Comments

Thank you for writing this and for the honest self evaluation.

Thank you for writing this and for the honest self evaluation.

For Hassana in Kogi, Nigeria, October’s floods were not like years past. “All our farmlands washed away as many had not yet harvested what they planted. The flooding continued until our homes and other things were destroyed. At this point we were running helter-skelter,” she said.

These floods, the worst in a decade, result from predictable seasonal rains. If we can anticipate floods, we can also anticipate the action needed to help. So why does aid often take months (even up to a year) to reach people like Hassana? Traditional humanitarian processes can be slow and cumbersome, government and aid agencies often lack the capacity and money to respond, and most aid is delivered in person, an added challenge when infrastructure is damaged.

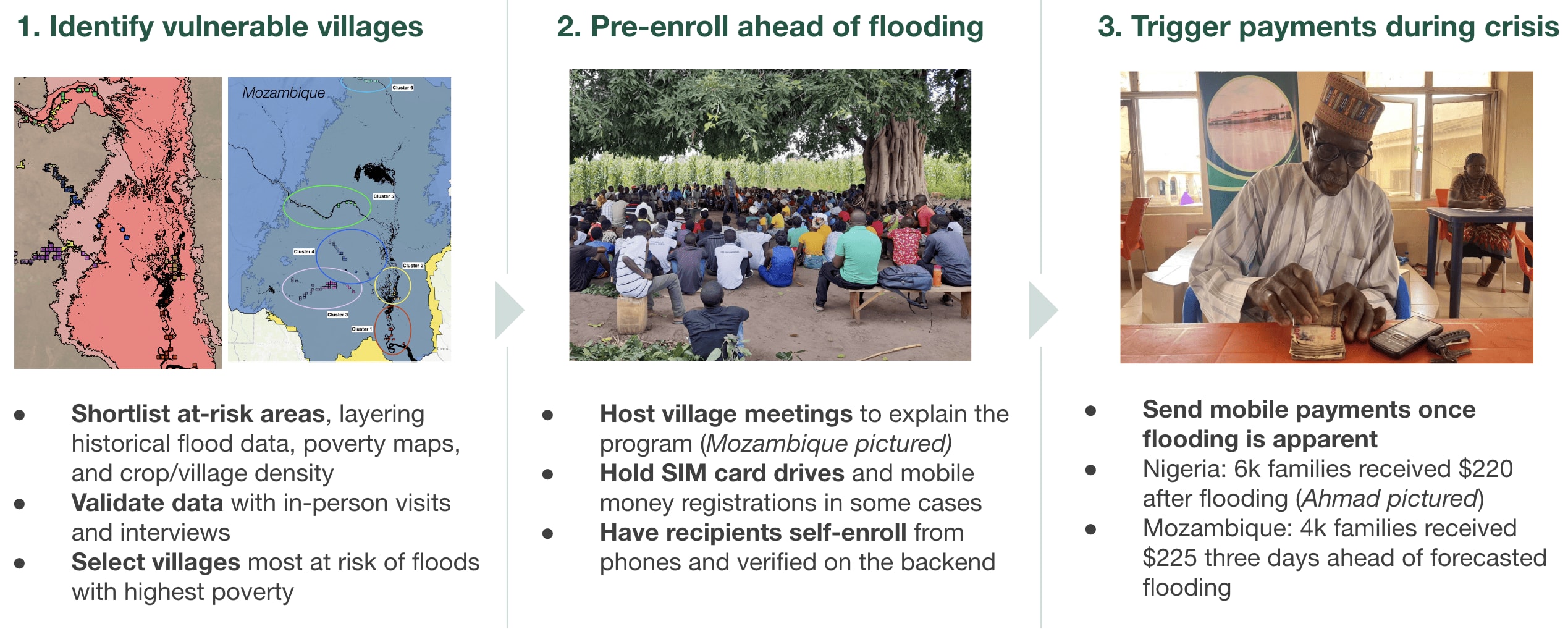

Digital cash transfers can avoid these issues, and getting them to work in a disaster setting means more people will survive climate change. In the past year, with support from Google.org, GiveDirectly ran pilots to send cash remotely to flood survivors: in Nigeria, we sent funds to survivors weeks after flooding and in Mozambique, we sent funds days before predicted floods. Below, we outline what worked, what didn’t, and how you can help for next time.

Over 1.5B people in low and middle income countries are threatened by extreme floods. Evidence shows giving them unconditional cash during a crisis lets them meet their immediate needs and rebuild their lives. However, operating in countries with limited infrastructure during severe weather events is complicated, so we ran two pilots to test and learn (see Appendix):

Innovating in the face of climate change requires a ‘no regrets’ strategy, accepting a degree of uncertainty in order to act early to prevent suffering. In that spirit, we’re laying out what worked and did not:

✅ Designing with community input meant our program worked better

A cash program only works if recipients can easily access the money. In Nigeria, we customized our program design based on dozens of community member interviews:

❌ We didn’t send payments before severe floods

In Mozambique, we attempted to pay people days ahead of severe floods based on data from Google Research’s Flood Forecasting Initiative, using a model validated on the only available data source: 50 years of government river level measurements. During Cyclone Freddy’s second landfall, our forecasts predicted river levels would rise to dangerous levels in the region, so we sent anticipatory $225 transfers to 4,183 people across 11 villages, aiming to help families prepare.

Ultimately, severe floods never came in the villages we paid, though some un-enrolled villages in nearby areas were flooded as Cyclone Freddy was the most significant of the season. Though we couldn’t respond in villages hit the hardest, we still paid people who are consistently vulnerable to climate disasters: 90% of people who received this payment had survived a significant flood in the prior year.

In the future, we need more flexibility on where to respond and to incorporate more than one trigger from forecasts to make sure we respond at the right time and where floods are most severe. In addition to overflowing rivers, floods are also caused by rain (flash floods), which are hard to predict on a village level, and certain villages are more likely to flood than their neighbors due to subtle geographic differences. In post-pilot conversations, these communities also told us they’d need payments more than several days ahead of a flood event to fully utilize the cash and prepare.

As we scale up anticipatory action, we’ll continue working with Google Research, local communities, and experts to:

❌ Limited pre-enrollment meant we lacked flexibility to respond to the worst floods

When Cyclone Freddy approached Mozambique, we could tell it would likely hit hardest far north of where we’d pre-enrolled villages – but we couldn’t pivot and pay the villages that were clearly about to experience the worst floods. Though we had more luck in Nigeria predicting where floods would hit, we accepted some uncertainty with our village selection. This lack of flexibility was a major limitation, but our budget limited us to only pre-enrolling a relatively small area.

A larger potential payment area means a more responsive program. There are two ways we can improve, each with its own trade-off:

✅ Ultimately, people in poverty affected by floods got money

One reason for our ‘no regrets’ principle is that any money put in the hands of people in extreme poverty is a good thing. Nearly all of the families in Mozambique paid ahead of March’s forecasted river floods that never came had suffered from other flooding in the prior year and used the funds to improve their resilience. Across both countries, we delivered $3M to 13,782 families impacted by both flooding and poverty, which they spent on things like agricultural inputs to restore damaged cropland, evacuation to safer areas, food and essential goods, and home repairs/improvements (see Appendix)

Our Google.org-funded pilots prove it’s possible to quickly send cash aid to flood survivors in extreme poverty. We already have actionable ways to improve our flexibility, accuracy, and speed next time. But in typical humanitarian grantmaking, funding is only released after a flood happens, which leaves little room to innovate. We need more donors committed to giving funds for climate survivors before the crisis hits. Support innovation before the next disaster.

As the New York Times observed, bringing our work to scale could change how billions of dollars in loss and damage climate funding is spent. What works for 10,000 people could soon reach millions.

If the flooding is predictable, are we causing moral hazard by subsidizing farming in flood-prone areas?

As long as only a small percentage of people in flood-prone areas receive payments (and which villages receive them isn't too predictable), I wouldn't expect any meaningful moral-hazard effect. I don't expect people would move into such an area for a tiny chance at receiving a payment of this size at some point in the future. And the people who were already there before GiveDirectly started the program weren't motivated by the pilot program.

I agree with Jason that the specific moral hazard of "people might move to flood-prone areas in order to get cash" seems unlikely to be a concern.

The moral hazard that I was thinking of when I read Robi Rahman's comment was "people who already live in flood-prone areas might be less prone to invest in flood defences/move away/do other things in light of the information that floods may be coming"

I think that's contingent on the percentage of people who receive payments, and the ability to predict one's likelihood of receipt. If GD gives money to the same people every flood season, then I would be much more concerned about this than if everyone in the flood zone knows they have a 5% chance of receiving money in any year their area was flooded.

If the question is whether the beneficiaries may be more likely to stay / underinvest / not take action once identified as conditional beneficiaries shortly before the flood -- it didn't sound like getting the payment was conditional on being in the flood zone when the flood actually hit. If you were pre-registered to location X earlier in the season, and location X was selected as a beneficiary site, it sounds like you got paid. If that's true, one could argue for the opposite effect -- evacuation can be pricey, last-minute flood defenses require resources, etc. So getting them money a few days ahead of the storm might enable better risk-mitigation measures. I'm thinking of the people in the US who didn't leave before Hurricane Katrina due to lack of funds.

This isn't something I expect either, and I think you may be slightly misunderstanding the mechanism by which moral hazard leads to bad outcomes.

When moral hazard hurts regular people who have their money in the banking system, it's not because a bank executive specifically tried to bankrupt their corporation to collect bailout funds from the government. Rather, it is the toxic incentive structure caused by privatized payoffs and socialized losses. These executives can gamble money on risky business practices knowing that they'll keep the profits and be rewarded if they succeed, but the government will pick up the mess if they backfire.

Right now the state flood insurance systems of California and Florida are insolvent, because these states have been paying out claims at an increasing rate while the homeowners' lobbies have blocked a corresponding increase in insurance prices. Private insurers are losing money and considering ending their business in these states altogether, and then the state insurance funds will be unable to pay out all its obligations in the next inevitable (and entirely foreseen) 100-year flood. The federal government has been exacerbating this problem by 30 years by subsidizing flood insurance costs, which encourages people to keep living in flood-prone areas they otherwise would rightly avoid.

But, payments from GiveDirectly are on a far smaller scale, and may not have an analogous effect.

I don't think we disagree much if any -- my next point was that the people in these areas had decided to live there prior to and independently of GiveDirectly's action. To the extent they were engaging in a cost-benefit analysis, the current residents had already decided it was worth the flooding risk.

At least in Florida, my understanding is that many of the more at-risk properties would not have been built at all (or at least re-built) but for the government subsidized insurance covering the bulk of losses with very high probability. Between the size of the GD payments, and the small fraction of flooded people who receive them, an analogous effect here seems unlikely to me.