Comments

How much of this advice is generally applicable outside the US?

How much of this advice is generally applicable outside the US?

Thanks for asking, and I want to caveat again that this is not intended as financial advice.

Unfortunately I think relatively little of this material would be relevant outside the US. The section on finding fee-for-service financial professionals is probably helpful across borders, but the rest of the post is based on US tax laws.

Executive summary: Helping loved ones optimize their finances, especially in their 60s and beyond, can significantly increase their lifetime giving potential with a relatively small time investment.

Key points:

This comment was auto-generated by the EA Forum Team. Feel free to point out issues with this summary by replying to the comment, and contact us if you have feedback.

Within a tax-exempt account like a traditional or Roth IRA or 401k, you can sell assets in the account and reinvest the proceeds without forgoing the tax advantage so long as you do not transfer money from within the account to outside of the account. As soon as you transfer money to e.g. your bank account, that money loses its preferred tax treatment and you are not able to transfer it back to the tax-exempt account beyond the annual limits (e.g. $7,000/year in 2024 for IRA contributions among people under 50).

This is not true. You actually have 60 days:

https://www.irs.gov/retirement-plans/plan-participant-employee/rollovers-of-retirement-plan-and-ira-distributions

- 60-day rollover – If a distribution from an IRA or a retirement plan is paid directly to you, you can deposit all or a portion of it in an IRA or a retirement plan within 60 days. Taxes will be withheld from a distribution from a retirement plan (see below), so you’ll have to use other funds to roll over the full amount of the distribution.

I would not encourage anyone to try to make clever use of this "float", but it's there.

Interesting! Thanks for adding this.

Last summer, my late-60s parents asked me to help tidy up their investments and advise their giving over time. After ~150 hours of Googling, working with a financial advisor & an estate planner, and collecting thoughts from friends & finance-y EAs, we set up a plan that I feel good about. I shared our learnings with other family members of similar ages, and they made changes to their investments that I think will significantly increase their lifetime giving potential.

I am not a financial professional, and I strongly recommend that anyone consult with a professional before making changes to their investments. More information on how to hire a financial professional can be found in this section of the post. This post is specific to the US context.

I’m writing this post because:

In this post I write about:

I’m sure I’m missing a lot of important material on this topic. For example, I haven’t looked into the laws and considerations for gifting property (either to charity or to an heir). I would appreciate it if readers leave comments to enhance this post and help others use their resources to do more good.

To close this preamble, I just want to recognize that this process can be overwhelming. You may have circumstance-specific questions not covered by online resources - that’s perfectly normal. The upside of improving (even if not perfectly optimizing) loved ones’ investments is potentially so high, and the cost of reaching out is so low, that I highly encourage you to consider it. Had I thought to do this ten years ago, my family members likely would have been able to save dozens of additional lives through their giving - in this sense, the stakes of inaction couldn’t be higher.

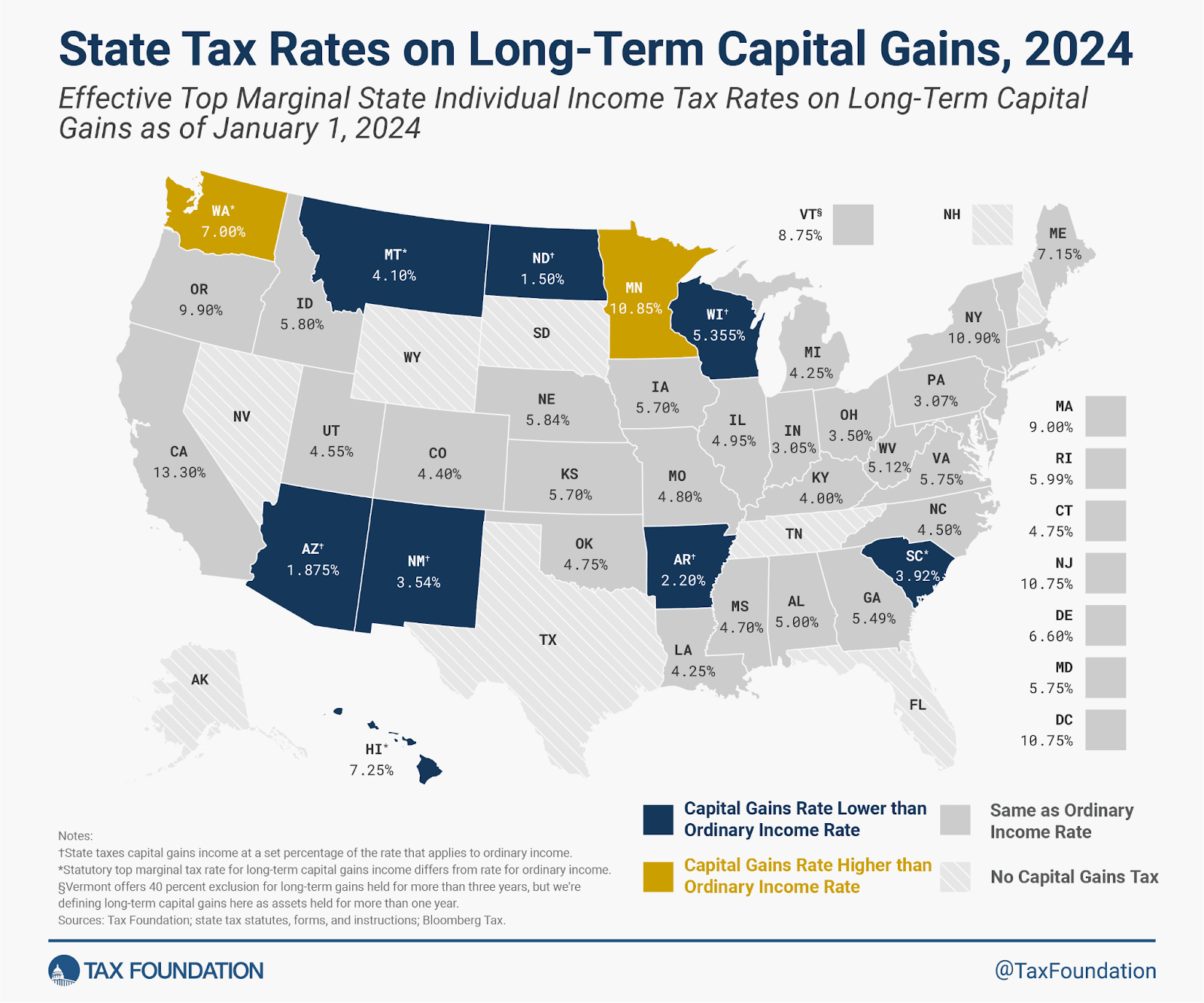

Here is a non-exhaustive list of rules and regulations that may affect decision-making around portfolio changes in taxable accounts. I would highly recommend speaking to a financial professional about these and other laws that may apply to your situation:

| 0% | 15% | 20% | |

| Single | Up to $47,025 | $47,026 – $518,900 | Over $518,900 |

| Married filing jointly | Up to $94,050 | $94,051 – $583,750 | Over $583,750 |

My parents are happy to use a high variance strategy for their investments (e.g. all equities) if they can also ensure they have enough to retire on (e.g. by adjusting their approach if markets fall or if a big unforeseen expense comes up). They are agnostic as to when they donate to GiveWell (thinking that increases in the marginal cost to save a life roughly keeps pace with the nominal returns of the stock market).[7]

My parents also have a uniquely strong preference for donating in cash rather than appreciated stock. They have access to a type of counterfactual donation match that is available only if they give in cash (though not literally physical bills). I expect this post will be relevant to readers whose family members do not share these idiosyncrasies. But in anticipation of questions like “why not set up a Donor Advised Fund?”, I wanted to open with this.

On the donation tax-efficiency/counterfactual bonus side of things, here (1, 2, 3, 4) are a few EA forum posts that offer different strategies for increasing the impact of donations. The general principle that I expect would guide many donors is bunching donations and donating appreciated stock rather than cash. Exceptions to this may include:

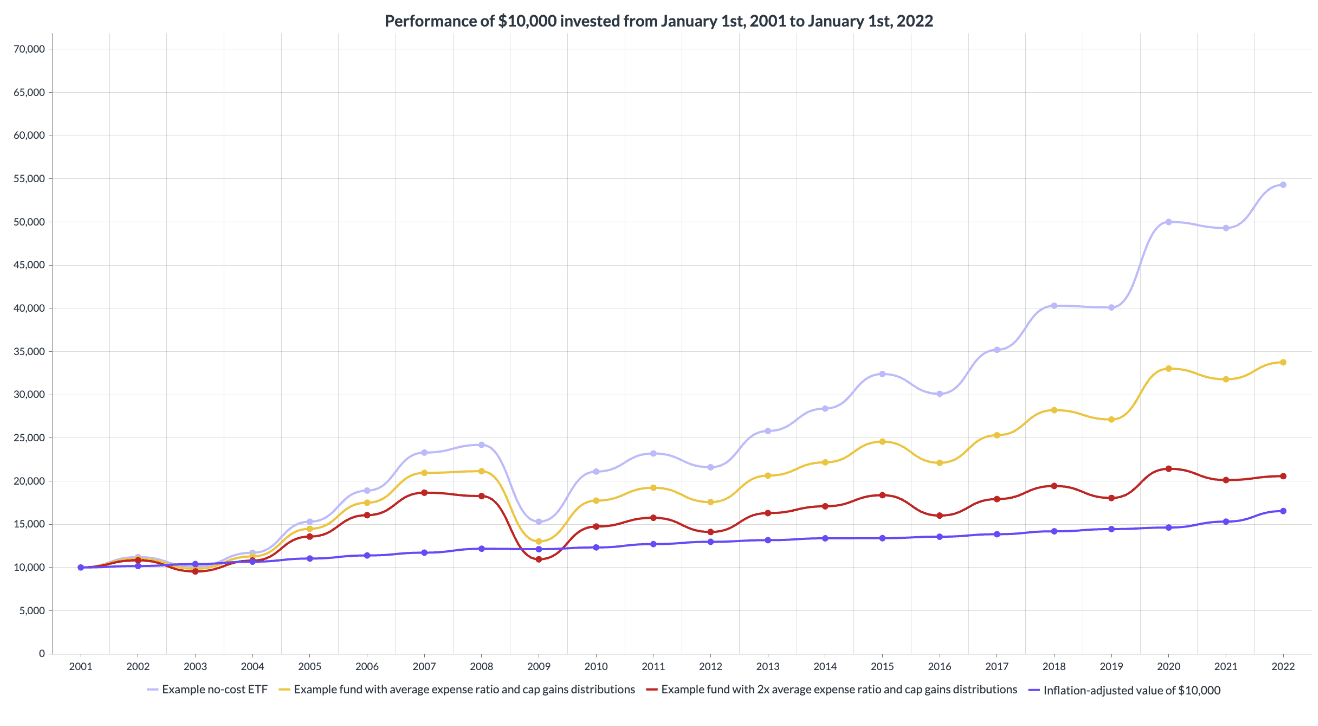

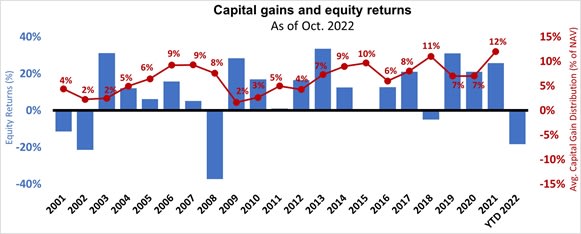

In my parents’ non-tax-protected account, they held a collection of actively managed mutual funds and individual stocks. Many of these mutual funds had expense ratios between .7% and 1.5% per year with capital gains distributions rates between 5% and 10% per year. As context, here are the US averages for mutual funds’ capital gains distributions as a percentage of net asset value between 2001 and 2021:

Capital gains distributions are usually taxed at the state and federal long-term capital gains rate, so the cost of capital gains distributions depends on one’s income. Per a 2021 ICI report, the average expense ratio of actively managed mutual funds was .68%.

Combining these effects, for a married couple living in California making $120,000/year here is how $10,000 would have performed in:

The punchline numbers of what $10,000 invested in January 2001 would be worth in 2022 in the following funds are:

This is a big difference - money invested in a no-expense, no capital gains distributions ETF would have grown by an additional 60%[10] more than money invested in actively managed mutual funds with the US average expense ratio and capital gains distributions. Because of this, I wanted to convert as many actively managed mutual funds into target ETFs as possible, balanced against the tax incidence this would bear. A clean version of this looks like selling offsetting pairs of investments that have equal amounts of appreciation and depreciation.

(Un)fortunately, mutual funds that have been invested in the market for decades generally go up in value, so the amount of depreciated investments in my parents’ account had depreciated by less than the dispreferred appreciated investments had appreciated. This means that we needed to make tradeoffs between selling some investments at a capital gain and having a higher tax bill this year, or holding those investments and paying taxes and fees over time. Here is a tool I created to help make sense of this tradeoff.

Other ways of offloading dispreferred investments include donating appreciated stock or transferring appreciated stock to a tax-exempt entity like a donor advised fund or charitable remainder trust.

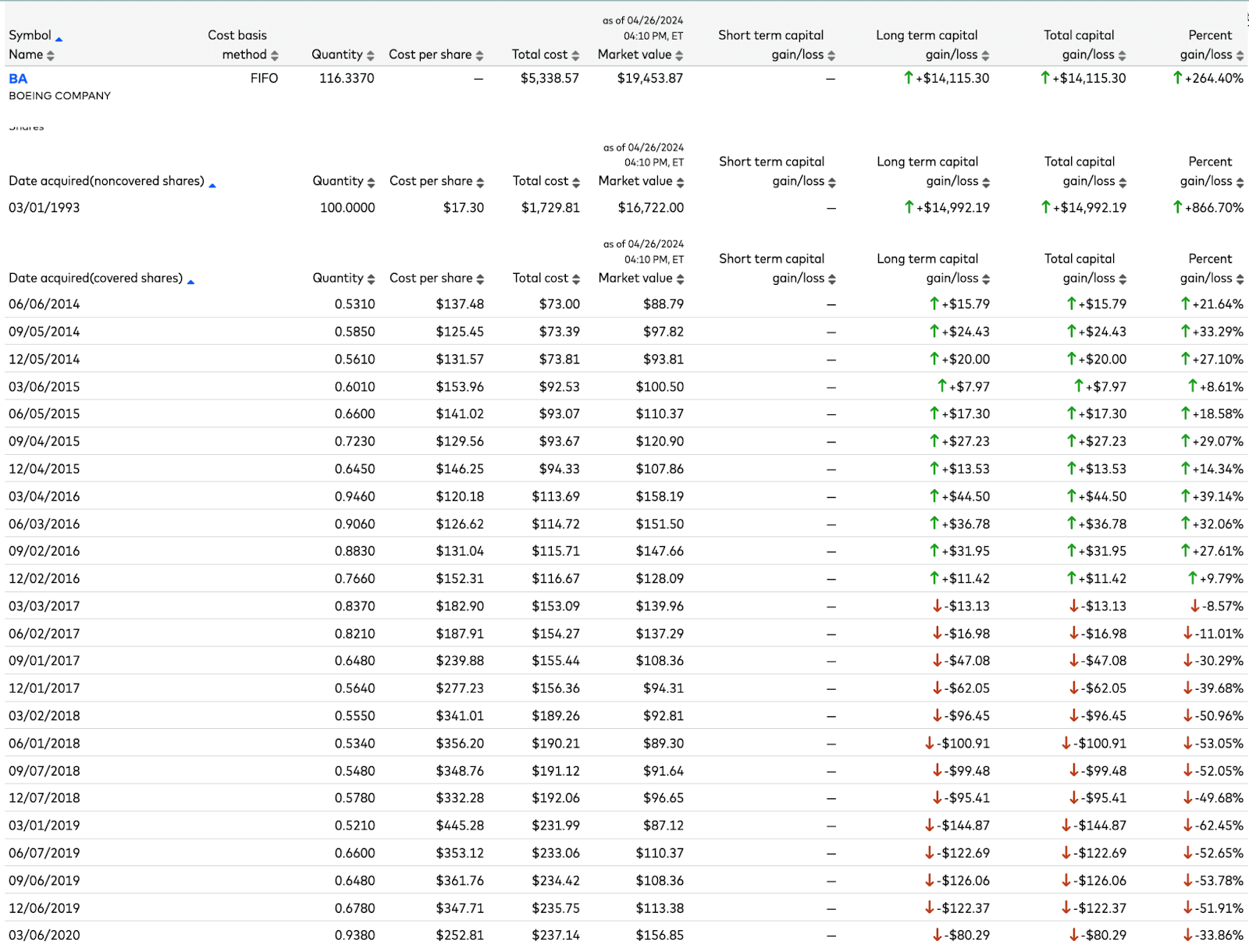

From this information, it looks sensible to hold this Boeing stock. Boeing is a blue chip company that probably has similar expected returns to the total stock market, and our investment has appreciated 264% so eating these long-term cap gains would be pretty brutal. But by checking lot details, we see the full story:

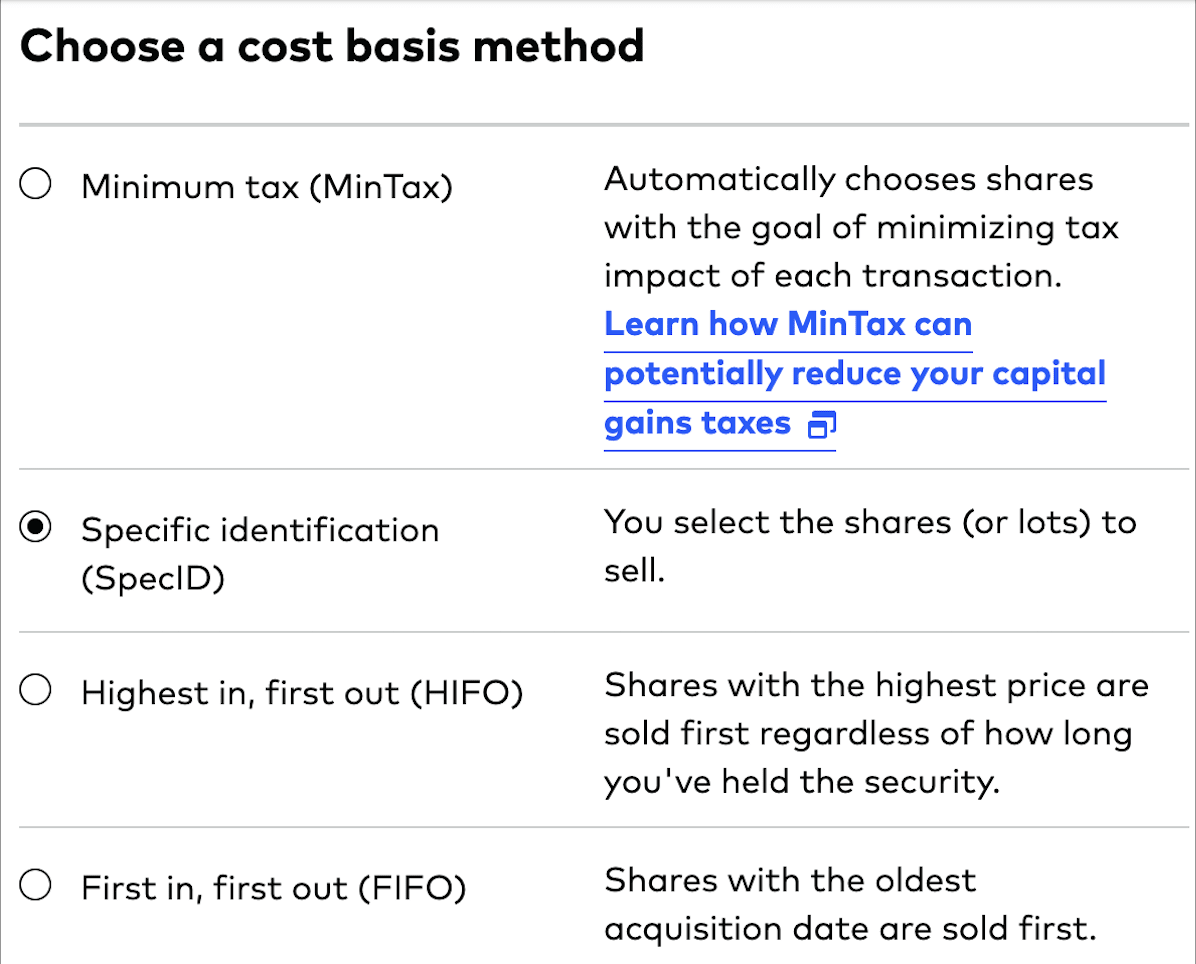

Of these 116 Boeing shares, 100 have appreciated by 866%, eight have appreciated by 9-39%, and eight have depreciated by 8-62%. If we were looking to sell shares of Boeing and realize some long-term capital losses, we could simply set our cost basis method to SpecID and sell the specific eight shares that have depreciated.

A best practice is to investigate the unrealized capital gains and losses of each lot in your loved one’s taxable portfolio, not simply the average across lots. For stocks and ETFs with reinvested dividends, you may be able to find unrealized capital losses among these dividends (this was the case in the above Boeing example).

Unfortunately, many major brokerages no longer provide their customers with free financial advising. For example, Vanguard charges .3%[12] of assets under management per year to provide professional tax and advising service. For many investors, it makes more sense to hire fee-for-service professionals than a “dedicated financial advisor” who charges a percentage of assets under management every year. I’d also recommend coming in with specific, well-scoped questions about how you want the advisor to use the time you’re paying for. This could just be “please review my current plans and catch any blind spots”.

I found XY Planning Network to be the best resource for finding fee-for-service finance professionals. It’s a directory of CPAs and CFPs for hire that allows you to filter by expertise in the specific subdomain you want, and view hourly rates and reviews. I recommend working with professionals living in your state so that they’re aware of any state-specific laws that might apply to your situation.

In my opinion, most professionals aren’t going to be knowledgeable/competent in the areas you’re looking for help with. One approach to finding a good advisor is to send templated emails and conduct short interviews with people who are willing to have a free introductory call - here is a sample outreach email and set of interview questions to test competency. I ended up signing up for free informational calls with four professionals and hiring one of them for $1,500 to put together their recommendations for my parents.

Once you do hire a finance professional, I recommend setting a very specific scope of work at the beginning of your engagement. Certain projects like estate planning have standardized deliverables, but for work with CFPs or CPAs you may want to outline a work plan - here is a sample scope of work.

Word to the wise: Be aware of upselling when working with financial professionals. Some finance people may get a kickback even from products that aren’t directly affiliated with them or their company (e.g. “have you considered an annuity?”) and may not disclose those financial ties to you when making recommendations. Despite it being difficult to fully align incentives with finance professionals, I think they have a valuable perspective to add. If you’re ever unsure about their recommendations, you could always check with friends or ask for a second opinion.

Once again, I am not a financial expert and I am not trying to give you financial advice. I don’t have strong views on where to invest, but I do think it’s important to be skeptical of investment theses that deviate from conventional wisdom. I.e., the burden of proof should be on the nontraditional strategy to demonstrate why it is better than holding a low-cost, diversified portfolio. Choosing where to invest is a big call, and I think it’s wise to carefully construct a strategy that makes sense for your loved one.

Here’s an example of a way that one could be misled: mutual fund companies will “incubate” funds for their first few years of operation to “build up a track record”. In practice, this lets funds make the best-performing incubated funds public (performance mainly being driven by short-term variance rather than brilliant fund management). This can also skew how sectors appear to perform because sectors are represented by the funds that have continued to exist for, e.g., 10 years, not the funds that were around for one year and subsequently shut down.

Here is a doc with a few links on historical returns by sector, large cap vs small cap, growth vs value, and a tool for testing merged approaches for anyone who wants to do their own research.

At the start of this project, my parents and I overhauled their information security. My parents worked with an estate planner to designate GiveWell as the beneficiary of their IRAs and establish a will that could transfer leftover money to their descendants or GiveWell at the time of my second parent’s passing.

Once my parents and I developed a firm understanding of relevant tax laws, felt confident in where we wanted to invest, and created a dynamic budget[13] for their retirement, we took the following steps:

If you have questions after reading this post and are interested in setting up a call, feel free to schedule a time on my calendly. Again, I am not a financial professional so I will not be able to offer financial advice, but I’m happy to be a sounding board and recommend resources.

Thanks for taking the time to engage with this post and for considering taking action with loved ones in your life. The process has brought me and my parents closer; I think financial security and the ability for a loved one to do more good with their life’s savings is one of the greatest gifts you can give.

Within a tax-exempt account like a traditional or Roth IRA or 401k, you can sell assets in the account and reinvest the proceeds without forgoing the tax advantage so long as you do not transfer money from within the account to outside of the account. As soon as you transfer money to e.g. your bank account, that money loses its preferred tax treatment and you are not able to transfer it back to the tax-exempt account beyond the annual limits (e.g. $7,000/year in 2024 for IRA contributions among people under 50).

E.g. If the loved one had a stock that had appreciated by 20% and sold it the day before their death, they would owe capital gains tax on that 20% appreciation. If their spouse sold the stock the day after their death, the spouse would not owe capital gains. The holding period for inherited investments is automatically considered to be more than one year, so the inheritor will always pay capital gains on any appreciation at the long-term cap gains rate (e.g. if they don’t get around to selling the asset for a few months after inheritance).

Avoiding a “step down in basis” (the inverse scenario where a passing loved one holds investments with unrealized capital losses) is more complex and may not have an elegant solution. Your loved one may want to sell off unrealized capital losses well in advance of their passing whenever they are able to write these losses off against capital gains.

For many people, transferring money they intend to donate into a Donor Advised Fund can be sensible because taxes from ownership in a taxable account such as capital gains distributions and dividends can exceed DAF fees even for buy-and-hold investors. However, retirees may not know how much they can donate throughout the rest of their life given uncertain costs such as long-term care or market crashes. Because of this, I think this tool is worth exploring even for DAF-holders.

A costly estate planning software subscription for finance professionals that isn’t really worth paying for unless a significant share of their work is spent on estate planning.

These higher rates fully kick in at different income thresholds (i.e. it's better to have a $205,999 MAGI than $206,000 as a joint filer, because $206k would automatically cost you an additional $1,677). In practice, it can be hard to forecast your MAGI because for older investors it can depend largely on investment income, which is highly variable. Assuming you have no ability to predict, this works out to be functionally around a 2.2% additional tax on capital gains of one spouse qualifies for Medicare and a 4.4% additional tax on capital gains if both spouses qualify for Medicare.

I recognize that this is my parents’ idiosyncratic preference, not a fundamental law of nature. Much has been written about giving now vs giving later - here’s the EA forum archive on donation timing.

Source: Russell Investments blog.

I used this historical stock market calculator. For the first year (2001), I calculated the average capital gains distribution and expense ratio example by multiplying the 4% capital gains rate of capital gains distributions from the above graph by 24.3% (15% long-term capital gains tax rate + 9.3% California state long-term cap gains rate for joint filers making $120,000) to get .972% in capital gains distributions costs.

Then I added .68% in expense ratio costs to get 1.652% in overall costs. Then I multiplied the 11200 value of investing $10k from the historical stock market calculator from Jan 2001 to Jan 2002 by 1.652% and subtracted the product from $11200 to get $11,014. From 2002-2003, I plugged in $11,014 as my starting value, rather than $11,200 to account for compounding returns.

This is likely an underestimate, because an unmodeled cost here is dividend yield percentage (the percentage of an asset’s value paid out as a taxable dividend). Fee-conscious ETFs and index funds tend to have low dividend yield percentages, whereas actively managed funds tend to have higher dividend yield percentages. Even disregarding taxes and fees, the total stock market tends to return more than most actively managed funds due to broader exposure to the best performing stocks. This is also an underestimate for investors with higher adjusted gross incomes, who would have additional taxes on their capital gains distributions like Net Investment Income tax, higher IRMAA payments, higher state cap gains rates, and more.

Note: my parents reviewed a draft of this post and approved of its publishing.

Vanguard told me that the process of unenrolling in its financial advising program takes months, so signing up for this service with the intention of dropping it a few days later is unfortunately not as enticing as it may seem.

I.e. “Here's our plan for lifetime giving and investing right now, and here’s how we’ll adjust our plan based on changes in circumstances (e.g. market downturns and a potential need for long-term care coverage)”.

A nice feature of holding a few different types of semi-uncorrelated holdings for my parents is that when they sell off investments to donate in the future, they’ll have a few options to choose between to reduce expected capital gains.

Yield and Spread is a Profit for Good business that provides financial advice, particularly to help further effective giving. All the profit the business generates goes to effective charities. Thought it would make sense to give them a shout out here.

https://www.yieldandspread.org/