It has been quite a past two weeks, with different spheres in deeply divided narratives. In addition to the liberation of Kherson City, the midterm elections that of course took forever to resolve and the ongoing hijinks of Elon Musk taking over Twitter, there was the complete implosion of Sam Bankman-Fried (hereafter ‘SBF’), his crypto exchange FTX and his crypto trading firm Alameda Research.

The situation somehow kept getting worse several times a day, even relative to my updated expectations, as new events happened and new revelations came out.

In the wake of those events, there are not only many questions but many categories of questions. Here are some of them.

What just happened?

What happened in the lead-up to this happening?

Why did all of this happen?

What is going to happen to those involved going forward?

What is going to happen to crypto in general?

Why didn’t we see this coming, or those who did see it speak louder?

What does this mean for FTX’s charitable efforts and those getting funding?

What does this mean for Effective Altruism? Who knew what when?

What if anything does this say about utilitarianism?

How are we casting and framing the movie Michael Lewis is selling, in which he was previously (it seems) planning on portraying Sam Bankman-Fried as the Luke Skywalker to CZ’s Darth Vader? Presumably that will change a bit.

This post is my attempt to take my best stab at as much of this as possible, give my model of what happened and is likely to happen from here, what implications we can and should draw, and to compile as many sources as possible that I have found useful.

This is a fast-moving complicated situation that involves a lot of lying and fraud. Anyone attempting to sort it all out, especially quickly, is going to make mistakes. I decided that this was the time when the value of synthesis exceeded the cost of such errors. Still, doubtless there will be mistakes here. I will correct them as they are discovered, either by myself or others. I apologize for them in advance.

Thus I highly encourage you to read this post on the web rather than via an email or RSS version, in case there have been substantial revisions. There have as of yet not been any substantive revisions since publication, which was the morning of 11/17/22. The original version (and the one I will try hardest to keep updated) is here.

Also, yes, long post is long. By all means read only the sections you care about.

What The Hell Happened?

Background: FTX is a crypto exchange largely owned and run by SBF. Alameda Research is a prop trading firm owned by SBF. FTT is FTX’s exchange token, where they commit a portion of profits to buying back FTT. Thus, FTT is a non-registered security, functionally similar to junior non-voting stock in FTX.

The events of the past week, and the proximate cause of them, seem to have gone as follows, with some events likely slightly out of order or happening simultaneously.

Alameda Research, SBF’s crypto trading firm, has its balance sheet leaked.

The balance sheet contains a lot of FTT, such that if FTT loses its value it is not clear that Alameda would remain solvent.

This raises questions. Some people notice. Caroline, CEO of Alameda, says this is incomplete and that Alameda is fine.

CZ, head of Binance, who had been in various battles with SBF, notices. He announces the intention to sell >$500mm of FTT, but does not actually sell.

Alameda offers to buy all his FTT at $22/coin, almost full market price at the time but a deal cannot be reached.

Other people sell a lot of FTT. There are not other buyers. Alameda spends capital trying to defend the $22 price, and ultimately fails. They continue to sell everything they can to support FTT and to pay FTX depositors, but ultimately cannot keep pace.

SBF says that FTX deposits are backed 1:1, that customers are fine, everything is fine (narrator: he lied, they were not fine.)

There is a run on FTX as customers withdraw money. $5bb is taken out.

FTX is forced to pause withdrawals.

There is something set up whereby Justin Sun sets up funds to allow coins in his ecosystem, such as Tron, to be withdrawn to outside wallets, which causes the value of those coins to spike as people buy them in order to withdraw what they can.

SBF tries to raise capital from various sources. He fails.

SBF calls up CZ and asks Binance to buy FTX. CZ agrees and signs a non-binding letter of intent, subject to due diligence.

CZ looks at FTX’s books, presumably in contrast to everyone else who invested in FTX in previous rounds. Somehow they did previously have a ‘Gaap audit’ the accountants for which are now under investigation.

CZ runs away, saying FTX is ‘beyond our ability to help.’

SBF issues a Twitter apology thread and continues claiming FTX is solvent.

Later withdrawals are enabled for residents of the Bahamas and perhaps other insiders, at 100% of value. Some people who can withdraw sell NFTs at highly inflated prices, then withdraw the proceeds. Bahamas authorities later claim they in no way asked for this or even find it acceptable.

FTX is very much not solvent, at least in part because they stole (‘loaned out’) ~$10bb in customer funds and used them among other things to bail out Alameda, invest in VC funds, buy a large stake in Robinhood, and so on.

We later see a balance sheet (this thread has a photo that’s not gated) and it could not be worse. Matt Levine warns that if you look at it too long you will go insane. It contains claimed billions in assets that are worthless, that they made up themselves while giving themselves most of the tokens like Serum and Maps. With an $8 billion entry described as “hidden, poorly internally labeled ‘fiat@’ account.” See Levine or others for details.

The part where FTX stole the customer funds is discovered along the way.

SBF continues trying to raise capital, the amount he says is necessary keeps growing, now at ~$8bb.

Failing to raise the capital, SBF puts Alameda and FTX (including FTX.US and a host of other corporate entities) into Chapter 11 bankruptcy.

The guy who led Enron out of bankruptcy is appointed to deal with this mess.

It is revealed that SBF had a backdoor in the system allowing him to move any and all funds however he wanted without anyone in the system knowing.

The entire FTX Future Fund team resigns. It is clear that any money not already dispensed will not be forthcoming. There is much worry among charities about where money will come from, including whether they will have to, or be ethically obligated to, return money they have already received.

FTX is hacked, presumably by some insider who may have used the backdoor. Kraken claims to know their identity. They siphon a lot of what funds remain, >$500mm worth, before the remainder is put into offline storage. FTX apps including FTX.US try to access people’s bank accounts and are considered dangerous malware, the websites are to be avoided as well, and so on.

SBF continues to be in the Bahamas, meets with regulators, and is under observation to prevent him fleeing, which he is said to be looking to do and may or may not present a real barrier to him doing so.

FTX shuts down, most everyone is fired and expelled from corporate housing.

Michael Lewis is revealed to have spent the last six months with SBF and FTX, doing interviews for a book about him and CZ. Movie rights are in play.

Throughout, crypto overall falls by ~25% versus where it would be expected to be given movements in inflation expectations and the stock market.

Binance announces industry-wide stability fund, potentially similar to an attempt made to avert the great depression. Binance also reveals it never sold any of its FTT before the bottom fell out. Whoops.

SBF kept talking to reporters while also doing a Tweet thread of single letters at a time, somehow thinking this would… help… matters? He also talked to Kelsey Piper, link to article here. In which he claims that he is still attempting to do right by customers and raise funds and is standing by the fantasy of the ‘balance sheet’ and its interpretation of the situation. Also seems he is continuing to try and raise $8bb off that same balance sheet, I guess there is nothing to lose there. Congress plans to investigate. Lawsuits have already been filed.

The bankruptcy filing is something else, including the statement (from the man who restructured Enron) ‘Never in my career have I seen such a complete failure of corporate controls and such a complete absence of trustworthy financial information as occurred here. From compromised systems integrity and faulty regulatory oversight abroad, to the concentration of control in the hands of a very small group of inexperienced, unsophisticated and potentially compromised individuals, this situation is unprecedented.’

Or the simple version:

People discovered FTX and Alameda might be insolvent.

SBF and company lie over and over, saying at each point, no, everything is fine.

Everyone sold FTT and withdraw their funds from FTX.

FTT price crashes and FTX runs out of liquid funds.

FTX tries to sell itself to Binance but things are so bad Binance says no. There is no one willing to bail them out, the holes and legal risks are too big.

It is discovered that FTX and Alameda are indeed insolvent, and that FTX sent $10 billion in customer funds to Alameda, and that SBF had a backdoor allowing him to silently transfer funds.

FTX and Alameda file for bankruptcy.

FTX gets hacked, likely from inside. It gets worse.

Or the even simpler version:

FTX and Alameda and SBF were insolvent frauds.

People figured this out, or at least suspected it, and tried to cash out.

FTX and Alameda went bankrupt and were revealed as insolvent frauds.

What The Hell Happened Before That Happened?

Good question. This is my current understanding of the key events leading up to the events of the past two weeks. If I left something off this list, it does not mean it didn’t happen or wasn’t important, this is simply the events that seem salient to me as I write the list.

SBF is influenced by his longtime friend Will MacAskill and others by the principles of Effective Altruism. He adopts naïve utilitarianism, and he decides to become a trader in order to Earn to Give.

SBF leaves his trading job to ostensibly accept a job offer from Will MacAskill to come work in Berkeley for the Center for Effective Altruism. He is on their board. An alternative possibility is that this was a cover story to throw off his former employer and protect his shot at the Japan arb.

SBF discovers (before or after deciding to move out to Berkeley and leaving his trading job) that you can buy Bitcoin (BTC) in America at one price, and sell it in Japan or South Korea at a different higher price.

SBF decides not to work at the Center for Effective Altruism. Arbitrage ho!

He founds Alameda Research in order to take advantage of this opportunity.

Alameda and later FTX are founded explicitly as Effective Altruist organizations, although they rely on commercial investment and seed funding. Early employees are mostly or all EAs. The hiring process filters aggressively for goodness of fit a lot of which is to what extent someone is an EA. They pitch FTX and Alameda as places to go work if you are looking to do good.

He has at least one cofounder, Tara Mac Aulay, but registers the company entirely in his name as sole owner. I do not understand how he was permitted to do this.

Attempts to take advantage of the South Korean arbitrage fail, but attempts to take advantage of the Japanese arbitrage succeed. They make eight figures.

This money then becomes the initial capital for Alameda Research.

Alameda aggressively scales and makes markets and trades in a crypto world where the standards for trading skill are very low and there is treasure everywhere.

There is no reason why the traders involved, given their skills, could not do very well in crypto with that kind of funding. I can say based on my personal experiences that there really was treasure everywhere back then.

It is unknown how Alameda does. This is their 2018 deck, which claims >100% consistent annualized returns (and ‘no risk’). I have seen claims they actually lost the money that was made on the Japan trade through bad trades and recklessness, and that Sam was taking insane risks all over the place, including a likely disregard for legal risks and structures. He was definitely posting Twitter threads justifying exceeding the Kelly criterion.

Sam’s cofounder Tara Mac Aulay and others who had been verbally given equity leave after disagreements over how to run the business, in particular disagreements over risk management and business ethics. Sam uses his sole legal ownership and various other tactics, which people have claimed were gross violations of common sense ethics and very not OK, to cut those people out and retain sole ownership.

Alameda attempts to raise money at 15% interest ‘with no risk.’ Seriously, they said ‘no downside’ and ‘no risk.’

Sam notices that all the crypto exchanges are kind of terrible and that Alameda would benefit from working with an exchange. He founds FTX.

Alameda is FTX’s first customer, making markets and otherwise trading on FTX. All the lines between them are blurred from the start. This is one of many people who report being told to deposit to FTX via sending money to an Alameda account. Everybody knows that they are doing this, and that under normal financial regulations this would not be allowed, but this is crypto and it makes financial sense for both sides if handled properly (which we now know it very much wasn’t).

FTX builds a pretty good product outside of the fraud and the insolvency and the stealing customer deposits, and does a lot of things very well. The competition really is pretty terrible so it doesn’t take much to offer a superior product.

FTX gets initial investment from Binance.

FTX grows by leaps and bounds, gains higher valuations, gets investment from big players, and has a profitable underlying business.

FTX and Alameda were from accounts I’ve seen very much move fast and break things, seat of the pants, do what a handful of people decided was right kinds of places. I can say from personal experience that was plenty good enough in 2018, but that does not mean you can get away with it in 2022.

Over time Alameda’s market making edge degraded as competitors improved, to the point where they were likely losing money on market making. They get into other things like yield farming and venture, then directional news trading.

FTX and Alameda make a lot of money by shilling coins in which insiders are granted tons of locked tokens, and thus that will inevitably later lose all value. They make a lot more than that on paper, but they also make real money too.

FTX and Alameda also then put endless supplies of those same tokens on their balance sheet and claim they are worth billions and billions of dollars. Whereas if they sold them they would get essentially zero dollars.

They seem to have made frequent large directional (often or always long) bets on crypto or major coins, increasingly simply going long things for extended periods during a bull market, which worked out in the examples we know about while being an excellent way to lose quite a lot of money when it backfires.

FTX spends big on ads. FTX Arena. FTX on MLB uniforms. Super bowl.

SBF was hanging out with Tom Brady, I mean how did we not see this coming.

FTX and Alameda make a bunch of illiquid investments, including in Sequoia Capital, Robinhood, expensive real estate, Semafor, buying Good Luck Games and so on. They do it with borrowed money against fake assets whose value they cannot allow to collapse, and perhaps borrow it from Tether. SBF was looking to launch a Substack competitor for some reason. He tried to get in on the Twitter deal. There were billions in such investments, my current best guess from combining various sources is between 3 and 4 billion with wide error bars. How much was from real profits versus investors versus stolen customer deposits is unclear, Caroline says it came from loans backed by crypto but that does not tell us the origin of the crypto, and even if it wasn’t fraud it was still nuts. Alameda was taking huge risks the whole way, it seems, so on the way up they might have made a ton. Notice the parallels to Yahoo and the tech bubble.

FTX also splurges on a whole bunch of other non-ad stuff costing billions.

SBF starts the FTX foundation, devotes eight to nine figures. Long term causes in the EA space, and community development, are flooded with cash.

SBF also invests a lot of money into Democratic politics and the Protect Our Future PAC, with his headline cause being pandemic prevention (a very good cause!), also works on crypto regulation and (falsely with regard to at least handling of customer deposits) testifies before congress, which is a clear federal crime.

While crypto is doing well and BTC is over $60k and all that, all seems well.

SBF goes on a bunch of podcasts in which he says a lot of interesting things, like that he is such a pure expected value utilitarian that he bites the bullet in the St. Petersburg paradox, and his famous description of The Box on Odd Lots where Matt Levine responded ‘you’re saying I’m in the Ponzi business and business is good’ and SBF said that response was super reasonable (although, despite the parallels in hindsight, he was not at the time saying FTX itself was a Ponzi.)

FTX employees were pressured to buy into FTX stock and to store their personal money at FTX. FTX offered 8% interest on USD and BTC deposits.

FTX gets Binance off its cap table in part by giving them FTT tokens. WTF?

SBF, a long time gamer, is known to have been playing League of Legends during investor pitch meetings while also being bad at it. Later after an intervention he switched to Storybook Brawl because he was freezing up during tower battles.

The whole Terra-Luna ‘stable coin’ scheme blows up, precipitating a crisis in crypto and losing a lot of people a lot of money, none of whom can use the excuse that no one could have seen that one coming. I cannot emphasize enough how little sympathy I have on that one.

In the wake of Terra-Luna, several major crypto players including Voyager and Three Arrows Capital are bankrupt. Several such players are bailed out by FTX and Alameda. The current belief is that they did this not to help the crypto ecosystem more generally or to pick up underpriced distressed assets, but rather because not doing so would have caused forced selling of FTT that would have threatened FTX and Alameda, and that this preserved or expanded the presence of customer funds in the FTX/Alameda space that could then be stolen. This is also why various players were pressured to store their money at FTX.

It is not known whether Terra-Luna and the direct fallout also rendered Alameda insolvent without a bailout from FTX. It is still unclear to me exactly how bad things were at this time, or how dependent they were on the non-collapse of FTT and it being treated as a valuable asset.

FTX’s financial regulator was somehow the lawyer who covered up the Ultimate Bet cheating scandal, which also involved interest on deposits and information asymmetries, because why not. Also they claim to have had a GAAP audit of their assets, somehow.

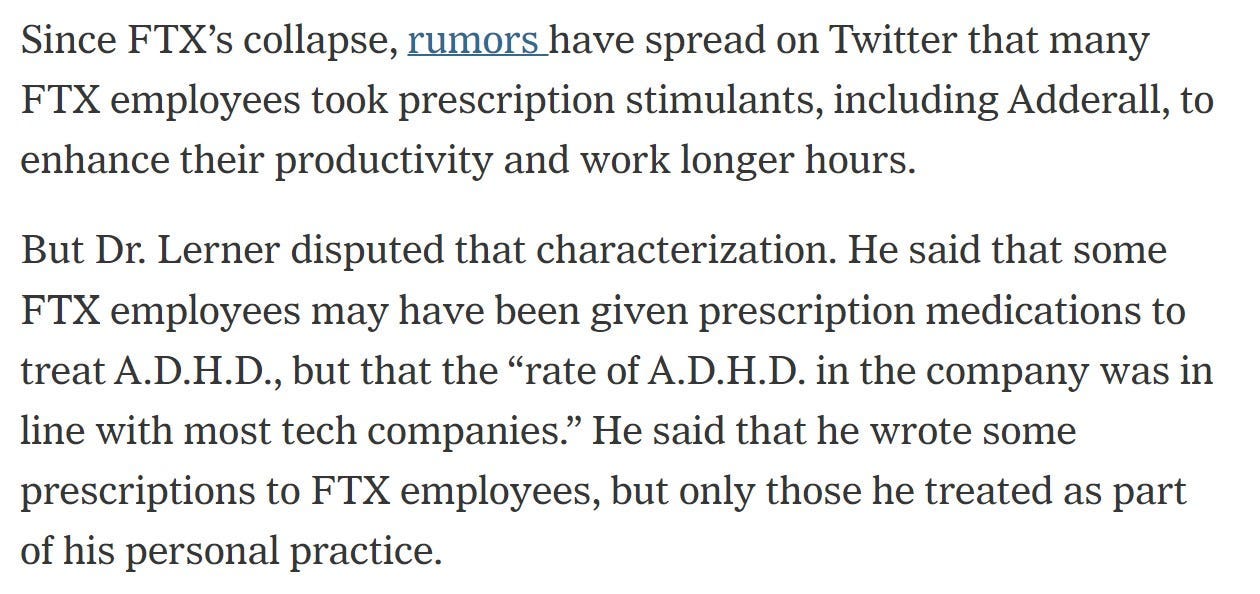

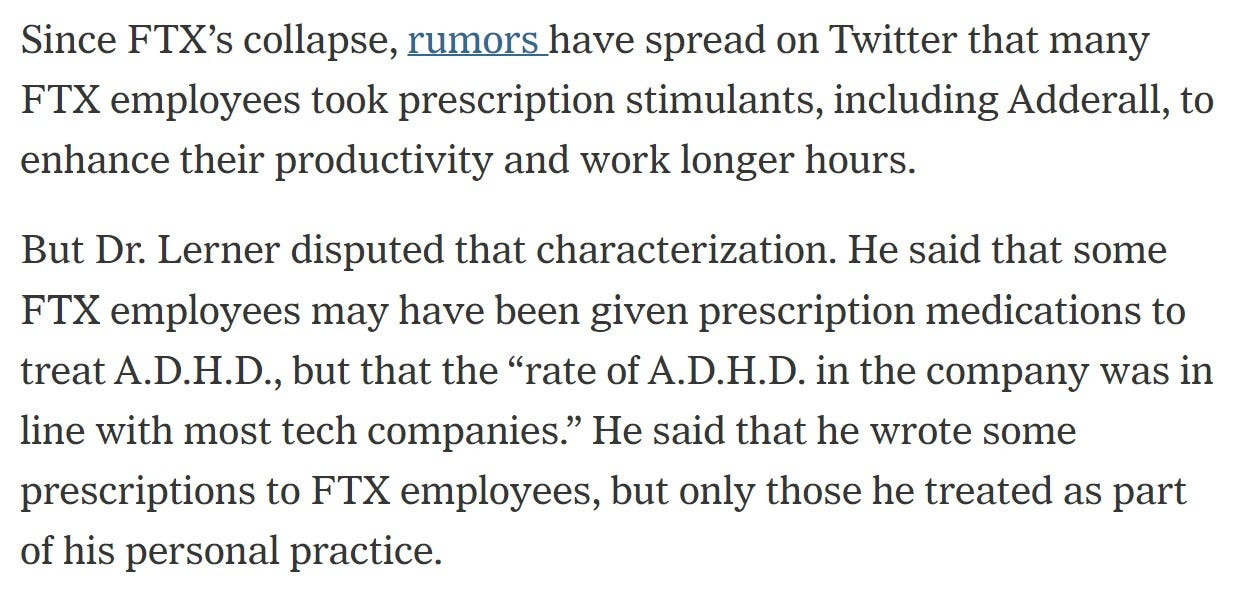

There was widespread use of stimulants by many.

There are claims there were various polyamorous things going on, one source I have says that yes SBF and Caroline dated and were potentially engaged at one point, but it was all serial monogamy. Others say otherwise. I do not see this as central.

Security is so bad that they used an unsecured group email account as the root user to access confidential private keys. Kind of a miracle they were never hacked until recently.

Somewhere along the line, in addition to being illiquid, Alameda and FTX lose really a lot of money, over $15 billion, somehow. We know because they had a bunch of money and made a lot of money, and then Money Gone. Note that ‘lose’ is flexible here, we don’t know the details.

At some point, probably when their loans were recalled in early 2022, SBF started using his backdoor to send customer funds from FTX to Alameda, or alternatively was already keeping customer funds at Alameda for no good reason and then decided to let Alameda use them. It is also unclear for now exactly when customer funds started being sent to Alameda and otherwise comingled and stolen. It could be that it happened at the start, or otherwise well before Terra-Luna and that only accelerated things, or maybe not. Caroline’s story is that this happened when their loans were recalled post-Luna. The default assumption is that, either way, this happened because Alameda was broke at the time or at least highly illiquid. SBF’s alternative claim, in his 11/15 completely insane texts with Kelsey Piper, is that customers sent their deposits to Alameda and they simply never remembered to collect the $8bb in such funds, which ended up as ‘poorly labeled internal fiat account’ on their balance sheet, and which Alameda then used, rather than SBF doing an active transfer. At this point I suppose I can’t quite rule it out.

SBF filmed a Master Class about trading, which is going to be epic.

Alameda investments required the target to store their funds at FTX and use FTX services. FTX deals required various entities to maintain credit lines to Alameda.

SBF was going around trying to raise money in the weeks prior to the incident, which confused a lot of people since he shouldn’t have needed it.

The endgame begins, as detailed above.

Or, the short version once again.

SBF seeks to make a lot of money to earn to give, founds Alameda.

First project is the famous Japanese BTC price arbitrage, worth 8 figures.

Business is not well-run, cofounders leave because of it, SBF cuts them out.

SBF founds FTX, things initially go well, money is made. FTX goes big: big investment at up to $32bb valuation, big spending, big advertising, FTX foundation, etc.

Alameda transforms over time from a prop trading firm that focuses on market making to a combination of longer term illiquid investments and directional bets, effectively taking super risky large long positions and borrowing short to invest long. In general the firm was structurally permanently long and unhedged.

Some bets go well, others go much less well.

In wake of Terra-Luna Alameda’s loans get recalled, a lot of money is lost and various others need bailouts or there is risk of collapse of FTT, and there is opportunity to get more funds into FTX ecosystem.

SBF decides to use his backdoor to send customer funds to Alameda, (or to allow Alameda to spend customer funds they have lying around for some reason)..

Or, the shortest version:

SBF co-founds Alameda, does an arb to make money, they start prop trading.

SBF cuts out cofounders, founds FTX tightly integrated with Alameda.

They increasingly make naked long bets and borrow short to invest long.

When this inevitably blows up Alameda SBF steals FTX customer funds to save it.

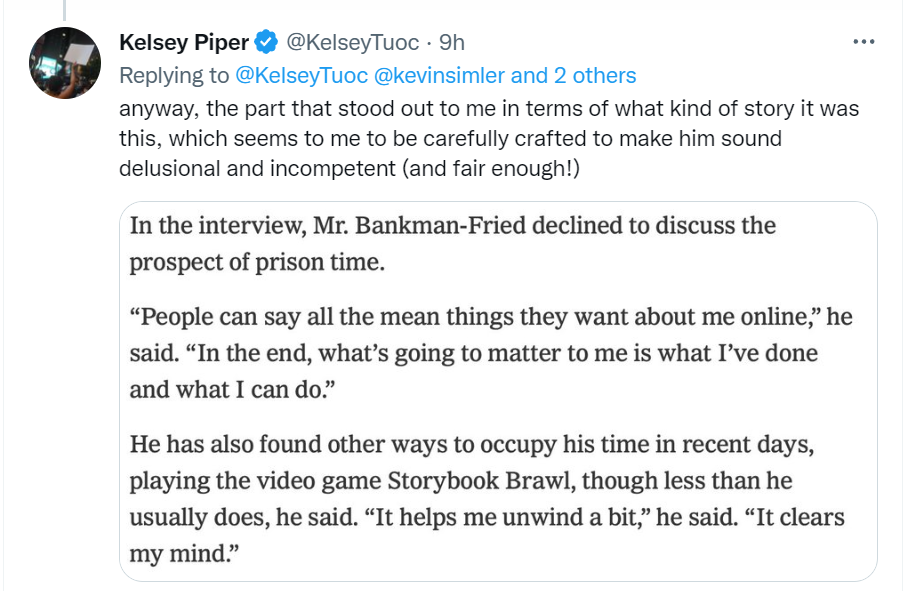

The Kelsey Piper Interview and the Hail Mary

I recommend reading Kelsey’s interview with SBF after it all went down if you have not yet done so. Extreme candor here, unless that too is a front. Also it is completely insane. Includes new theory of ‘no we did not send customer funds to Alameda, we had customers send their funds directly to Alameda and forgot that they still had $8 billion of it that they could use.’

SBF’s biggest regret? Declaring bankruptcy, if not for that everything would be fine, he says. His entire ethical persona was a lie except perhaps for the pure naive utilitarianism. Winning is what matters, ends justify means, no one cares how you got there. And he says he ‘has two weeks to raise 8 billion dollars’ to make customers whole, sticking to the story on his balance sheet.

That is very much not a story whereby someone can raise 8 billion dollars, unless the plan is ‘drive those who look at it insane and then take advantage of their mental incapacity.’ SBF knows this, he knows we know it, it is common knowledge.

So what is going on here? What is the final play?

(None of this post, anywhere, is investment advice or legal advice.)

If SBF did manage to raise 8 billion dollars, how the heck did he do that?

He is selling things that are not on the balance sheet.

The first additional thing he is selling is confidence in the crypto ecosystem. This is why Binance was originally willing to step in before they looked at the balance sheet and ran away screaming. FTX going down took ~$200 billion off the market cap of all crypto. Spending $8 billion to undo a lot of that damage is a collective action problem. There are some very large and very long players in the crypto space.

This also comes with a predictable large sudden increase in crypto prices. If you were to get long now, then buy FTX while making customers whole, then sell at the new price level, you’d presumably make a lot.

FTX could potentially have enterprise value. It was a functional exchange. It has obviously lost all customer confidence, but under new ownership that makes customers whole, who knows what might happen? Especially if the new buyer or group is either clearly safe as houses, or has a clear path to finding a whole bunch of new customers.

SBF is also pitching, by implication, his knowledge and the knowledge of others at FTX. They know a lot about who is in deep trouble, who is and isn’t what kind of scam, and so on. A lot of people would very much like to know all that information, for many reasons.

Finally, SBF is selling SBF. If SBF were to pull off this rescue, that does not get him out of legal jeopardy or mean his reputation and wealth are not shot to hell. It does mean that he pulled off the sale of the century. Whatever you think of him, wow can that person raise money, everyone will say. What a great trader, who has both managed to lose billions - always a plus as Levine points out every so often - and also make them and raise them. Different people place different values on willingness to engage in fraud. Perhaps there are those who would like to then be in business with this person? On extremely favorable terms? Also with a host of evidence of numerous crimes in case he ever tries to get out from under their thumb?

I put a very very low probability on that working, but I realized overnight that I was wrong to put it at zero. If it does happen, we will learn a lot about the world we live in.

Other People Explain or Have Takes

This is a compilation of other people’s explanations and summaries and such.

Milky Eggs posts what they think happened at Alameda Research. Consider reading in full, if you had to pick one source I would pick this one. This seems like an excellent piece with unique parts of the puzzle. Includes a rough guess as to Alameda’s losses and where they came from:

Voyager/BlockFi acquisition: 1.5b

LUNA exposure: 1b

KCG-style algo crash: 1b

FTT/SRM collateral maintenance: 2b

Venture capital: 2b

Real estate, branding, other frivolous spending: 2b

FTT drop from $22 to $4: 4b

Discretionary longs going bad: 2b

Total: 15.5 billion (from above, later below two are added to get to 18.5 billion)

Buying out Binance’s stake in FTX: 2b

Loans to companies that defaulted from the LUNA collapse: 1b

Scott Alexander addresses the pharmacology of the whole FTX situation. Unique perspective and information here.

Doug Colkitt speculates that FTX was an exit strategy once Alameda had become unprofitable, except Alameda became very unprofitable over time and FTX was increasingly a place where liquidity was only provided by Alameda, who got picked off constantly, so the holes kept getting bigger, and FTX was effectively a Ponzi trading scheme where everything was +EV but the casino couldn’t pay the players.

Matt Yglesias offers his thoughts, which can be contrasted with his previous defense of SBF. I do agree that it would be quite bad if people dismissed worthy causes based on their association with bad monkeys. I especially agree that this is very bad for the prospects of us being able to spend money to guard against pandemics, and that this is a very bad outcome.

Fast Company describes the dynamics of what happened, no unique insights, frame is that all of crypto is a house of cards.

Astrid Wilde explains some of the basics in simple terms (no unique info).

Jason Choi thread giving his take on What Happened, with the perspective of this all being super shady from the start with a core philosophy of insane risk taking.

This EA Forum comment from a crypto insider describes some of SBF’s behavior, which has been incorporated above.

Bismark Brief takes the attitude that the main effect will be to weaken the EA movement, especially its moral authority and legitimacy, along with hurting the resources available to tech elites. Also available in Twitter thread form.

Lucas Nuzzi notes FTX may have minted a lot of Serum (SRM) out of thin air to prop up its balance sheet. Except, why? What good does that do? No one was under the illusion they could sell those tokens, so this is some sort of mystical worship of the idea of a balance sheet. Here he highlights a likely FTT bailout in Q2 for Alameda.

Kathleen Breitman of Tezos, also my old co-founder at Coase, offers her take.

SBF did have a working knowledge of game theory and economics, as far as I can tell, although he lacks technical acumen in the crypto/coding space.

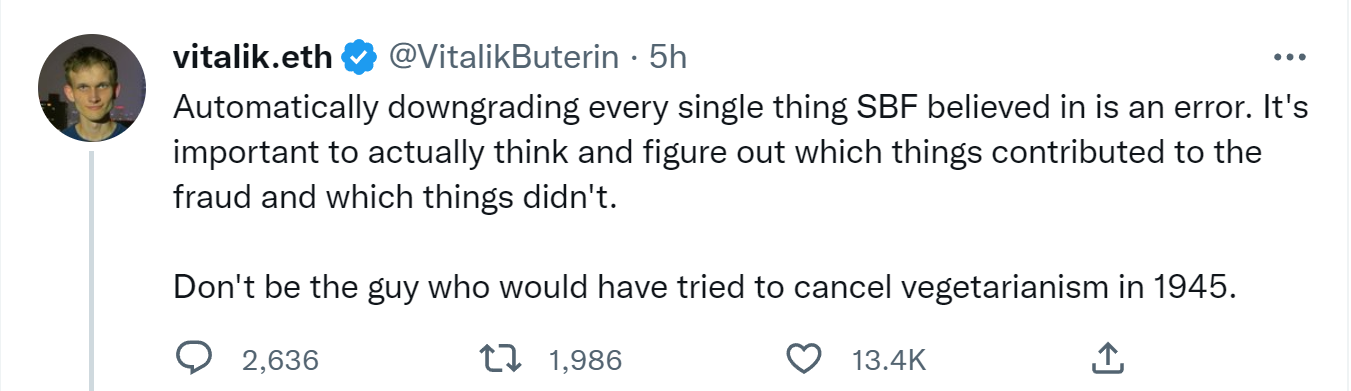

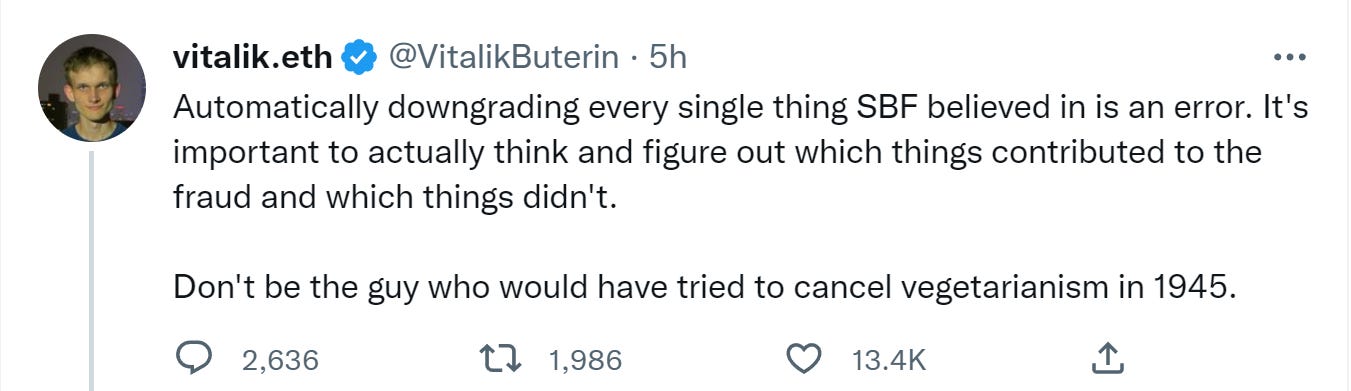

Vitalik Buterin reminds us that all humans, no matter how horribly they screwed up and how much fraud they committed, deserve love.

You raise? I reraise.

Noticing that fraudsters often portray themselves as altruists.

Tyler Cowen as always is here to asks what rises and falls in status. I disagree on Musk’s ability to judge character, you get no credit for saying you smelled BS after the BS is obvious. I also do disagree with most of the crypto players he says will rise in status, unless it is relative to other crypto players. Also ‘being unmarried and male over 30?!?’. This post seems like an attempt to raise and lower status rather than a pure prediction. I would like to think that buying stadium rights and super bowl ads will go down meaningfully in status, yet I expect everyone to forget. Given how much investors these days like potential frauds it might even rise. I would hope that Twitter citizen journalism will gain at expense of MSM, yet that seems to never properly happen no matter how richly deserved.

He also suggests what questions one should be asking, starting with ‘which 19th century novel does this story most resemble?’ I am choosing to ask mostly different questions.

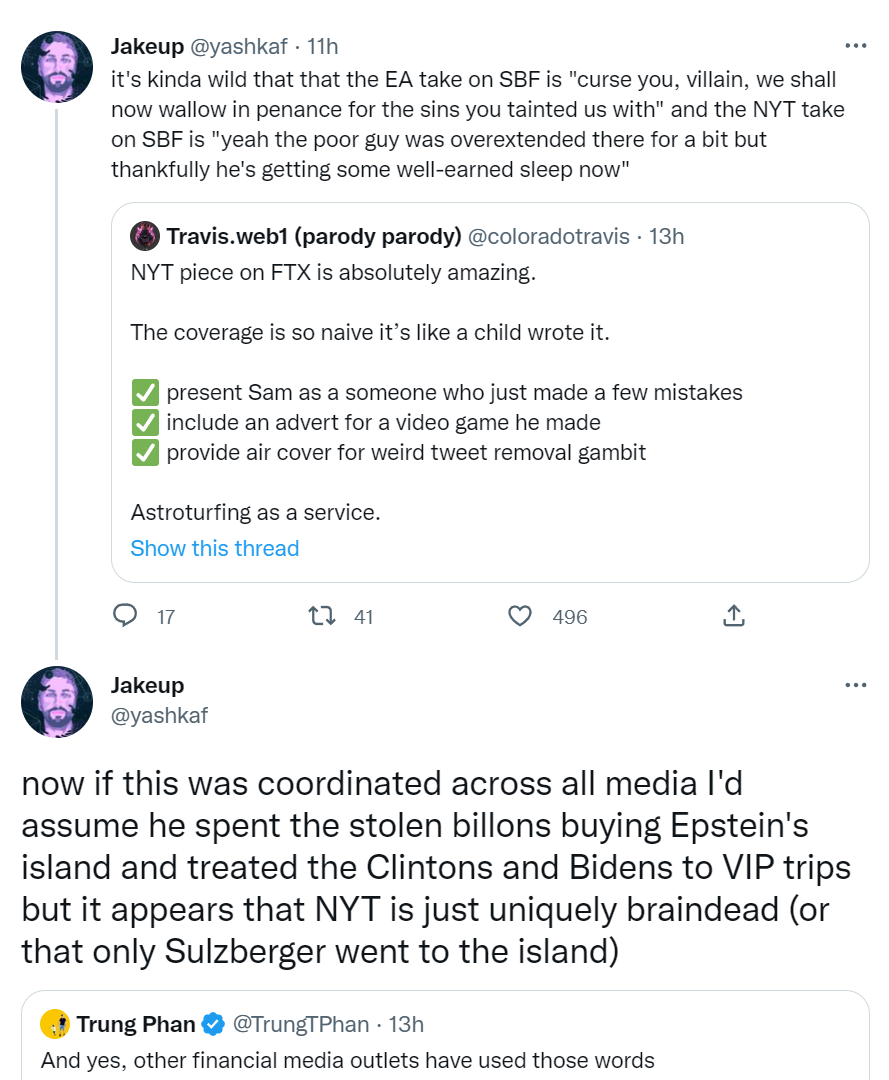

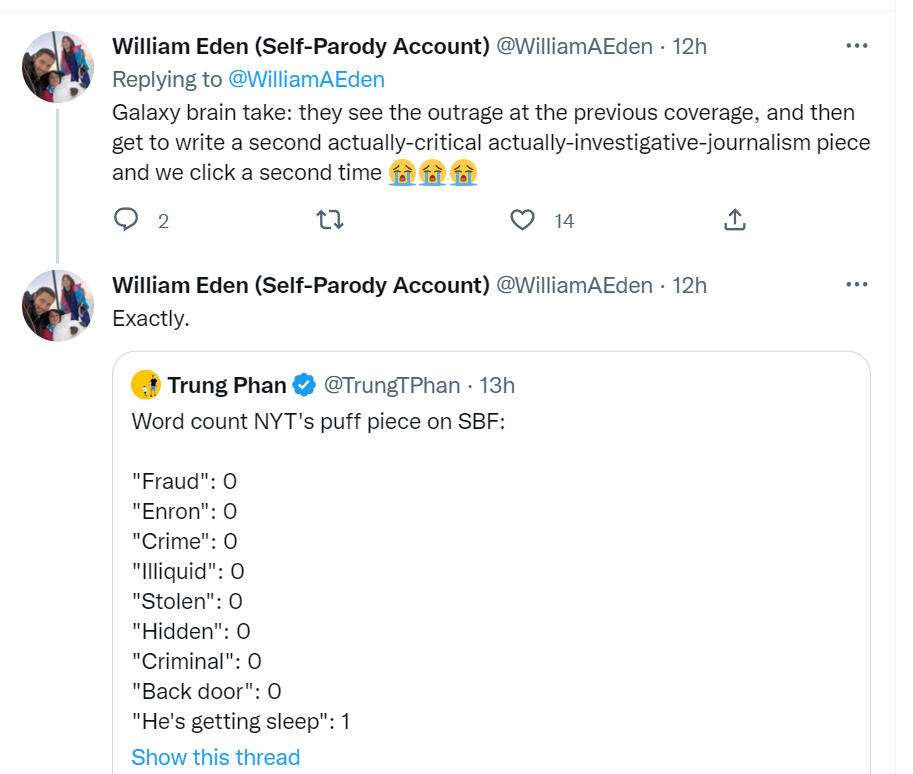

What The Hell, New York Times?

The New York Times landed an exclusive interview with SBF. They then used it to write what by most accounts, and my own reading, was an absurd puff piece. They then added a variety of other puff pieces.

NYT has spent years doing nothing but hitting the tech industry every chance they got to build a narrative that Tech Bad. Now, suddenly, there is a huge outright fraud and I mean, whose fault is that, really?

Have we considered that perhaps the ones who did the fraud are at fault? You’re blaming Binance for not buying FTX? Um, have you seen their ‘balance sheet’?

What? Seriously, what? You do know why he bailed out those firms right?

Contrast to this interesting thread from a New York Times reporter, where they did their usual thing and pressed SBF on regulations and location shopping and conflicts of interests and then wrote a hit piece. And then now turn around and say ‘of course all of this was predictable.’ That’s what NYT is usually doing.

Many have not taken kindly to the Times deciding to cover up this fraud.

Here’s Jacob noticing the different attitudes.

I can confirm that coverage everywhere else reads like you would expect it to. This is not some broad based liberal media conspiracy. It is specifically NYT, which in turn allows them to be cited in places like Wikipedia.

Even for NYT, this is really something, notes Will.

Or Patri Friedman, who notes SBF’s Democratic political contributions.

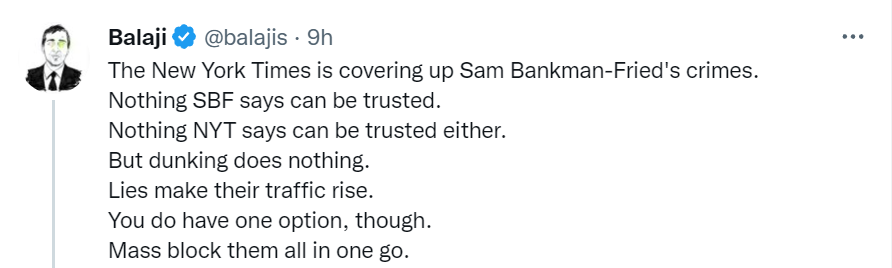

Here’s Balaji, although his attitude here is not new and even I think this is a bit much.

He doubles down here, generalizing beyond NYT, expecting media and politicians generally to downplay this and seek to protect SBF to protect themselves and the donations they got. Balaji recommends pursuing various legal strategies against the charities and political groups that got money.

Kelsey Piper offers the alternative perspective.

There certainly is the fact that someone in SBF’s position is completely insane to be talking to the press at all, no matter how friendly. This still does not read to me like a clever plan to give him rope.

Then there is this interview with the resident psychiatrist, another sympathetic piece.

Patrick McKenzie sees the hand of a very powerful PR firm for all the glowing covers, especially post-implosion. Makes sense, and scary to think it is this easy, although presumably not cheap.

The Wit and Wisdom of Sam Bankman-Fried

Tyler Cowen redux on his conversation with SBF, this is the whole transcript. Contra the comments, SBF seems like he was making great points in the quoted portion.

SBF’s 3.5 hour podcast with 80,000 hours. Once again this is not a man afraid of risk.

The famous Odd Lots episode where SBF describes The Box. If you haven’t listened to it, and you’re reading this far, treat yourself to at least the transcript. It’s better in audio, perfect, no notes.

Old two minute clip on how crypto exchanges have to manage risk.

TV interview on SBF’s political operation.

The Wit and Wisdom of Caroline Ellison

Caroline Ellison was the CEO of Alameda Research, and has admitted knowing that SBF stole customer funds to give to Alameda.

She also wrote a bunch of very frank things on the internet.

One source described it as, ‘that feeling when Caroline is based as hell but also evil and steals your money.’

Here is Caroline on flipping coins for high stakes.

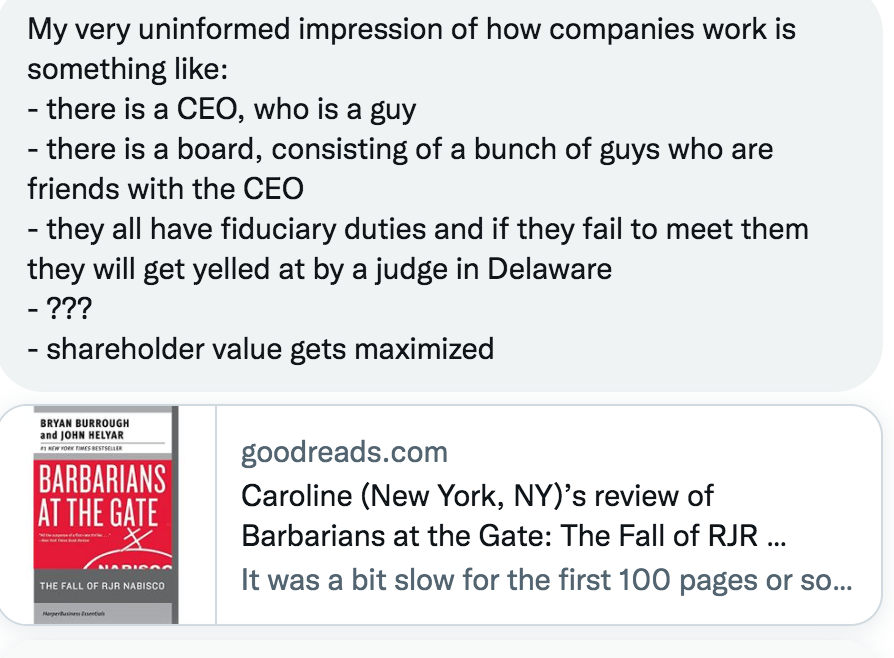

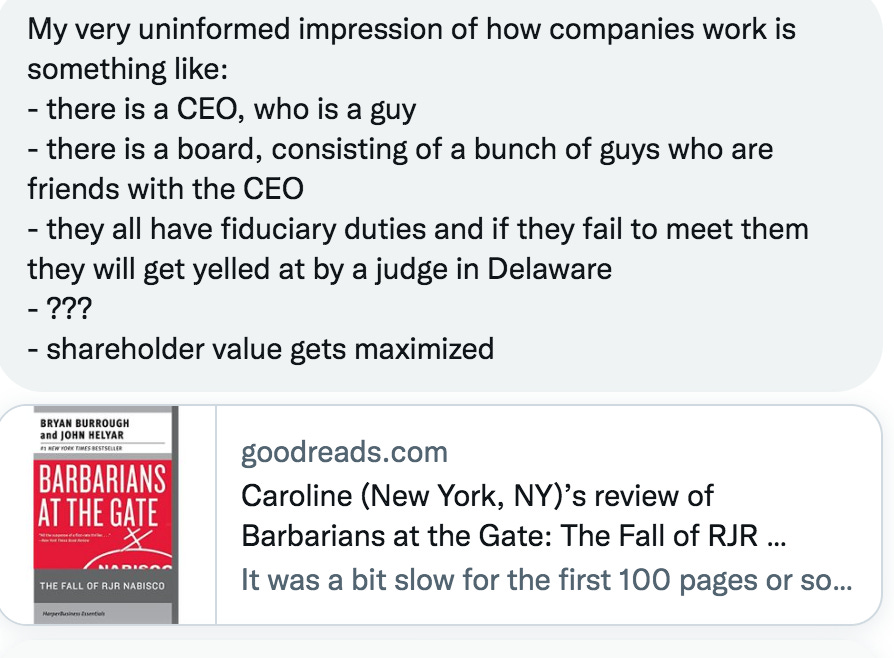

Caroline wrote a Goodreads review of Barbarians at the Gate (as opposed to SBF, who says he never reads books and Your Book Should Have Been a Blog Post). It said:

The source called it a good summary. I have not read the book but I think this is exactly wrong, in that what happens after the ??? step is that shareholder value is not maximized. The CEO and board do what is good for them, which may or may not involve shareholder value, and mostly the parasitic managerial class does its thing. The whole point of Barbarians at the Gate, as I understand it, is that the ‘barbarians’ notice that shareholder value is not being maximized and thus propose to buy the company.

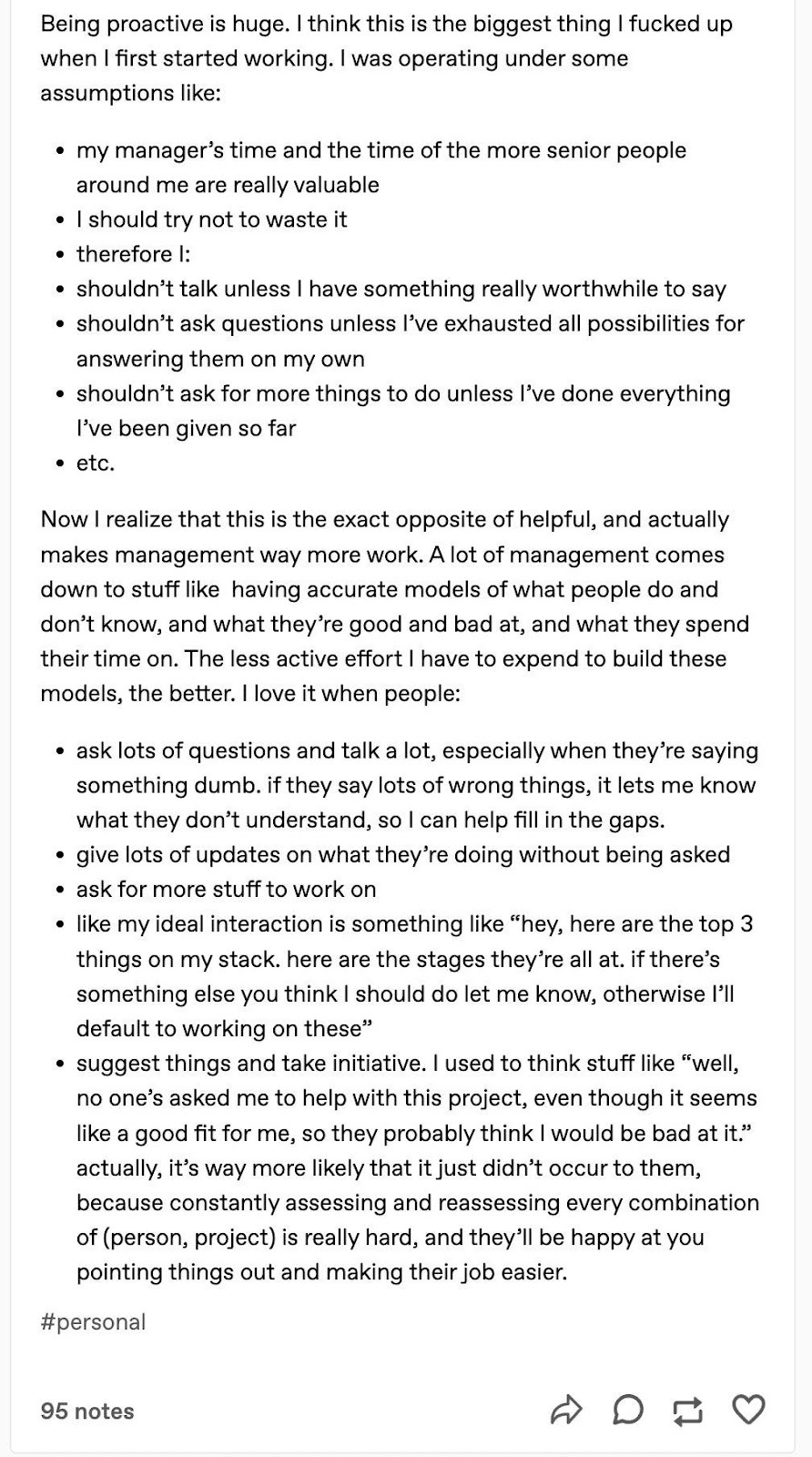

Here she offers career advice.

Mostly this is great. The interesting question is working hours. There are many jobs where there are highly diminishing returns to directly working more hours, especially doing so over long periods. There still is a real sense in which being ‘all-in’ on work really does make a super-linear difference in many jobs, whether or not that takes the form of super long hours that look like work. In the jobs where I consider myself to have been the most successful, other than writing, I was able to work basically all the time, and I think this made a huge difference.

Here’s Your Mistake Right There

To be safe, once again: Nothing anywhere in this post is investment advice.

(Section summary: Don’t commit fraud or steal customer deposits, get your share of the company properly papered, don’t take loans against tokens printable at will, don’t mark such tokens to market, don’t borrow short and lend long without being a real bank and definitely not against your own tokens, don’t go permanently super long your sector with leverage, don’t give your chief enemy and rival the exact ammunition to destroy you (via CZ’s FTT tokens), and do not talk to the press and confess crimes).

The biggest mistake was, obviously, ‘don’t commit fraud, don’t steal customer deposits, don’t be super shady in general and lie your ass off including to Congress and all that.’ The ends do not justify the means even when the ends are excellent. Even if they did initially, when you start to think the ends justify the means, the means change your ends.

This section sets that all aside. Ignore ethics and assume linear utility of capital. What if the ends did justify the means (which, again, they didn’t and don’t.)

The whole thing is still a murderer’s row of incredibly stupid mistakes.

First, in case anyone needs to hear this, get your share of the enterprise papered. Do not, I repeat do not, allow someone else to own the company outright. Do not do a ‘handshake deal’ for your royalties. Under business norms this is essentially telling them to screw you.

Second, how they did the accounting for ‘Sam coins’ like Serum, in addition to FTT. The ‘market’ value of their entire stash, which they could mostly print at will, was counted on their balance sheets. This is not how you do accounting, because this is not relevant accounting.

So what is the purpose of such an accounting or balance sheet?

If the purpose is to give you or anyone else an accurate indication of your assets, liabilities, value and future prospects, this is obvious nonsense. You are treating the balance sheet as some sort of mystical object that you placate with meaningless large numbers. To say ‘we are solvent,’ which SBF was still doing on 11/15, fools no one.

Unless it does? Presumably this is the purpose. Fraud. Who are you fooling? If the answer is ‘investors’ or anyone else who gets to see the sheet, it is a pure ‘flash your fake badge and hope they don’t look at it’ level con. If Sequoia Capital (or Tom Brady) fell for that, I am Jack’s utter lack of sympathy. If you don’t show the sheet, it’s lying about net worth with extra steps.

My presumption is that the primary goal is to borrow against the assets. This is something they did. It is deeply stupid on behalf of the lenders. Anyone actually thinking about the situation would understand that their capital is no good. If they try to liquidate it, they will not get very much even in ordinary times, and death spirals are likely. You are lending money against an asset someone can print at will and for which there is very little demand. This is crazy.

If you are Alameda, and a lender is stupid enough to give you that loan, do you take it? If your funds are all super liquid, and the interest rate is low, then I can see it.

That was not what happened. Alameda took out these and other loans, loans that could be recalled, and made long bets like venture investments.

Seriously. What. The Hell. You cannot borrow short and invest long like that if there is the risk that the loans can be recalled or not renewed, even setting death spirals and the black magic of borrowing against your own stock aside. If things in general are going badly, you are going to die to this. What are you getting in return that justifies that? Even if utility of money is linear it makes no sense.

The value of liquid capital to a firm like Alameda is super high, even setting aside the risk you run out and die, or your loans are recalled. Locking capital up for years makes no sense. Making such investments that are effectively long crypto, or long things correlated with crypto or both, makes even less sense.

That is a big danger for everyone in the crypto space. If you are in the crypto space, you are synthetically very long crypto. All your opportunities scale with price. Enterprise value scales with price. Ability to raise or borrow capital scales with price. The list goes on. Even if you don’t directly profit when the price doubles, you are very long.

When you invest in other crypto projects like this you are getting even longer than that. When you do that by borrowing against crypto collateral you are getting longer still. Meanwhile, Alameda was taking explicit naked long positions in coins for extended periods. They were flat out super long, all over the place.

If this was an explicit bet that we would never again see BTC $30k on pain of death, because most potential utility of a crypto firm is in worlds like that, then… I mean, I kind of get that thinking once you add in all the other crazy thinking, yet no. There was no need to take this risk. It did not buy anything worthwhile.

All Alameda seems to have been, after a while, is a levered bet on crypto, full stop, with a lot of leaks in it and an inability to survive downturns. Why?

Then there was the decision to shift from shady activity to outright fraud. Again, even setting aside the ethics, it seems highly unlikely that this was ever going to end well.

Even if it could have ended well, you know what one really shouldn’t be doing while doing that? Yes, the Michael Lewis thing too, but the thing where you take someone who has the power to take you down (CZ) and get into political fights with him.

The biggest WTF moment for me - I realize there are a lot of good ones and Matt Levine has his own favorites - is letting CZ/Binance get $500mm in FTT. Intentionally handing it to him. I don’t care how badly you want him formally off the cap table, either pay cash or do not do this, this is insane. You are handing your enemy the power to destroy you.

Oh, also, probably not a good idea to go around confessing crimes to the press.

Ethical Lessons Learned That Generalize Beyond Trading and EA

Before we start, in case anyone thinks ‘SBF was right except he got caught’ is a strawman position: Here is an in-the-wild example of the other perspective: philosopher at Rutgers University biting the bullet and saying the only thing SBF did wrong was get caught, ends do justify means, and all this talk of fraud being wrong is ‘just PR.’ They aren’t ‘really reckoning’ with the questions here. Whereas SBF? He’s doing ‘serious philosophy.’

People wonder why ‘serious philosophy’ is not taken so seriously these days.

There is also this, Rob Bensinger got less alarming but still worrisome results.

Eliezer Yudkowsky has a thread pointing out three key lessons from all this.

Those three lessons, which I endorse, are:

Do not violate deontology for utilitarian ends. Seriously. Stop. Don’t do it.

Get the cash in your damn bank account. Up front. Now.

We live in a universe beyond the reach of God, where bad things happen to good people, and where good things will get yanked away from you without notice.

I do think that there were good reasons for the ethical, non-fraudulent version of FTX to not set the money aside in advance. When you run a business that has large enterprise value and is vulnerable to crises of confidence, having marginal dollars available in an emergency can be super valuable, even if all you do is point to it so people know you have it. If people had thought FTX was solvent, it would have been, and the opportunity cost of capital in crypto is sometimes stunningly high. All of that would apply even if FTX was being fully responsible, and it goes double given all the fraud and dark magic FTX was using.

I would also disagree with Eliezer’s statement that you should expect the universe to surprise you on the upside as often as the downside. You should in expectation be surprised in a neutral direction. However, their distributions are different. If from an outside perspective FTX has a 5% chance of blowing up per year, then each day you wake up to the good news that FTX has not blown up, so mostly the news will be good if you are counting that as news. Whereas if one would mostly say that ‘man does not bite dog today’ is not news, then the news about FTX blowing up is only ever going to be bad until the situation is already quite bad.

Our world is not antifragile. Mostly disorder and unexpected things are bad news, so most updates above the standard update threshold are bad news. Note the same thing in AI, where the good news is of the form ‘we did not make any major visible progress towards ending the world today’ and the bad news is of the form ‘we did make such progress, look at this new result.’ So every time we get surprising news things seem like they are going worse than expected, which locally they are. Things do also seem to in general be going worse than expected on that front, but it does not obviously follow. We see a similar thing with Musk and Twitter, where the hunt is on for Bad News on a fractal level, so we should expect the news reports to be Bad News even if things are going well.

With related reasoning, Gideon blames the intersection of California ideology and the boiler room, and he draws the obvious conclusions about the dangers of naïve utilitarian thinking to cause the inversion of morality where it is immoral not to make as much money as possible, and then you spend that money teaching others to do the same.

Rao points out in this thread that when you try to spend large amounts of money on anything, you inevitably have to do so through abstraction and bureaucracy, and anything done at scale (EA donations being only a special case of this issue) will thus tend to be all screwed up. I do find his ‘the biggest thing you actually buy is a car’ attitude odd given the existence of houses.

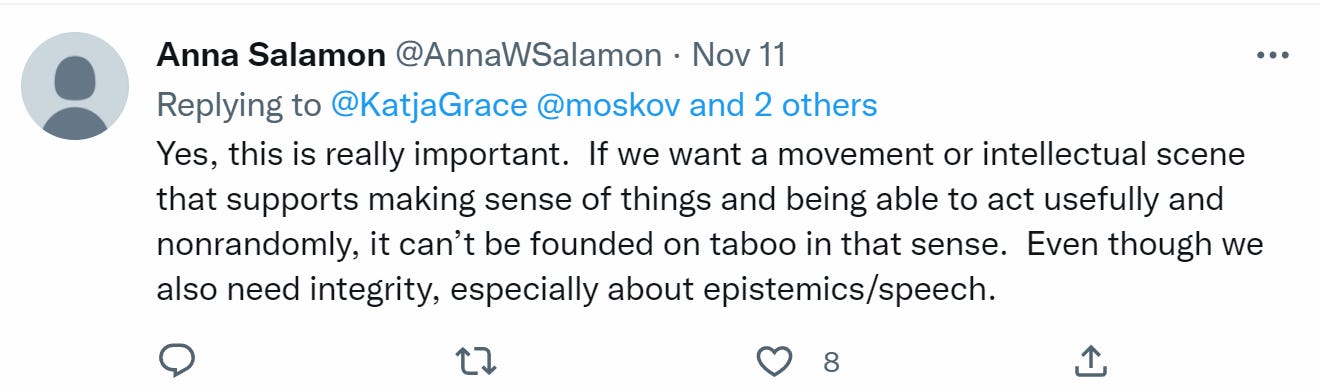

Anna points out that this kind of disaster, where people who end up in trusted positions with power and money then do unethical things and commit fraud, is rather common, including among nonprofits. As is the commercial source of your nonprofit's money turning out to have been fraud. There is a lot of fraud out there even if you don’t consider crypto. If we are so surprised, we thought that this group of people was so special, we should ask ourselves why.

This was in response to Jonathan Mannhart, who points out that the whole thing was a failure to realize what was happening but that this wasn’t a case of ‘a group collectively gave money and power to someone’ rather it was ‘someone went out and made a lot of money and then started handing it out.’ There was a failure not to recognize what was happening or was likely to happen next, on both an ethical and a practical level, which still indicates deep problems in the social dynamics and ethical systems involved.

What that does not obviously imply is a problem with risk management.

Then again, it kind of does suggest problems with risk management, in the sense that FTX failing was a risk and that risk was very much not being well managed. There was, as far as I can tell, no serious worry about the reputational fallout, nor was there any consideration of what would happen to the funding landscape and how to plan for the practical implications. That’s on top of the ethical failures.

Tail Risks and Existential Threats

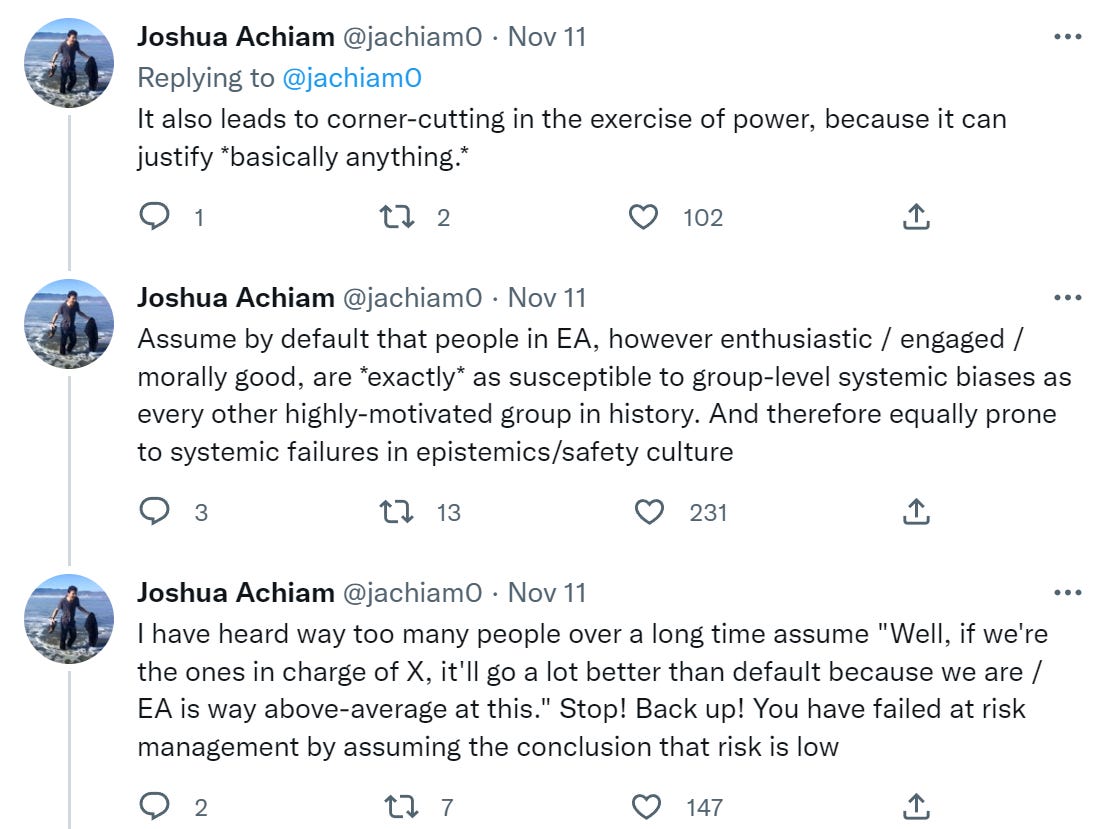

I will note that Joshua Achiam is at OpenAI, so him freaking out about tail risks seems like good news on principle. They could use more freaking out about tail risks.

What about Joshua Achiam’s thoughts on the implications for thinking about tail risks?

He also has thoughts about tail risks in his other thread I link to below.

(I will reiterate, in case it isn’t clear: No it is not reasonable at this point to think that this could possibly have not involved any fraud. If you explicitly claim the customer funds are there and they are not there, if you say you will keep the client funds there in your terms of service and you do not therein keep the client funds, if you offer loans against your own token, if your balance sheet is what we have seen, yeah, sorry, it’s overdetermined to be fraud, and it’s willful ignorance to not understand this.)

Side note: I do think that Joshua’s position on AGI risk, which is that ‘anyone who tells you probabilities are in the 5%-10% range or greater that AGI will immediately and intentionally kill everyone is absolutely not thinking clearly’ is very much him not thinking clearly, unless the ‘immediately’ he is saying here means, like, 2023, or ‘the first five seconds/minutes after you turn it on.’ The fact that he works on AGI at OpenAI and has this attitude should terrify you.

If this had indeed been a tail risk, a black swan, that was highly unlikely while also being preventable with better choices, what would I think of this argument? I would say that there is reason to worry, it should definitely be a negative update and need to be examined carefully. Also there would be big danger of some sort of large categorization error going on here, and problems like this are hard, that is the whole point.

This Was Not a Black Swan, We Could Have Seen This Coming

However, this was not a black swan and this was not a tail risk.

This was a white swan. It was a regular risk.

Certainly, from the FTX perspective, this was an ordinary, regular risk. If you know the kinds of things being done and the risks being taken at FTX and Alameda, under any possible interpretation at this point, you know there is the danger you will blow up if you miscalculate, especially if you get attacked and if people sell a lot of your token at once. Then you get into a political fight with someone who has $500mm of your token.

From the outside perspective?

There are at least two levels on which one could have seen this coming.

Alameda and FTX are taking crazy risks including being hugely synthetically long crypto, while borrowing short and investing long, so Alameda could easily blow up, and perhaps take FTX with it.

If it does blow up SBF will steal customer funds to try and prevent this.

Did we have enough information to conclude at least #1? Yes. We absolutely did.

Remember that SBF and Caroline were very public about being willing to take big risks, even at a planetary scale, and that he took expected value utilitarian thinking both seriously and literally. Very much an explicit bite the St. Petersburg paradox bullet when asked attitude. When someone like that blows up like this, is it ever really a tail risk? It is not even obviously a failure of risk management so much as a philosophical decision to not do risk management in a way we would consider proper.

This is thus very overdetermined to not be that surprising from the inside, it was a risk SBF and others chose to take on in order to, in their minds, increase expected value. I think that was both horrible ethics, and also horrible expected value calculation. What it wasn’t was a black swan.

We also know, because they explicitly told us, that they were taking large long positions in coins while also being synthetically long in other ways, much of which was illiquid. It does not take a genius to see this could blow up. From the outside, if you were paying attention, it seems fair to say you still had enough evidence to know this wasn’t a tail risk.

Most people got this wrong, some did not. That does not mean that most people in EA, or in crypto, or in general, did anything wrong in response to this level of risk. Most were not so exposed to FTX failing. Others were. I think it is fair to say that anyone who had reason to examine this, or did examine it, and did not see much risk, loses Bayes points and needs to reflect, myself and Patrick McKenzie included. I did not put the clues together.

The question is whether one should have seen the stealing of customer deposits coming, that the whole thing was pure fraud not simply ordinary crypto risk and fraud (which, again, is not a black swan when it blows up).

My mistake on this was two fold. One, I had far too low a prior on SBF stealing customer funds given what I knew (and given what I could have known). Two, I reacted to SBF claiming everything was fine as thinking that was a polarizing declaration. Once you say that, either everything is fine, customer assets are backed and this will all blow over. Or, things are very much not fine, and FTX and Alameda are pure frauds. Middle ground becomes extremely unlikely - as Patrick McKenzie said it is strange to do the thing you do when you are Very Not Fine in that spot, although he also did not sufficiently update at the time.

In that moment, I thought ‘surely this is not pure stealing of customer funds, SBF is neither that malicious nor that stupid, right?’ rather than updating properly that this was strong evidence of the stealing of customer funds. The moment the dam broke, and it was clear things were not fine, it was clear things were probably going to get worse, although things still got worse than I was expecting from there.

What about getting to #2 in advance? Can we add in, at the time, all the money being spent, all the strange requests and clauses, all the risk loving, all the shots being taken, all the illiquid investments and loans (which were largely public if you looked), all the predatory ‘Sam coins,’ all the complaints from former co-founders and everything else, and conclude that this house of cards is likely based on outright fraud?

I do not think one can be confident in this. I do think that if you were confident this was not true after an investigation, you were making a mistake.

Note that this applies differently to VC investment (either in FTX, or by FTX) versus professional traders on the exchange.

If you are a VC investor or taking VC money, the optimal amount of fraud, from your perspective, is not zero. You are more excited to invest if you suspect a fraud, those kinds of founders make good and make dreams real for you. So what if sometimes it all blows up? This is a game of hits for you, and you are much more worried about being asked why you didn’t invest in FTX than you should worry about people asking why you were. This goes double for crypto.

Notice this VC ready to invest in SBF again if he asked. Which, from a pure EV perspective, sure why not, same as they invested in Adam Neumann.

Therefore, I do not view ‘the VCs didn’t catch this’ as much of a justification. They are not supposed to catch it. It is not their job to catch it. I mean, they are supposed to do some things to catch this level of fraud, demanding voting shares and a company board in which they have a seat and doing proper audits, but they got none of that, because he needed to not allow it and the pitch was so good otherwise they went along (or, they took this to mean ‘this is a fraud’ and invested anyway thinking they were not the sucker, also plausible). SBF said ‘you can’t check for fraud, invest or don’t’ then they are doing what they do, as much as we might hate that. Better to make that common knowledge.

The institutional traders are different. They face a different risk profile. If the exchange blows up in 10% of years that is a real drag on returns, whereas a VC expects 80% or more of their investments to go to zero, fraud or otherwise. Why did they trade?

Some of them Did Not Do the Research, no doubt. Others likely decided it was worth the risk. If FTX is an easy place to make money, because trading is very good against Alameda and generally they treat customers great, and they pay interest on USD and BTC, it is not difficult to imagine a decision that the blowup risk is worth taking, at least for some portion of one’s bankroll. Or one can say that if FTX goes down everything is terrible anyway, it’s already systemic risk, so assume it won’t fail.

Another play is to hedge the risk with a short position elsewhere, and put your leveraged longs at FTX since if FTX goes broke you would have gotten liquidated at Binance anyway.

We do not know how much FTX risk reduced deposits (or depressed the value of crypto, see the last section) before the blowup. I can’t blame retail, in some sense, for falling for all the retail advertising, and the choice to do that suggests potential comparative advantage there.

I also simply don’t buy the ‘if the smart people didn’t see it you get off the hook for not seeing it’ argument. I mean, sure, somewhat, it's a partial excuse, but it is very much not a full excuse. People are blind, especially when it suits their outlook and ability to pitch their business.

Back to the main thread of logic here.

If you thought from the outside this was a tail risk, then I think very few people on the outside handled it so badly. It doesn’t much change what you should do unless you are reasonably central or dependent. What are you going to do, buy credit default swaps on FTX as insurance? The reason why this was handled badly is that it wasn’t a tail risk or a black swan.

Except, when we say ‘handle tail risks’ with respect to AGI or pandemics?

Those are also not tail risks! Those are risks! Yes, they are tail risks on any given day, or week, or month, or maybe year or even decade. Over the long term, no. They are probably inevitable things we must deal with. We have model uncertainty, so perhaps not, but the chance of facing another pandemic within 100 years seems much higher than 50% (assuming otherwise normal conditions). The chance of facing an unaligned AGI within 100 years, or 50 years, or 20 years, is a matter of much debate, yet if you think the chances are all so low that they count as tail risks then I am confident you are being stupid about this.

The Future of Effective Altruist Ethics

SBF admitted in his interview with Kelsey Piper that a lot of his talk about ethics was fake. I interpret his claim there as continuing to double down on naive utilitarianism, while saying all his talk about other considerations was fake. Maybe that too was fake. Maybe it wasn’t. Either way, where do we go from here?

Reminder.

If you need a refresher, remember the ethics sequence.

Another reminder.

Dustin Muskovitz reflects, as does Rob Wilbin who is extremely angry.

Dustin also gives the excellent advice ‘don’t make leveraged bets on coins you can’t afford to lose. I would include in that any crypto purchases whatsoever. Understand that they very much can go to zero.

There is also this thread which seems worth considering.

Main thread then gets into more of the standard deontological stuff.

In addition to his thoughts on tail risk, Achiam has more EA-related thoughts.

Yes. This.

Well. Not quite this. You do not have to ignore the internal characteristics of the group entirely and revert to looking purely at base rates. There is some evidence that one can draw upon beyond that. Still, one must be very cautious, the default is to fool one’s self about such things. The order of magnitude needs to be reduced, at a minimum. In some circumstances, the sign of such updates is non-obvious.

The thread then talks about tail risks and AGI as I discuss above, where I disagree with it a lot, and then suggests listening to normies more - they are aware crypto is a hive of scum and villainy and are not suddenly acting surprised here.

While I do think many in the EA space do need a healthy dose of normie, I do not think that is an appropriate lesson here. Yes, normies know crypto is full of scams. It seems unfair to think that EAs did not know this until last Tuesday. The attitude was more ‘this is full of scams and it is worth it anyway’ and also ‘our guy is Definitely Not a Scam, No Way.’ The focus should be on those two statements, especially the second.

Tyler Cowen predicts it is not dead, but that he does anticipate a boring short-run trend where most of the EA people scurry to signal their personal association with virtue ethics. To which I say, even if boring that would be good because I am a long time supporter of virtue ethics, especially for EAs, although I chickened out and never figured out how to write “Can I Interest You In Some Virtue Ethics?” from my old to do list. Alas, I am confident Tyler is incorrect, and instead EAs are scurrying to signal their personal association with deontology instead.

It is worth pointing out, as Chris Freiman does here, that anyone criticizing those who took money from SBF has to include his very large donations to the Democratic Party (and also, although this will likely be forgotten, big donations from another FTX executive to Republicans as well, although smaller in scope.)

Deep, fundamental flaws have been revealed in the EA ecosystem. FTX was in large part throwing funds at anything that had sufficiently good EA branding, and little else. The flip side of ‘EA’s cause areas and problems are everyone’s cause areas and problems’ is to not assume all good must be done inside the self-dealing ingroup, and making decisions based on EA’s reputation does not lead down good paths. This is an excellent time to halt and catch fire, to take stock, to ask what other types of fraud or fooling ourselves were taking place. Current honesty norms are, according to Habryka and other private sources, degrading over time. There is a chance for EA to emerge from this as a much better, if for now less well-funded and less-liked, movement - if people take that opportunity.

Reporting Live From the EA Forum: Highlights

I pulled 20 posts from the EA Forum about FTX. Consider this an index.

FTX FAQ, focused on the concerns of EAs. Duplicative of other info.

The FTX Future Fund team has resigned. Any funds not already sent are unlikely to be sent.

Important from the comments there about What Happened will be quoted, verifying claims elsewhere, then we are on to the question of potential clawbacks.

(This below is Eliezer in reply to Kerry above)

Highlighting: and more broadly I have been complaining about an erosion of honesty norms among EA leadership to many of the current leadership.

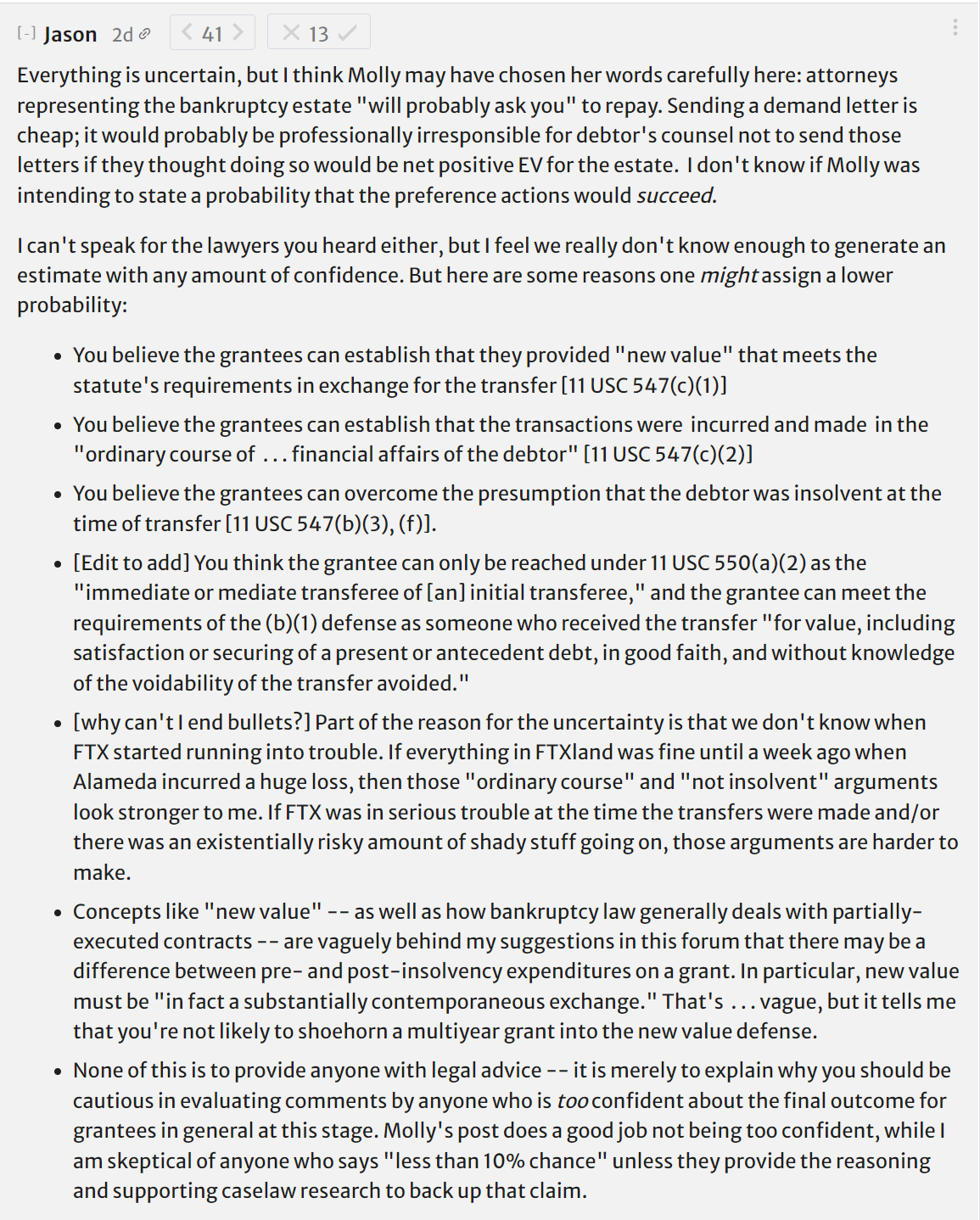

Legal guide to the possibility of clawbacks of funds given by FTX.

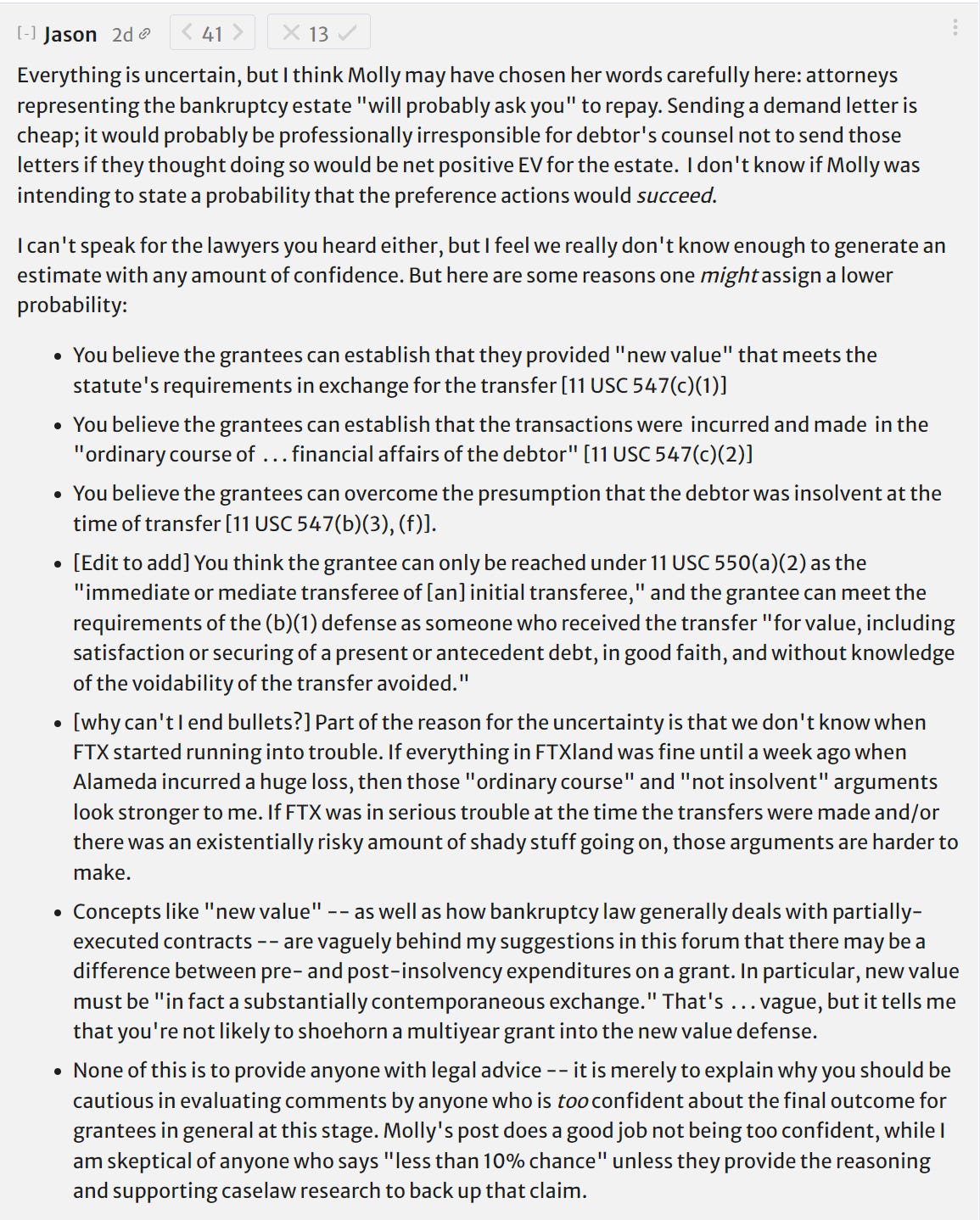

There are two main types of clawback processes. The first and most common (called a “preference claim”) target transactions that happened in the 90 days prior to the bankruptcy filing. Essentially, if you received money from an FTX entity in the debtor group anytime on or after approximately August 11, 2022, the bankruptcy process will probably ask you, at some point, to pay all or part of that money back.

The second clawback process (called a “fraudulent conveyance claim”) targets transactions that happened up to two years prior to the bankruptcy filing. The root of these claims is an allegation that the debtor moved assets out of their organization for the purpose of frustrating future creditor claims. These types of claims are more complicated to prove, less commonly brought, and more individualized to the specific transaction.

It is way too early to tell whether and how fraudulent conveyance claims might be used in the FTX bankruptcy proceeding. But they would tend to target larger transactions or transfers that seem irregular, even if the recipient (e.g., grantees receiving funds) did nothing wrong and had no knowledge of any impropriety.

…

Timing: This will likely take months to unfold.

From the comments:

"probably" sounds like >50% probability. I talked to some lawyers and my (possibly incorrect) notes from that call say that preference claims are "very unlikely" to apply to Future Fund grantees (suggesting <10%). I don't know why they believe this; it's possible I misunderstood them; they also flagged that everything is very uncertain.

I interpret this as ‘they will probably ask you nicely to pay the money back. It is much less likely, but possible, that they will attempt to legally force you to pay the money back.’

If you need emergency funding in the EA space, Nonlinear says they will attempt to provide it.

Eliezer Yudkowsky advises not to injure yourself by returning FTX Future Fund money for services you already provided. I strongly endorse this. If you have not yet rendered the services it is trickier, yet I still would not return any funds unless, at a minimum, I was required by law to do that, or had good reason to know the money would go to reimburse victims rather than to insiders, lawyers and other crypto funds. Another note is that if you are not given a formal legal clawback, and you return the money, the legal process can force you to return the money a second time. So it is likely unwise to respond to any informal requests.

Also, in case it wasn’t obvious, if the rent is due, you can use that money to pay the rent or buy food, it does not put you in a better position to not do that. Even if the money is later clawed back, you are not making things worse on yourself here.

I do intend to donate or return, in some fashion, the $1,000 I won in the EA Criticism Contest, even if not legally required to do so, because I directly criticized a contest funded by FTX and did not point out any of the problems with FTX. So I do not deserve to have won a prize.

Eliezer also offers the opinion that the one to blame for FTX is... FTX, not anyone who had some sort of twisted moral impact on Caroline or SBF. Certainly the ones most to blame are the ones that did the thing. That does not let those who created the conditions for it to happen off the hook.

I also would point out that ‘heroes put the entire group, many innocent people, ‘the city,’ planet Earth or even the whole damn universe or multiverse in grave danger to save any main character because That’s What Heroes Do’ is ubiquitous in our fantasy media. Villains invoke it Because Decision Theory, they know it will work, and even without that it is rather mind-bogglingly awful. It might be a majority of DC comics plots. That kind of thinking needs to be widely condemned and fall in status at least via What The Hell Hero moments, and I worry it has more influence in these situations than we think.

Discussed above, ‘how could we have prevented this?’

The top-karma post of all time on EA Forum says: We must be very clear: fraud in the service of effective altruism is unacceptable. The top comment points out that CEA explicitly condemns fraud. I very much wish such statements would recognize there is nothing special about EA here, and simply say here (for example) ‘fraud is always unacceptable, period.’ Yes, it is good to see everyone condemn fraud, even after it is uncovered. It is still one hell of a low bar. Most fraudulent organizations take a formal anti-fraud stand (if formal enough to have such stands at all) and few if any take the opposite position - I am curious about certain weird cases like the Communist Party, which seems to take a clear pro-ends-means position. Which is a hint. There are also a handful of people who endorse fraud when asked, one of whom arguably was recently president. It makes him smart. This position is still quite rare.

Will MacAskill offers a personal statement on FTX, a repost of his Twitter thread, which can be summarized as ‘I have said over and over that you can’t use means-ends reasoning and no one should commit fraud, I am shocked shocked to find it going on in this establishment and condemn it in the strongest possible terms.’

But if there was deception and misuse of funds, I am outraged, and I don’t know which emotion is stronger: my utter rage at Sam (and others?) for causing such harm to so many people, or my sadness and self-hatred for falling for this deception.

I want to make it utterly clear: if those involved deceived others and engaged in fraud (whether illegal or not) that may cost many thousands of people their savings, they entirely abandoned the principles of the effective altruism community.

I believe that Will needs to ask not only how he fell for this fraud. He also needs to ask how his influence and teachings, and his personal sponsorship and advocacy for SBF, did not prevent, or even helped cause, the events in question. It does not matter what one explicitly writes in books if people end up taking away the opposite message when the chips are down..

It is very reasonable to take time to reflect here, as Will says he is doing. I await the results of that reflection, and would be happy to assist if he so wishes.

Holden Karnofsky offers his thoughts, currently with 666 karma. He is of course outraged at all the fraud. He is also warning that OpenPhil is now likely to have a wider range of funding opportunities, and thus the bar for getting funding from them will be higher rather than lower. Holden is not committing to adjusting the OP portfolio towards long termism.

A post suggesting people are drawing the wrong lessons from the FTX fiasco, in particular these mistakes:

Ambition was a mistake, abandon AGI risk and buy bednets.

Earning to give now icky, abandon.

We already knew EA was full of this sort of thing.

Most hot takes on ethics.

I agree that the FTX fiasco should not much alter one’s cause priorities, except insofar as you were outsourcing your prioritization, in which case you should do less of that, especially if it was to FTX and also in general.

Earning to give is tricky. The need for it is now larger, and one could say that the ‘threshold of competence’ to expect chance of success is lower. However, the whole of earning to give’s results were previously mostly SBF and others at FTX, which no longer count in the win column. If they got there by fraud and insane risk taking, then lost it all, earning to give’s track record and prospects going forward look much worse, even if returns are higher. This is also a warning that if you are the type to try and make billions, you should worry that your ethics are vulnerable along the way. Most people who make it to billionaire do not keep the values and ethics they started with, and there are signs SBF was willing to cut ethical corners from the start.

Certainly, on a personal level, I have updated in favor of considering trying to make a lot of money, especially if it turns out that non-profit funding is sufficiently scarce that it does not make sense for me to be raising it for Balsa. If one must fail, fail fast.

The FTX crisis highlights a deeper cultural problem within EA- we don’t sufficiently value good governance. Post points to a series of examples of places where lack of good governance arguably did substantial harm. This is a strange time to respond with ‘the optimal amount of fraud is not zero’ or extend that to mismanagement, yet it would be wrong not to point this out.

I gave my take on seeing this coming earlier, and there is some additional evidence from the comment sections of these posts.

As for hot takes on ethics, no, of course events are evidence of the truth of philosophical positions, everything is evidence and all that. This is indeed rather strong evidence that something is deeply wrong with utilitarianism in practice. That said, my ethical position was already very different and has mostly not changed.

It is also worth pointing out that turning organizations into bureaucracies that ‘follow best practices’ is a good way to ensure nothing worthwhile is funded and lots of funds are misappropriated while also ensuring no one involved gets blamed for that result. There are twin failure modes, ‘do everything based on informal power dynamics and inner rings’ and ‘do everything with the proper meetings and paperwork attached.’ We have FTX as the move-fast-and-break-things position and OP as the institutionalists. I hope that EA does not double down on institutionalism.

SBF, extreme risk-taking, expected value, and effective altruism, detailing the evidence for SBF’s extreme risk tolerance.

Proposals for reform should come with detailed stories, which points out that many suggestions for what ‘should have’ been done would not have been actionable or would not have given reasonable hope of a better expected outcome. Seems right. There certainly is a class of ‘procedure that might have noticed the FTX situation in some form’ that should be given more detail and looked at carefully. I do think, as noted above, there was enough information for at least a lot of it.

An important question is what happens with the $500mm that SBF put into Anthropic. A bad actor could easily end up with those shares. It is also possible, although unlikely, that there could be an attempt at a clawback via fraudulent conveyance, which I doubt would work.

Discussion of the NYT article about FTX implosion’s impact on EA, low value.

A simple call to focus on ourselves rather than throwing stones. Good advice on the margin for most, still very possible to take this too far.

Post asks what to do if contacted by a journalist? Eliezer advises, and I agree, mostly do not talk to them unless you have knowledge that they in particular have been accurate and fair in the past. At most, offer to speak on background.

This call to wait for more information seems wrong to me. We know enough to react.

This older post is now obsolete, except as an example of what people thought at the time.

The Future of Crypto

Where does crypto go from here?

It doesn’t look good.

She links to Christopher Perkins, who was on the Lehman trading floor that day and sees a lot of parallels to the FTX situation.

Nothing anywhere in this post is investment advice, of course, and all that.

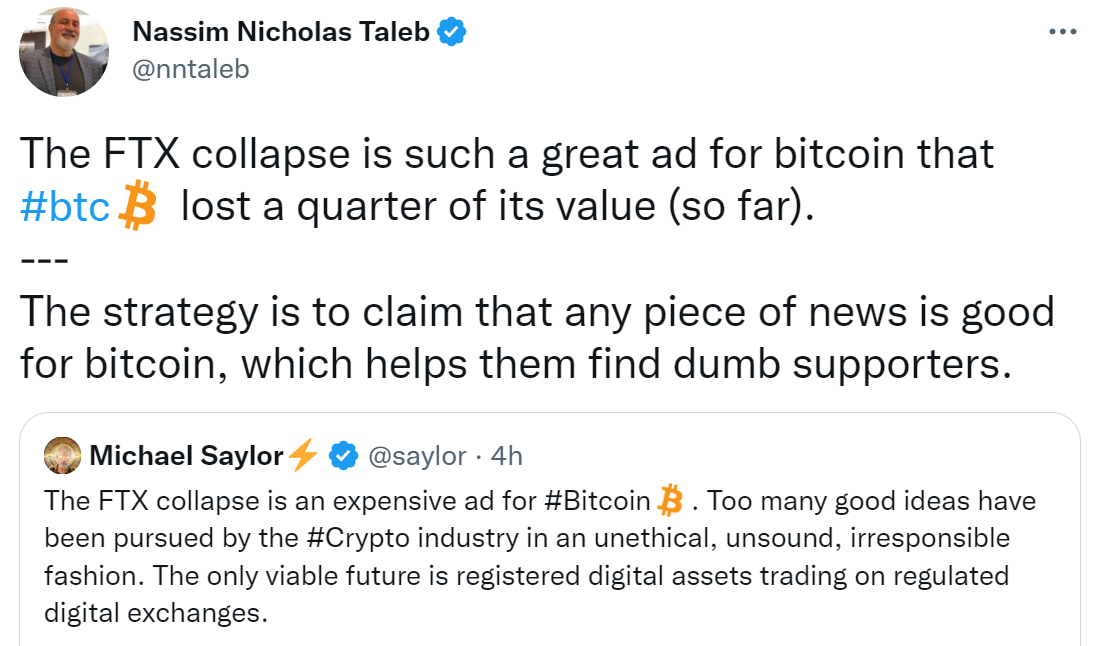

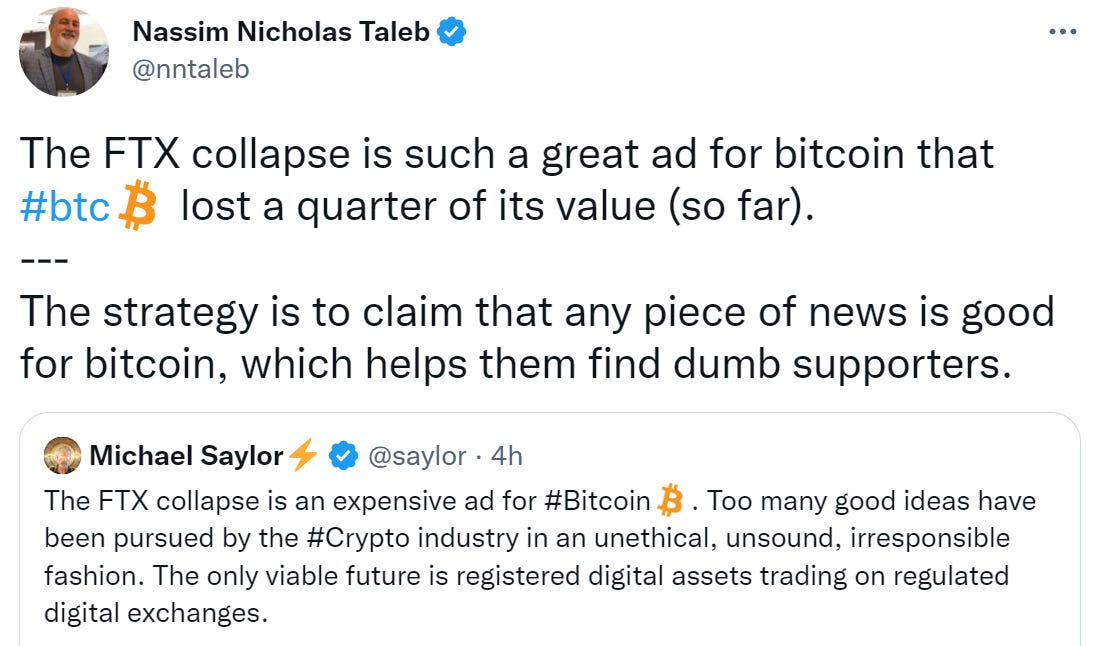

As always, some people will say anything is Good For Bitcoin. Except, no.

Alex Tabarrok worries this could lead to Central Bank Digital Currencies (CBDCs) and financial totalitarianism. Certainly the chances of that future went up a bit.

What contagion has happened so far that we know about?

Crypto lender SALT pauses withdraws. Genesis’ crypto-lending unit iss halting customer withdraws, endangering Gemini Earn.

As always, People Are Calling Tether a Fraud, the peg has been shaky at times. An additional hypothesis is that Tether was previously loaning funds to Alameda, explaining their super sketchy commercial paper holdings, but critics forced them to clean up their act in time.

Patrick McKenzie warns of widespread contagion, citing Ikigai Capital as an example.

The one place I have heard multiple warnings about is Crypto.com, this is one of a few I saw, there is also this claim that they directly lost over a billion in the FTX collapse.

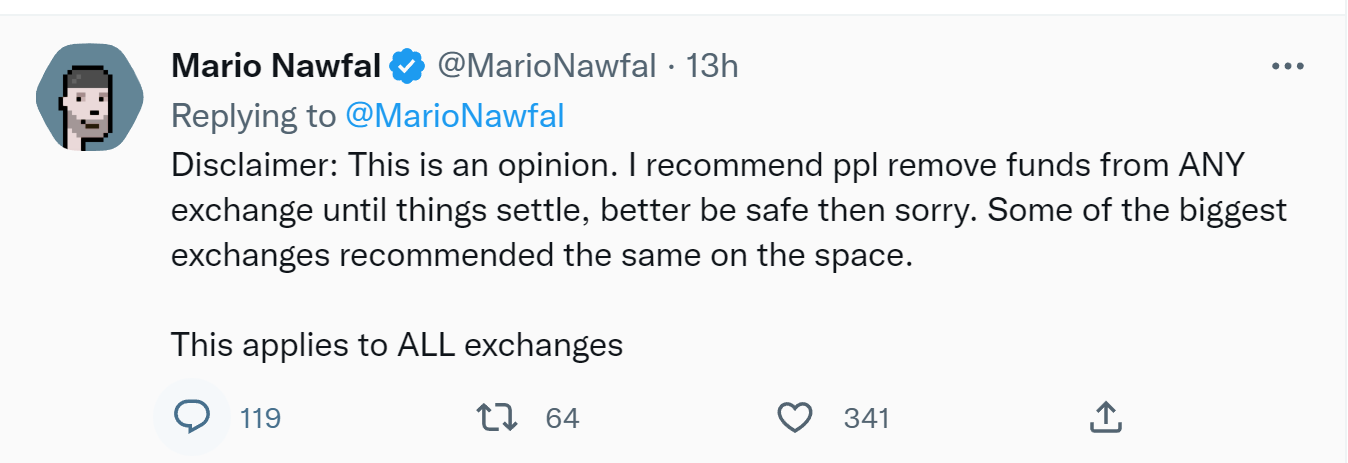

I am inclined to agree at least for any exchange that isn’t deeply regulated, and if it’s easy for you then definitely any exchange at all. If you are not actively trading, there is no reason to take on that tail risk. If you are actively trading, think about what scenarios mean you don’t get paid.

Are they all insolvent? Some people do suspect this. Does not mean they would collapse. I would be very surprised if Coinbase was insolvent. Gemini seems to have let customers loan out funds to get interest in ways that put them at risk due to Genesis.

I definitely do not think that was SBF’s plan. It would be a monumentally stupid plan if part of the plan was ‘remain solvent.’ Binance blowing up would have killed FTX dead given what SBF knew, along with everyone else it would kill dead, and the fraud all gets uncovered. So no. I still would be skeptical that many offshore exchanges could survive a run on the bank, and I would withdraw any funds at such places unless you are getting tons of value from it.

Milky Eggs here makes the doomer case that this is the beginning of the end. Not that crypto will entirely disappear, store of value still has some worth especially in failed states, but that there will not be a comeback this time. Similarly, Noah Smith asks, what if crypto just dies?

A question that must be asked.

I mean, it would take out a big chunk of EA because it would bring down all of crypto quite a lot. The failure of Tether would be a catastrophic event for crypto. ‘I do not hold any USDT’ is not a way to stay safe out there. If you have your USDT short on against a USDC long, or what not, I would be very very careful about exactly who or what protocol you think it paying you your winnings.

Binance is forming an Industry Recovery Fund.

In the short term, things look bleak to me - not as bleak as Milky makes them out to be, still rather bleak. Reputation is way down. Enthusiasm will be way down. Regulation and crackdown are coming. Ability to raise money will be way down. Bailouts will be much harder to come by. Contagion is likely.

Will Eden has a thought.

The decline in crypto prices of ~20% does indeed seem too low to me. The very good inflation number means this is more like a real ~25% decline, which still seems too low. It is crypto, so anything can happen at any time.

The trick: This says nothing about whether the pre-blowup price was accurate.

This brings us to the three hypotheses that make sense to me.

This somehow is not... that... bad? I mean, this does not really make sense to me. This seems really bad. Still 25% is a lot, and the decline in market value is 5x-10x the wipeout at FTX. Perhaps further contagion can be prevented and this move now makes sense.

Perhaps a lot of insiders already sold off or went short knowing this was coming (at least eventually),maybe some of them were super short, and it was priced in quite a bit. Given it didn’t have the BTC and other coins its customers thought they had, a lot of this selling was by FTX itself. That this would make FTX itself and its selling the cause of FTX’s loans being recalled, at the same time they were going long in ways that didn’t create market impact. Wow. Prices were already far down from their highs, so that would explain it. Then those insiders can cover the shorts or buy back in at a profit, taking the money from ‘weak hands’ in liquidations, same as it ever was. The cycle continues.

The other explanation is that insiders simply cannot allow prices to fall further.

Call that last one the Rubicon theory. What happened to FTX was at least partly contagion from Terra-Luna. There is already going to be a lot more contagion from FTX. How many more players become insolvent, how many more loans get liquidated, how many more cascading disasters happen if prices fall much further? Are any of the major players equipped to survive in that world?