

Proportion of portfolio invested in companies doing AI work

20%

(F)

Loss appetite on companies doing AI work (= (D)/(E))

25%

The assumptions were entered without careful checking, and should not be treated as a definitive model. It suggests that investors should be willing to reduce returns by up to 25 percentage points, as long as that investment genuinely led to a reduction in the probability of unaligned AGI. As with the rest of this paper, it also incorporates the crazily conservative assumption that in that scenario, the only thing the investor will care about is the fact that they will lose out financially.

To get a sense of how substantial this could be, it seems likely that the total spend on AI alignment is unlikely to be averaging at a rate much higher than $100m per year, if not less.

By contrast, Big tech firms spend much more than this on AI talent. For example, Deepmind spent around $1bn in 2020, and Alphabet, Meta, and other big tech firms collectively have substantial pools of talent and funding which could be partially redirected toward AI safety. Doing so could unleash substantial pools of talent and funding for AI alignment; pools which are currently focused on pushing AI forward.

Note that there are reasons to doubt whether this action will be effective (as mentioned later in this paper). These doubts can be incorporated into the model; indeed the structure incentivises this, and this is one of the strengths of the Universal Ownership system as outlined here.

This increases the extent to which the AI alignment work happens in the heart of the large firms which are creating and deploying AI. This increases the probability that the alignment approaches, once created, actually get used.

4.2.1 Further research needed with regard to AI risk

Further research is needed to explore whether this will actually be effective at tackling AI risk.

Part of the benefit of this is to raise awareness of the risks of unaligned AI among the finance community. Doing so could lead financiers to take the risks of unaligned AI more seriously; this could lead to a number of positive consequences. However it could also lead financiers/investors to realise how much more powerful future AI could be relative to current AI, which could lead investors to influence companies to push for AGI sooner. Further research is needed to explore:

Is it possible to influence norms around how unaligned AGI is perceived? It appears that divestment campaigns have been successful in detracting from the fossil fuel companies’ social licence to operate, so a similar campaign could be effective at changing perceptions of unaligned AGI among investors. To be clear, this would not be sufficient to stop all investment in the development of AGI. However it may cause trepidation on the parts of some investors. The area to explore is a judgement about whether this effect outweighs the risks that some investors may become more interested in investing in AGI. This exploration should also consider how the “ESG” concept is perceived; i.e. including this risk within the ESG banner may invoke moralistic sentiments.

The culture of different segments of investor: life insurers are material asset owners but also need to explicitly model risks (at least this is true in many jurisdictions such as those with Solvency II or equivalent frameworks); it may be the case that the culture of risk awareness leads insurers to be a good choice of asset owner

Goodharting risk: if the models justify strong action based on the long-term risks of AI, is there a risk that by the time the concept is “Chinese whispered” from the world of finance to the people in the AI companies, could the understanding of the risks have morphed? For example, could the models justify more work on long term AI safety, but lead to more work on short term AI safety (where the latter refers to risks such as biased algorithms).

Further research should also explore the extent to which the work done to tackle short term AI safety is useful groundwork for AGI alignment work. (i.e. could the aforementioned failure mode be a graceful failure)

Assume that the ideas were transmitted faithfully and goodharting risk were overcome (i.e. if there was a surge in appetite for long term AI safety work in the big tech companies). Would this lead to a surge in effective work on long term AI safety? To what extent do the outstanding problems in AI safety require the skillset of the AI engineers or other staff working at big tech firms? Is there a risk that the “AI engineer” mindset is materially different from the AI safety mindset, and that this might make it harder to effectively redeploy existing AI talent? As it would likely take some years before the ideas filter through the financial system and reach the key asset managers, it would be important to explore what this will look like in a few years time as well.

4.3 Example 3: Industrial/”factory” farming

Although the world of ESG finance is still heavily focused on climate risks, there is some slowly growing attention on the idea that some elements of natural capital are important.

Step 1: select an action:

e.g. getting major animal farming companies to stop all industrial/”factory” farming

Step 2: model the impact and the externalities

Step 2a: model the costs incurred by the firm in doing this; presumably the firm may be able to shift to a different type of farming, e.g. animal farming which is substantially less industrial (and substantially less profitable) or farming of plants. This change would likely cause the company to incur some short term transition costs, especially if the company currently has experience and capabilities in industrial animal farming. In addition, the new business model may be structurally less profitable.

Step 2b: model the extent to which industrial farming causes harm. Unfortunately a limitation of this modelling (at least at the moment) is that it focuses just on profitability, which means that animal suffering is not captured in the model (although that could evolve over time, see below). However, animal farming poses risks to humans as well -- it’s implicated in climate change and pandemic risk. Hence the model would quantify outcomes like:

less industrial animal farming → more forests intact → improvements in atmospheric greenhouse gas concentrations → improved economic/profit outcomes as assessed using (e.g.) the social cost of carbon

less industrial animal farming → more forests intact → less zoonotic disease transmission → fewer pandemics → fewer economic stresses/downside risks to profitability

less industrial animal farming → less anti-microbial resistance → fewer pandemics → fewer economic stresses/downside risks to profitability

Step 2c: adjust for intergenerational inequity (this concept is described later)

If the benefits across the rest of the portfolio (Step 2b), adjusted for intergenerational inequity (Step 2c) are greater than the losses incurred (Step 2a) then the action is warranted.

Step 3:

If the benefits outweigh the costs, the asset owner is now empowered to take strong action to achieve that real world impact, even if achieving positive impact for the world means reduced or even negative returns on the specific asset

Status: I haven’t done any modelling on this, and don’t know whether the benefits would outweigh the costs.

4.3.1 Further research needed with regard to pandemic risk

Background on natural and engineered pandemics

High-level research to support a UO model

estimates of rate of emergence of natural pandemics, estimates of rate of emergence of engineered pandemics, including deliberate and accidental, exploration of how future pandemics could affect asset prices.

Research on impact routes:

Lab safety: what proportion of BSL4 labs are privately owned, if privately owned labs were influenced to have a stronger safety culture, how likely would this culture be to spread to government-owned labs, what scope is there for financiers to influence governments on pandemic risks, be it in their capacity as investors in sovereign debt or in other ways.

Greater government funding of high-impact research

More government resilience in health systems

Research on the financial impact of pandemics

The impact of COVID-19 has been unclear. At first glance, the effect seems to have been that assets lost a lot of value in the short term, but then quickly regained that value, and some assets, especially tech stocks, ended up doing better.

As I outlined in my talk on pandemic risk for a conference of the Institute and Faculty of Actuaries, there are three interpretations of this:

COVID was good for the S&P 500, and the early decline was market irrationality

COVID is bad for asset values, but government stimulus packages are maintaining asset values (and storing up problems for a later date), and the initial market decline was because investors didn’t know the stimulus package was coming

COVID had the potential to be catastrophic, but fortunately it wasn’t; the initial decline was a rational response to the potential of an outcome that could have been much worse

One part of the research is to explore this last possibility. Specifically the research should explore:

Could future pandemics have systemic effects, for example could critical infrastructure fail to function if there is a high-enough death rate? If so, what would that mean for asset values?

The focus should not be so much on the specifics of COVID (although some reference to COVID is inevitable); instead it should consider the potential ramifications of future pandemics

5. Real impact is possible

The examples in section 4 have ended tantalisingly with references to “strong action to achieve real world impact”.

In order for the Universal Ownership concept outlined here to work, it must be possible for asset owners and providers of finance to achieve real world impact.

At first glance this seems intuitive -- after all, providers of finance actually own the real economy.

However it’s reasonable to question the track record: has much real impact been achieved by mainstream finance? For example, the world of finance has increasingly turned its attention to climate risk, and nonetheless carbon dioxide emissions continue to rise despite the pandemic, global meat consumption looks set to keep going up in 2021, and investment in new coalfacilitiescontinues.

This write-up is too short for a full review of impact investing.

However here are some relevant intuition pumps, which suggest that real impact is possible, even if it hasn’t happened enough yet:

Engine No 1 is a distinctive activist hedge fund; it bought 0.02% of the shares of Exxon, spent only $12m, and was able to introduce several new, more climate-aware board members to the Exxon board.

Divestment of publicly traded equities (i.e. shares) will have minimal effect (because when you sell them, the shares simply move from one owner to another without affecting the capital flowing into the company). However this story is different for debt (i.e. when companies borrow money). Debt has a maturity date (unless it’s perpetual, but that’s very rare). When the debt matures (i.e. when it is repaid), the fact that an investor is not willing to invest in it means that the company would find it harder to borrow more. This means it could lose out on actual capital – or at least have to pay more/accept less good terms to get that capital. Andreas Hoepner, the academic associated with the phrase “deny the debt, engage the equity” has observed that divestment in South Africa appeared to have minimal effect on equities, but was effective because of the impact on debt.

“Vote no” strategies involve voting against the reappointment of a director of a company. There is precedent for their use, but they are not in widespread use in mainstream finance. This action has the potential to have real personal consequences for the directors and decision-makers of the companies. An asset owner can start by simply asking for change. Being able to escalate to a “vote no” action is powerful: it seems highly likely that the threat of losing your job would be a strong incentive to comply -- much stronger than the risk that a current investor might divest. At first glance it would seem that 50% of shareholders would need to demand the same action before this is effective -- in other words this appears to only work after systemic change in the financial system has occurred. It’s somewhat easier than this because institutional asset owners are much more likely to vote than individual shareholders. Furthermore, anecdotal evidence suggests that even a modest level of “voting no” is surprisingly effective: directors are accustomed to close to 100% of votes being for their reappointment, and even only 1% of votes being against them is a source of embarrassment.

There is more discussion of this in section 10.3.

5.1 Further research needed on impact investing

“Exit vs voice”: i.e. under which circumstances does it make sense to divest/not invest, and when does it make sense to invest (e.g. in order to influence the company’s decisions):

I have alluded above to the possibility that divesting from shares traded on the secondary market appears to have minimal impact: research is needed to explore the counter to this. To what extent does divestment lead to an increase in the cost of capital; is there evidence that it makes it harder for companies to raise new capital

Review of the effectiveness of the “vote no” strategy; what past evidence is there of this working; what is the quality of the evidence

Exploration of impact as a debt investor: what evidence is there to support the claim that avoiding investment in “bad” debt will avoid negative externalities from occurring? Under what circumstances will investing in “good” debt lead to positive externalities occurring which wouldn’t have otherwise?

Primary market investment in “good” activities: what are the barriers to getting these ideas to spread to the VC market; when the VC firms seek to exit from their investment, they will likely sell the business to investors in mainstream finance. Is this incentive sufficient for them to encourage them to also model externalities and impacts? If not, how well positioned are asset owners in mainstream finance to provide primary investment in early-stage companies?

To what extent do investors currently work to achieve impact in their capacity as investors in government (i.e. sovereign) debt; how effective can investor influence be, given that governments are beholden to multiple stakeholders; are there any a priori reasons why this may be inadvisable; who are the key stakeholders (i.e. to what extent are credit ratings agencies influential compared to, say, asset managers); this review is likely to find that investors in sovereign debt have less impact than investors in companies – how much impact can the financial system have for big problems which have government and corporate involvement?

How much of the financial system needs to be thinking this way before impact is achieved? E.g. could it work with only 1% of the world’s assets adopting UO thinking? (after all, Engine No 1 achieved impact with much less than 1% stake in Exxon.) Does it need >90%? (which might be unrealistic?) Could it work with c20%? (e.g. because that’s a big enough constituency of the ownership to dissuade management from doing bad things, especially when small, non-institutional investors don’t vote). How does this question interrelate with the different asset classes?

Displacement effects: If an investor forces a company to stop doing bad-but-profitable activity X, will another company pop up to do X? What are the drivers of this displacement risk, how is this risk influenced by the components of the financial system (e.g. VC funding vs mainstream buy-side institutional investors vs hedge funds vs governments), to what extent can this risk be mitigated, and if so how, and how should it be incorporated into UO models?

6. How widespread does Universal Ownership have to be to achieve impact?

As the Engine No 1 example indicates, highly significant influence can come about even if only a handful of large asset managers adopt these models. This section explores to what extent this can be replicated at scale.

Shareholder influence (aka engagement or stewardship)

Lenders (aka debt investors) investing in “good” debt

6.1 Shareholder influence (aka engagement or stewardship)

It appears that shareholder influence may have a big impact even if only a handful of large firms adopt this approach:

The “Big Three” index fund providers (BlackRock, State Street and Vanguard) have constituted c.25% of all shares voted in corporate elections in the S&P 500. (source: Ceres)

Those three asset managers collectively managed $22trn as at around 30 Sept 2021 (source: ADV ratings). The ten largest asset managers collectively manage $45trn.

For comparison, the amount of assets signed up to the UN PRI is > $100trn

Hence if those ten institutions alone adopt Universal Ownership, then this is likely sufficient for >50% of votes to be following this approach. Influencing those ten institutions is a substantial but not insurmountable challenge.

Note that companies may well adapt long before 50% of shareholders are adopting Universal Ownership and pushing for positive impact

Note that the above calculations relate to the S&P 500. If an asset owner pushed a large company to change its behaviour, then would the ”bad” activity simply be adopted by another, smaller company?

Part of the strength of the UO system is that there are incentives to ensure that such risks are considered and incorporated into models. I.e. if you (an asset owner) believe that there’s a risk that your actions won’t have the desired impact (e.g. because a startup will do the activity if the large company doesn’t) then it makes sense for you to incorporate that risk into your models.

6.1.1 Further research needed on displacement effects with shareholder impact

Does the activity have barriers to entry? (e.g. not many people would be able to undertake a complex operation such as building a fossil fuel plant)

Which asset owners are more or less prone to fund activities with high negative externalities in order to gain profit?

What are the international dimensions to this?

6.2 Lenders (aka debt investors) investing in “good” debt

“Good” debt here refers to debt to fund activities which have lots of positive externalities.

This does not need a large pool of asset owners. Once asset owners have funded the work, this is sufficient to achieve impact.

“Bad” debt here refers to debt to fund activities which have lots of negative externalities.

The key issue here is that even if (say) half of all debt investors believe that they should be put off from investing in “bad” debt, that still leaves lots of investors who are willing to invest. This is unlike the “good” debt scenario.

6.3.1 Further research needed on displacement effects with debt investment

The research should also consider other sources of borrowing. For example, the fossil fuel sector currently relies heavily on banks in order to borrow for new fossil fuel activities.

Further work is needed to clearly articulate the theory of change. E.g. people in the investment sector (who?) speak to governments → governments recognising pressure to behave differently → changes in policy.

We know that governments can be influenced by credit ratings agencies. To what extent is there an influence if a topic is on the agenda of credit analysts at asset managers? To what extent is it possible to push for specific changes, and to what extent are investors better positioned to put topics higher up on the agenda (without necessarily specifying precisely what should be done about them)

7. Misc other observations

An interesting implication is that Universal Ownership could be a badge of credibility around greenwashing (i.e. the accusation that financiers/companies are paying lip service to ESG ideals). This is because the Universal Ownership models make the incentives more strongly aligned: asset owners who proclaim loudly about the positive effects of their investment decisions would be punished financially if they had not done their due diligence to ensure that the positive effects were real. Or conversely it’s because if you take a local loss (on the immediate asset) in order to enjoy a global gain (on the whole portfolio) then this adds to credibility.

It’s useful to distinguish between two different things this project can achieve:

For climate risks: providing a clear, model-based rationale for achieving impact

For non-climate risks: raising awareness of the risk among a constituency which is strategically chosen for impact

While the asset owner's moral stance may well place value on things other than investment returns, the universal ownership model simply focuses on the portfolio returns alone. It is possible to expand the universal ownership model to place value on other outcomes apart from profit. Inherent in this is the determination of something called moral weights (e.g. how much profit am I willing to give up in order to save one statistical life?) An asset owner starting on its journey as a universal owner would be unlikely to incorporate these elements immediately because of the complexities of determining moral weights, and the extra modelling required.

In principle there's nothing to stop a Universal Ownership model incorporating assets with a guaranteed return of -100%. This essentially allows charitable donations to be incorporated within an asset portfolio, but only where the impacts have satisfied a number of demanding financial models, as required by the Universal Ownership framework. Doing this would require careful communication with stakeholders.

I believe the thoughts outlined in this article outline the best hope for the whole of mainstream finance to have genuine positive impact, this does not mean it is the best thing you can do as an investor to have the most impact you can. A high net worth individual could identify specific high impact investing opportunities. For example, assessments such as this review of Mind Ease might identify which investments are the best ways to invest to do good. (Note: I have not reviewed that write-up.) It may be a struggle to find enough investment opportunities which meet a high bar for impact, especially when accounting for the fact that high impact investment opportunities which are also highly profitable would likely be very well subscribed. For all the money which doesn’t meet this bar, adopting a universal ownership approach would likely enable the wider financial system to adopt this approach. Therefore I believe that the highest impact way to invest for someone who wants to maximise the amount of good they do with their investments

8. Impact of this work: across the probability distribution

This paints a picture of what might happen assuming that this concept gets material EA support.

8.1 95th percentile: realistic best possible outcome

This paints a picture of what the 95th percentile outcome might look like, assuming that we pursue this concept now. These outcomes will likely take several (maybe 15) years to achieve.

As set out below, this leads to a substantial change in the way that global resources are allocated.

The work outlined here leads to systemic changes to the way the financial system operates

Under the realistic best possible outcome, the sort of modelling outlined in this document has become mainstream across the financial system. I.e. >25% and maybe >50% of global financial assets employ these models. This is the portion of the financial system which is most influential on company management.

Because mainstream corporate finance overwhelmingly uses such models in the realistic best case scenario, corporates themselves are employing these models, and executive remuneration is based not just on profit generated, but rather incorporates careful, EA-style models of externalities (e.g. what is the ultimate harm caused by the climate implications of these greenhouse gas emissions? What are the global implications of unsafe AI?). They use these models to guide their actions.

This leads to systemically different corporate behaviour. Fossil fuel companies now largely self-regulate. Major AI companies actively work to ensure safe AI. Agri-businesses are incentivised to at least avoid the harms that industrial farming can cause to humans.

This mode of thinking has also extended to government-owned companies (e.g. government-owned fossil fuel companies) because asset owners also have influence over governments (e.g. in their capacity as providers of finance for government debt, or because they are important employers of citizens).

This means there are very few companies left who can “defect” – i.e. who are in a position to take profit at others’ expense. The only ones who can do this are those who are willing to have a very concentrated portfolio, which is counter to the standard advice that “diversification is the only free lunch”. This is likely to apply to a very small number of investors. The only companies likely to be able to take profits without considering externalities are businesses which are still (materially) founder-owned. 7% of large companies are owned by their founders.

The financial system is now set up to actively seek out opportunities to achieve improvements in corporate externalities.

The opportunities being sought need to have large, broad scale impacts in order to be material enough. This means that a mindset of actively seeking the most important impacts is built into the system.

I’m not sure this is still within the 95th percentile of outcomes within 15 years, however if we extend to longer than 15 years or to an outcome beyond the 95th percentile:

Furthermore, the models don’t simply assume that asset owners only want profit at the expense of all else. Instead, the models also reflect moral weights and trade-offs between profits (for me, the asset owner) and other good outcomes in the world. (Note that this might require some changes in or clarifications to the law in some jurisdictions, but that work to campaign on this has already started; see, e.g. the work of ShareAction)

This means that the corporate world places explicit value on human life, animal welfare, and other things we value other than profit.

The next section (section 9) sets out some question marks around timing mismatches. I believe that this is a thorny issue, and it’s unclear to me whether it’s fully resolved in the 95th percentile scenario, or whether it is complex enough that it is more likely even than this; it likely also needs substantial support from NGOs.

The project achieves nothing (See the “achieves nothing” failure modes outlined in sections 10.1 and 10.2)

There are no negative effects apart from the opportunity costs of the funding

8.4 5th percentile: realistic worst possible outcome

See section 10.4 (getting the financial sector to make decisions could be unfavourable)

9. Possible issue: Timing mismatch

This section and the next is about discussing some potential objections/counters/failure modes of this concept.

I believe the biggest concern is the timing mismatch issue. This issue is:

Investors have to incur a loss now…

… but the benefits across the rest of the portfolio probably only occur later

This casts doubt over whether investors would really want to incur that loss, and without the loss appetite, the basis for genuine impact evaporates.

I’m going to explore two angles on this

9.1 intergenerational inequity concerns, which may be a legitimate concern, and which I think is relatively easily managed, and might be a feature, not a bug

9.2 incentive issues, which I believe to be more important, and for which have set out three solutions

If this issue is solved effectively enough, it has exciting systemic implications. The final sub-section explores these:

9.3. Seekers, not just planners: A framework for an action-oriented ideas marketplace

9.1 Intergenerational inequity concerns

Imagine an institutional asset owner, such as a pension scheme. This asset owner amalgamates together funds from different (heterogeneous) individual savers. These include:

Alice, a 27 year old member of the pension scheme

Bob, a 63 year old member of the pension scheme

If the asset strategy involves taking a loss now in order to make better profits over the coming decades, then both Alice and Bob will incur the losses, but Alice will reap the financial rewards while Bob doesn’t.

This (arguably) constitutes intergenerational inequity. (I use the term “arguably” here, because some might argue that this action actually just corrects a pre-existing intergenerational inequity – this argument is explored in section 9.1.4).

The above example comes from a pension scheme, but the concept would work similarly for other financial institutions such as certain types of life insurance product.

At this point, our hearts might observe that the positive actions don’t just have profitability implications, but also wider benefits for the wider world, and that Bob probably has children or grandchildren or even just younger friends who might benefit, or even Bob himself might benefit from the non-financial benefits of these actions.

However our models are built giving no credit to non-financial benefits – at least at first.

I believe there are three possible resolutions to the intergenerational inequity issue:

9.1.1 Simply incorporate tail risks now, and don’t give credit to gains several years/decades from now

9.1.2 If prices incorporate future risks, this would resolve the problem

9.1.3 Incorporate an explicit appetite for intergenerational inequity

9.1.4 Reframe the issue as an antidote to an existing intergenerational equity problem

9.1.1 Simply incorporate tail risks now in UO models

The intergenerational inequity concern often arises when thinking about climate risk.

My description of the concern incorporates a widespread assumption:

Climate risks will be really bad – the reason why it doesn’t feel catastrophic now is that the worst is yet to come

I’m confident that climate risks will get worse if we don’t tackle them. However it’s also possible for another hypothesis to be true:

Climate risks already mean that the probability of catastrophes is elevated now

Given that the insurance sector is already experiencing elevated and upward trending losses from extreme weather, this seems to be the case.

The modelling that I’ve done thus far has not yet been detailed enough to distinguish between a social cost of carbon which incorporates the tail risks which exist now and a social cost of carbon which incorporates the extent to which climate hazards will get worse over time. Hence I don’t know whether the risks are bad enough to warrant strong actions under a Universal Ownership model. Furthermore, the incentive issues described in sub-section 9.2 may still apply here (i.e. just as it’s problematic to get assets to reflect risks which don’t arise until some time decades from now, it may also be hard to get assets to reflect risks which have a small probability of arising in the short- to medium-term).

Similar thinking could be applied to other risks apart from climate risk.

If this approach is not sufficient to resolve the issue, incorporating an explicit appetite for intergenerational inequity should be sufficient.

Further research needed: this is already captured earlier in this document, but more research is needed on the Social Cost of Carbon.

9.1.2 If prices incorporate future risks, this would resolve the problem

If asset prices fully reflected future systemic/tail risks, there would be no intergenerational inequity concerns, because the systemic benefits would be recognised immediately.

This is explored in section 9.2.1.

9.1.3 Incorporate an explicit appetite

While it’s certainly unfortunate that Alice gains while Bob loses, it’s not necessarily correct to infer that the UO-sanctioned actions should not be taken.

Looking at gains and expenses in purely financial terms:

If we take the actions, Alice gains at Bob’s expense.

If we don’t take the actions, Bob gains at Alice’s expense.

As there is no easy way out, the current draft of the model includes an explicit appetite for intergenerational inequity. This applies an adjustment in the model. For example, an appetite of 50% would mean that the UO model has to find twice as much benefit as the short term loss in order to justify taking an action.

This appetite could be set at the level of each asset owner (e.g. the specific pension scheme), and could reflect the age profile of the scheme or other considerations.

9.1.4 Reframe the issue as an antidote to an existing intergenerational equity problem

At the moment asset owners have stakes in industries which achieve economic growth now at the expense of younger members. I.e. the status quo benefits Bob at the expense of Alice. Arguably, therefore, the impact work that the UO models would recommend may not be benefitting Alice at Bob’s expense, but rather undoing the injustice being done for Bob’s benefit at Alice’s expense.

Further research is needed to explore intergenerational equity in more detail. This would involve a review of the existing thinking on intergenerational equity in the context of climate change and environmental law, and some work to determine how this relates to Universal Ownership.

9.2 Timing mismatch incentive issues

I believe this is a bigger issue than intergenerational inequity.

The concern here is that even if asset owners would technically be serving their clients better by employing the ideas set out here, they might opt not to do so because the benefits arise potentially some years in the future. Hence asset owner institutions may not be motivated to act now for benefits which may not arise for several years.

I can see two potential solutions:

9.2.1 Prices may incorporate tail risks within a small number of years

9.2.2 Universal ownership could be a solution to mis-selling risk

9.2.1 Prices may incorporate tail risks within a small number of years

The finance sector is currently experiencing a boom in interest in ESG, and some would say that the main aim of this is to

firstly improve disclosures; and then

use the improved disclosures to ensure that risks are adequately captured in the prices of assets.

It is certainly conceivable that this project will be successful in the coming years – at least with regard to climate change, which is getting the most attention at the moment. If this is the case, then assets will already directly reflect risks. This means that a substantial improvement in risks would lead to benefits being reflected immediately in the price. This would solve the problem.

On balance, I don’t feel great optimism that this will happen naturally. At least, if we’re talking about capturing the risks to a very high quality within, say, the next three years, then I’m quite confident this won’t happen.

When individual assets are priced, a “stock-picking” mindset is usually employed. I.e. the model to set asset price usually is very careful to model asset-specific features. E.g. if my model can tell me that stock A is better than stock B, then I can invest less in stock B and more in stock A. However if there are systemic tail risks, and for all I know they will affect stocks A and B equally, then traditionally there is no point modelling these risks too carefully. Instead I simply discount future cash flows, and this implicitly captures those risks.

Because the financial system is working within this paradigm, it is very interested in the question of which assets are more or less exposed to risks relating to climate change, but less attention is going on the question: “to what extent does climate change make my assets less valuable”. Hence a number of generic risks can be captured in the discount rate.

However there may be scope for this “systemic” or “beta” perspective to become more explicitly incorporated in the way that the financial system models things, if there is a strong push for this to happen – which would require a substantial amount of extra work.

9.2.2 Universal ownership could be a solution to mis-selling risk

Currently asset owners such as life insurers and asset managers advertise their ESG funds using feel-good imagery. However these funds frequently do not aim to achieve impact. Instead they have a “risk management” aim, meaning that they aim to identify climate (or other ESG) risks, and reduce exposure to the assets which would be most exposed to those risks; i.e. this is a goal entirely consistent with the aim of maximising returns for investors.

I have conducted initial surveys, in which I showed respondents screenshots of websites selling ESG funds. Those surveys have found that:

If respondents invested in an ESG fund, they would expect the fund managers to be using their money to make the world a better place

If an ESG fund only protected their funds from ESG risks without expressly doing anything to make the world a better place, they would be disappointed.

They would expect their fund manager to be protecting their funds from ESG risks (and other risks) anyway -- whether or not it's branded as an "ESG" fund.

Note that these surveys have been conducted using low sample sizes and low-cost research methods, which means that the survey would need to be replicated before its findings were considered robust. Having said that, other research seems to be pointing in the same direction. If we assume this reflects reality, this would constitute a legitimate reason for financial institutions to be concerned.

Arguably, by promising a product which promises to make the world better but doesn’t do so, or even really try to do so, then this falls foul of “mis-selling”. People in financial services are typically wary of the risk of mis-selling scandals, as such issues have been very costly for the industry in the past.