Introduction

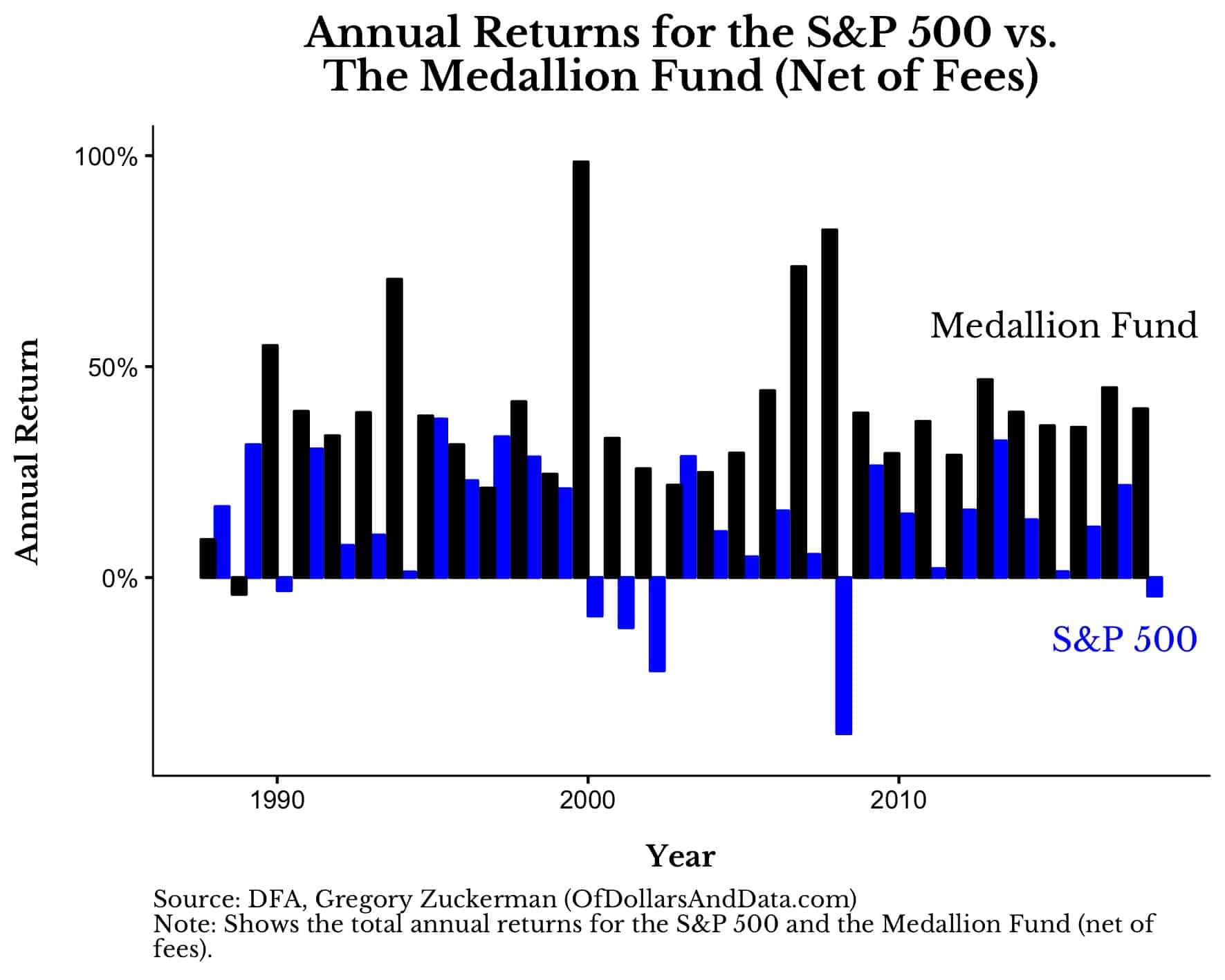

In this post I’ll discuss how achieving a high rate of return on investments could strengthen a piece of the patient philanthropist argument set forth by Philip Trammell, and go into detail regarding how good the best investments can be. For reasons I’ll explain later, I will limit the investment vehicle time horizon to a few decades. Discussions on the EA forum and in Trammell’s paper about annual discount rates and average annual financial returns consistently use single digit percentages (0.5%-2.3% for discount rates and perhaps 5-7% for investment returns). However, these investment returns are average returns, not the very best returns. The EA community has consistently espoused the idea that the very best charities are 10-100x better than the average charity. After some brief research, I have concluded that the same multiplier holds for the very best investment vehicle. Since its inception in 1988, the Medallion Fund from Renaissance Technologies has posted average annual returns on investment of 39% after significant management fees. To get a sense of how fast these annual returns compound, Cornell has concluded that $100 invested in 1988 would be worth almost $400 million in 2018. This fund has posted annual returns of 98% after fees in 2000 during the dot-com crash and 82% after fees in 2008 during the Great Recession, which indicates that it actually hedges against risk, unlike most other high-returning investment vehicles.

To put it simply, I believe that if a patient, well-connected philanthropist had the ability to invest in the Medallion Fund today, it is likely to be the very best thing that person could do with their money.

A short disclaimer: I am not affiliated in any way with the specific institutions or persons I mention, and I am not in the quantitative trading or hedge fund industry. This post is not intended to be personal investing advice. This is my first post on the EA forum, so I apologize in advance for any ways that it does not conform to the norms of the community. I am also relatively new to EA in general and have almost certainly missed citing some important work related to this topic.

ITN Framework

I’d like to take a first pass at applying the ITN framework to the issue of high-yielding investments.

Importance: High-yielding investments could significantly increase the total amount of capital available for charitable giving in the relatively near-term. Since monetary giving is a core part of “doing the most good”, I will score this category HIGH.

Tractability: The Medallion Fund is only open to employees of Renaissance Technologies, which has a remarkably low turnover rate. It keeps this structure as a strong recruiting incentive, and popular media reports that it employs many of the top minds in the field. Joining the company would be difficult, and perhaps not the best use of a brilliant mind. I see two possible routes to gain tractability. First, the EA community could reach out to Renaissance Technology employees like REG reaches out to prestigious poker players. Perhaps the employees could lobby to increase the size of the fund (currently $10 billion) to accommodate EA money from Founder’s Pledge or Open Phil. I will score this idea LOW. Second, it seems there is significant room for active research in identifying the best investment vehicles that do allow for investment of charitable giving funds. I will score this idea HIGH.

Neglectedness: Achieving a high rate of return on investment is probably one of the least neglected topics in the world at large. However I have seen surprisingly little engagement from the EA community on this particular topic, possibly due to the only recent publication of Trammell’s 80,000 Hours podcast, his patient philanthropy paper, and the two blog posts by Dickens and Hoeijmakers I reference above. None of those sources directly reference the question of optimizing high-yielding investments, but they do discuss issues relevant to the broader topic. Trammell remarks, “… advocating long-term investment is still far from mainstream in philanthropic circles, including the EA movement, and very little effort has been put into its implementation.” I will score this category MEDIUM.

Discussion

An annual return of 39% (even assuming 30% of those returns lost to capital gains taxes) simply dwarfs any plausible discount rate. For the standard metric of r – g, the Medallion Fund is an example of r >> g which makes investing highly compelling. Looking at just investing money for a single year, charitable giving options do not dramatically change in expected value in one year so increasing giving by 39% dominates the expected value calculation. An argument against investing by claiming the unique hingeyness of history would need to meet the bar that this particular year is far “hingier” than any recent past or future years (for example if a world government was being set up this year by some sort of popular vote that could be influenced by campaign lobbying, see MacAskill). Perhaps a compelling investment strategy would be to “play poker with history”, where the philanthropist invests (folds their cards) most of the time until a particularly opportune moment when they go “all in” on an excellent hand (see Trammell).

Since the Medallion Fund has only existed for 30 years, I have restricted my time horizon of this particular investment to 30 years in the future. It seems reasonable to expect that this particular fund may lose its edge in the next few decades due to employee turnover, advances in AI that this fund does not capitalize on, or a change in the stock market regulations that allow this type of quantitative trading. This time horizon also avoids thorny issues of estimating the success of investments over centuries, where there are few promising examples. It also reduces concerns of not following through, disappearing opportunities, and indefinitely postponing giving brought up by this post from the Global Priorities Project and this post from Giving What We Can.

A few relevant criticisms were put forth by Wayne Chang in a comment on Hoeijmakers’ forum post. He comments that high-risk, leveraged strategies have historically been unsuccessful over long investment periods. I grant this point in general, but the Medallion Fund has successfully produced high yields over the past thirty years without resorting to high-risk strategies that tend to fail during downturns. Rather, the fund makes many smaller trades that are slightly more likely than average to net a positive return. Secondly, he mentions that when funds grow too large, they must compete with themselves and are less likely to beat the market because they hold a significant fraction of markets they invest in. To combat this, the Medallion Fund has capped the total fund size at $10 billion which means a substantial amount of money ($3.9 billion on average given annual returns) must be taken out of the fund every year. Capping fund size is rare for endowment-type funds (common among philanthropists) since their goal is growing the total size of the fund over time. If the EA community does create a large high-yield fund, the fund should have a specific mechanism to address this major concern.

I’ll make a few comments comparing the Medallion Fund to other investment vehicles. The annual returns have certainly been remarkable, but it is worth considering whether other non-traditional investments could have a comparable performance. For example, Bitcoin increased in value from $0.0008 to $20,000 per coin between its launch in 2009 and its peak in 2017, which is strictly speaking a higher return on investment than the Medallion Fund. The total Bitcoin market cap in 2017 was approximately $100 billion. The difference between these two, in my view, comes down to Bayesian priors and expected value considerations. When Bitcoin was inexpensive, reasonable priors would have placed the expected value of an investment in Bitcoin relatively low, particularly given the strong possibility that the cryptocurrency could have crashed to become functionally worthless. As the value of a Bitcoin increased, updating priors would be the rational course of action, but by then the investment would have been much less compelling than in 2009. This concept holds for successful startups as well. The initially low expected value can be broken down into a large chance of zero value and a small chance of extremely high value. Investing in vehicles like this can be thought of as “hits based investing” which is comparable to the “hits based giving” approach of Open Philanthropy. This requires a much higher tolerance for risk than the Medallion Fund and annual returns are strongly dependent on the ability of the investor to choose “hits”.

Takeaways

· Some investment opportunities are extremely high yielding and the EA community may find significant value in identifying such opportunities

· High enough yields tend to dominate the expected value calculation for charitable giving

· The Medallion Fund in particular is an example of an investment vehicle that is 10-100x better than average

Citations

80000 Hours feat. Trammell (2020). How becoming a ‘patient philanthropist’ could allow you to do far more good.

Bitcoin price history. https://www.investopedia.com/articles/forex/121815/bitcoins-price-history.asp

Cornell (2020). Medallion Fund: The Ultimate Counterexample?

Dickens (2020). Estimating the Philanthropic Discount Rate (EA Forum).

Global Priorities Project (2015). Give now or later? What to do when the order of your actions matters.

Greaves (2017). Discounting for public policy: A survey.

GWWC (2014). Donating vs. Investing.

Hoeijmakers (2020). The Case For Investing to Give Later (EA Forum).

MacAskill (2019). Are we living at the most influential time in history?

REG https://reg-charity.org/. Accessed July 26, 2020.

Trammell (2020). Discounting for Patient Philanthropists. Working paper (unpublished). Accessed July 26, 2020.

{kind=link}

It seems like the obvious problem with this is that identifying the best investment opportunities is hard.

More specifically, I think EA really shines when identifying the problems nobody really cares about or is trying to solve already (eg, evaluating charity cost-effectiveness, improving the long-term future). It makes sense that there would be low hanging fruit for a competent altruist, because most of the world doesn't care about those causes and isn't trying. So there's no reason to expect the low-hanging fruit not to already have been plucked.

Investment, on the other hand, gives EAs no such edge. The desire to make a lot of money seems near universal, and so you should expect the best investment returns to have already been taken. Because a lot of optimisation power is going into investment and into finding the best sources of returns. So I can't see any clear edges of EAs here.

Arguably EAs have an edge in terms of caring an unusual amount about long time horizons? So I could believe that there are neglected investment opportunities that aren't great in the short term but which sound excellent over 10+ year time horizons. And I'd be excited about seeing thought in that direction. This is still an area a lot of other people care about, but I think most investors care about shorter time horizons, so I can believe there are mispricings. It'd definitely require looking for things that aren't also obviously good ideas in the short term though (ie not the Medallion Fund)

Long time-horizon institutions like university endowments, pension funds etc might be interesting places to look for what good strategies here look like.

It also seems plausible than an EA worldview isn't fully priced into markets yet, eg if you believe there's a realistic chance of transformative AI in the next few decades, tech/hardware companies might be relatively underpriced. Or more generally GCRs, like climate change, antibiotic resistance, risks of great power war, artificial pandemics might not be sufficiently priced in? (I'd have put natural pandemics on that list, but that's probably priced in now?)