One place where EAs paying taxes in the US can probably have differential impact is in making donations less than the standard deduction(s) they can take on their taxes such that they would not benefit from itemized deductions from donating to registered charities. Impact concerns aside, unless you're donating enough to exceed your standard deduction, you don't get much or any tax benefits from donating to registered charities, and so all of your donations will be post-tax anyway so you have a unique opportunity to give funds to EA-aligned causes that are otherwise neglected by larger donors because they can't get the tax benefits.

Some examples would include giving small (less than $10k USD) "angel" donations to not-yet-fully-established causes that are still organizing themselves and do not or will not ever have charitable tax status and participating in a donor lottery.

Plenty of caveats to this of course, like if you have employer matching that makes it worthwhile to give to registered charities even if you yourself won't reap any tax benefits, and state-level standard deductions are smaller than federal ones so it's often worth itemizing charitable giving on state returns even if it's not on federal returns.

TL;DR: Even though Facebook has only provided $7 million USD in matching funds, EAs have been able to get more than half their donations matched in the last two years and I don't expect the opportunity to become saturated (by EAs or the general public) this year either. That is, I expect EA donors who take an hour or two to prepare (by reading the EA Giving Tuesday team's instructions and making a few small practice donations) will still have a 30-70% probability of getting matched (up to $20,000 per donor) this Giving Tuesday, December 3, 2020. (E.g. I'm currently willing to make an unconditional bet at even odds that I will make a donation that is matched by Facebook for Giving Tuesday this year.)

Great idea, I didn't know that this opportunity existed!

For those like me who don't know what a 'standard deduction' is in the US tax system, here's a brief explanation:

Even if you have no other qualifying deductions or tax credits, the IRS lets you take the standard deduction on a no-questions-asked basis. The standard deduction reduces the amount of income you have to pay taxes on.

You can either take the standard deduction or itemize on your tax return — you can’t do both. Itemized deductions are basically expenses allowed by the IRS that can decrease your taxable income.

Taking the standard deduction means you can’t deduct home mortgage interest or take the many other popular tax deductions — medical expenses or charitable donations, for example.

In 2020 the standard deduction is $12,400 for single filers and married filers filing separately, $24,800 for married filers filing jointly and $18,650 for heads of household.

Readers might be interested in the EA Donation Swap system, which increases the overall tax-deductibility of EA donations, without people having to change the organisation they support.

An example of how it works: - Cara from Australia wants to the Good Food Institute (which is registered in Canada but not Australia) - Sam from Canada wants to donate to AMF (which is registered in both countries). Cara and Sam are matched through the EA Donation Swap website, and agree to swap donations, resulting in Sam donating to the Good Food Institute (and getting his tax-deduction), and Cara donating to AMF (and getting her tax-deduction).

We've also arranged swaps when one recipient organisation is NOT a registered charity in any country, and the swap results in one donor getting tax-deduction, which they wouldn't have done without the swap.

At the moment we are very constrained by Global Health and Poverty donors from countries with a lot of EA charities (UK, US, Canada) and countries with no EA charities - so if you are in this boat contact us! This constraint means we can't guarantee we'll be able to find you a matching donor.

Focusing on tax-deductibility too much can be a trap for everyday donors, including myself. I keep referring to this article to remind my peers or myself of that.

One piece of information is not mentioned: At least in some countries, donating to a not-tax-deductible charity may be subject to gift tax. I recommend that you check out if this applies to you before you donate . But even then the gift tax can be well worth paying.

A similar point to be made is that "Donating effectively does not necessarily imply making a donation with low or zero fees."

E.g. If you would donate $X to an organization if there were zero fees, the fact that there is actually a credit card fee of a few percent probably should not cause you to donate to a different organization entirely (or cause you to give substantially less for that matter).

That said, it does seem to me that once one had decided on an organization to give to, one should separately optimize how to make that donation (considering donation matching opportunities, whether the donation is or can be tax deductible (which may mean investigating whether a donation swap with another EA makes sense and whether practicing donation bunching makes sense), fees, etc.)

Yeah, both good points. To further complicate things, if you're concerned about the net costs of your donation (e.g. both the transaction fees, as well as the administrative costs involved) then sometimes paying the transaction fee means that it's actually cheaper overall to process the transaction. For example, the service paid for by the credit card fees on EA Funds (Stripe) allows us to automate almost all of the accounting, saving a huge amount of person-hours and keeping running costs lower. Obviously there's a break-even point, and for larger donations it definitely makes sense to seek to avoid percentage-based fees.

Some estimate of how effectively the government uses your paid taxes is an important part of this equation too right? I'm guessing it's not considered to be that close to 0? Anyone seen an attempt at any kind of estimate?

I think that for most donors this can be disregarded. Even if the marginal use of your additional tax dollars is still pretty good (e.g. 10% as valuable as your best charitable option), you're still better off donating to the charity. In extremis, it would imply that your best marginal donation option would be to voluntarily pay more tax, rather than donate.

While it seems in theory possible that the marginal dollar that your government spends is more effective than your best charitable donation option, I'd guess that in practice this is almost never the case, largely just because Your Dollar Goes Further Overseas, but also because your contribution to government revenue will be diffused between the many hundreds of programs that the government runs (some of which may be positive, like preventive health or basic research, others which may be pretty harmful, e.g. subsidies for industrial agriculture or maintaining nuclear arsenals).

Donating effectively does not necessarily imply donating tax-deductibly

[Disclosure: I help run EA Funds, a platform for making effective donations]

TL;DR: If you expect a non-tax-deductible donation opportunity to be ≥2x times more impactful than one that you could claim a tax deduction on, you should probably choose the higher-impact option and forego the tax deduction.

* * *

Claiming a tax deduction on your donations allows you to effectively increase your overall income, in the form of a tax return. This additional income can then potentially be also donated, increasing your overall impact[1].

Unfortunately, not all charities (or giving opportunities in general) are tax deductible.

Sometimes a charity doesn’t have a tax-deductible entity in your jurisdiction. For example, while Effective Altruism Australia (EAA) has done great work making a number of GiveWell top charities tax deductible in Australia, it is (to the best of my understanding) legally constrained from regranting to charities working in other cause areas, such as those promoting longtermist or EA meta work.

Additionally, many promising projects (even those based in the same country) aren’t conducted by registered charities at all, e.g. commissioning independent research, funding a new (i.e. as-yet-unregistered) high-impact charity, providing stipends to talented students, etc.

I’d guess that many donors’ first instinct is to look for tax-deductible giving opportunities. But I’d like to argue that donors may end up having more impact foregoing the tax deduction, and simply donating to the project that they believe to be most impactful, even if this means that their overall donation amount is smaller.

(For the purpose of this piece I’ll assume that the primary purpose of seeking a tax deduction is to increase your net income, or your net donations, and ignore other reasons for doing so.[2])

Let’s consider a hypothetical donor with a marginal tax rate (MTR) of 25%. In the donor’s country, Charity A is the most effective donation opportunity. However, there is another charity, Charity B, which operates in a different country, which the donor considers to be twice as effective as Charity A. Let’s baseline to Charity A, and say that they produce one unit of impact for every $100 they receive.

Scenario 1: the donor donates $100 to Charity A, and claims the tax deduction, which is worth $25. The donor has purchased one unit of impact, for a net cost of $75 [3].

Scenario 2: the donor donates $75 to Charity B. Ignoring transaction costs, foreign exchange rates etc., the donor has purchased 1.5 units of impact for the same net cost of $75.

Foregoing the tax deduction allows our hypothetical donor to have 50% more impact overall for the same net cost.

I believe this presents a compelling case that effective altruists should focus considerably more on the impact of their donation rather than the potential for tax deductibility as the key determinant of where they donate.

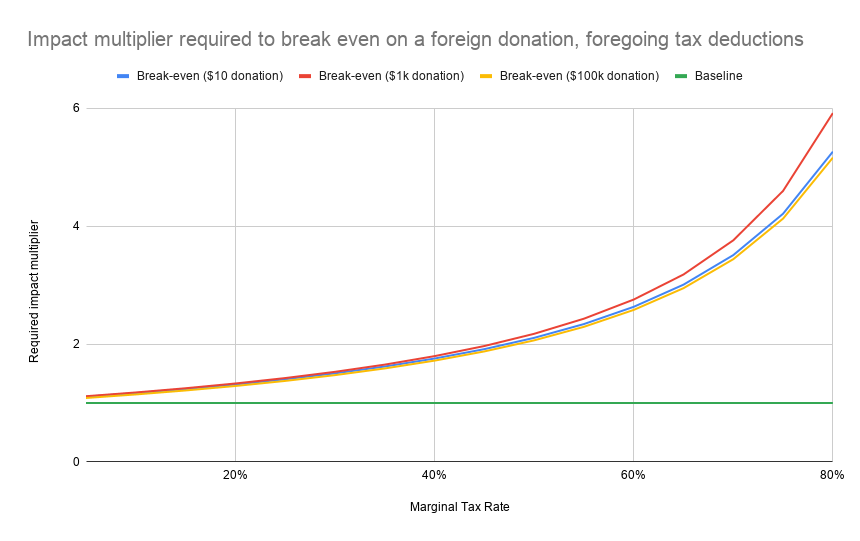

It’s not always easy to know (or even guess at) the relative impact of two different giving opportunities. However, it’s not necessary that you know the exact multiplier. All that matters is believing that the multiplier is sufficiently large. At normal tax rates [4], an estimated impact multiplier of between 1.1x and 2x (which seems very plausible) is sufficient to break even. Even assuming a very high theoretical MTR of 80% only requires a ~5x multiplier to break even. I’ve calculated the break-even points in the chart below, factoring in forex/transaction costs (source) [5].

Obviously, the ideal case is that we, as a community, expand tax deductibility for highly impactful projects to as wide a range of countries as possible. Unfortunately this is often fraught with legal complications. Most tax authorities (in my experience) don’t look particularly favourably on pure pass-through regranting, and setting up the required legal entities can be costly and time-consuming. Some countries’ tax codes only allow tax deductions for specific kinds of public benefit (e.g. education, poverty relief), which may preclude donations to e.g. longtermist or meta projects. While many in the community are working to solve this problem [6], it’s inevitable that there will still be gaps. And aside from these jurisdictional issues, there will always be the possibility that the highest-impact project on the margin isn’t even being run through a registered charity.

By thinking in this way, you expose yourself to a much broader scope of potential impact. You can find the best charity in the world that champions the cause you care about, instead of settling for a local alternative. You can support talented people in your community who have exciting, potentially world-changing ideas for projects, and help them get off the ground. So, consider just donating less (by the amount of your marginal tax rate) to the projects you believe will have the greatest impact, and don’t sweat the tax deductibility!

* * *

Footnotes

In the United Kingdom this process is effectively automated via the Gift Aid scheme, where instead of receiving a tax return, the charity instead claims the money directly.

E.g. donors using ‘tax deductibility’ as a proxy for ‘this organisation has been deemed legitimate by the government and probably passed an audit’; donors who are constrained to donating to tax deductible orgs because their funds are coming from a Donor Advised Fund or workplace giving scheme etc.

I’ve chosen to ignore the case where the donor reinvests the tax deduction as a donation, but the math works out the same. In Scenario 1, the donor purchases 1.25 units of impact for $100 net, in Scenario 2 the donor purchases 2 units of impact for $100 net.

This chart assumes a foreign exchange loss of 3% of donation value. On the $10 donation, it assumes a transaction cost of 2% (comparable to expected credit card processing fees), on the $1k and $100k donations it assumes a $25 transaction fee, which is typical of a bank wire transfer in the US (SEPA transaction costs would be much lower). In reality this could be smaller if you used a dedicated forex broker like TransferWise. It also assumes that there are no transaction costs for donating in-country, which may not be realistic.

Giving What We Can members take a pledge to donate a percentage of income. While this is generally taken to be pre-tax income (under the assumption that donations are tax-deductible), members who don’t expect to receive a tax deduction for their donations base their pledge on their post-tax income. If you’re planning to apply the above method to the majority of your donations, you can simply select “My donations are primarily not tax deductible” when reporting your income, which will then prompt you to enter your post-tax income.

This post presents the executive summary from Giving What We Can’s impact evaluation for 2025. At the end of this post we share links to more information, including the full report and...

I used AI to fix transcription errors, rerrarange the ideas, and suggest tweaks to the title and some sentences.

Three of the most exciting projects to come out of EA in recent years are, in a vague sense, CEA spinouts:

* Kairos is directly a spinout of CEA and now handles most support for university AI safety groups. Basically everyone I've found who knows them is really excited about what they do

* NEST is an opinionated ideas-fi...

One place where EAs paying taxes in the US can probably have differential impact is in making donations less than the standard deduction(s) they can take on their taxes such that they would not benefit from itemized deductions from donating to registered charities. Impact concerns aside, unless you're donating enough to exceed your standard deduction, you don't get much or any tax benefits from donating to registered charities, and so all of your donations will be post-tax anyway so you have a unique opportunity to give funds to EA-aligned causes that are otherwise neglected by larger donors because they can't get the tax benefits.

Some examples would include giving small (less than $10k USD) "angel" donations to not-yet-fully-established causes that are still organizing themselves and do not or will not ever have charitable tax status and participating in a donor lottery.

Plenty of caveats to this of course, like if you have employer matching that makes it worthwhile to give to registered charities even if you yourself won't reap any tax benefits, and state-level standard deductions are smaller than federal ones so it's often worth itemizing charitable giving on state returns even if it's not on federal returns.

Also worth mentioning: Whether you have employer matching or not, all US donors can take advantage of Facebook's Giving Tuesday donation match (see EAs Should Invest All Year, then Give only on Giving Tuesday and the EA Giving Tuesday website).

TL;DR: Even though Facebook has only provided $7 million USD in matching funds, EAs have been able to get more than half their donations matched in the last two years and I don't expect the opportunity to become saturated (by EAs or the general public) this year either. That is, I expect EA donors who take an hour or two to prepare (by reading the EA Giving Tuesday team's instructions and making a few small practice donations) will still have a 30-70% probability of getting matched (up to $20,000 per donor) this Giving Tuesday, December 3, 2020. (E.g. I'm currently willing to make an unconditional bet at even odds that I will make a donation that is matched by Facebook for Giving Tuesday this year.)

Great idea, I didn't know that this opportunity existed!

For those like me who don't know what a 'standard deduction' is in the US tax system, here's a brief explanation: