Comments

Worth mentioning that given EA is quite big at Oxford, an elite university, a lot of British EAs will probably fall in the 20% who are forecast to fully pay off their student loan.

Worth mentioning that given EA is quite big at Oxford, an elite university, a lot of British EAs will probably fall in the 20% who are forecast to fully pay off their student loan.

Sure, and if you are in a high-paying job you do have a decision about whether to make voluntary payments to clear the debt early, but you should consider whether you will be taking a career break (either by choice[1] or not[2]) or moving into a lower-paying job in the future.

MSE has some advice on whether and when to voluntarily overpay back your student loan.

You can also use PolicyEngine UK (my nonprofit's free, open source web app) to estimate your taxes and benefits given your income and household characteristics. It captures nuances like the Child Benefit High Income Tax Charge and phase-outs of Universal Credit and the Personal Allowance, and shows your total marginal tax rate considering these factors.

You can also design custom policy reforms, and PolicyEngine estimates the impact, both on the UK and your own household.

Hey Max, great website! I randomly came across it a few days ago (possibly via hackernews?), didn't know you hung out here!

The folks organising EAGx Cambridge might be interested in chatting to you, I can connect you with someone there if you're interested

Yeah both my cofounder Nikhil and I are longtime EAs :) We have a couple projects in the works on tying PolicyEngine to EA , which we'll probably launch in the next couple months.

Nikhil is actually in the UK as well (I'm in DC), so could you please connect him to the EAGx Cambridge folks? He's [email protected].

Distrust any attempt to get you to make a bank transfer, you have less recourse when it comes to reversing these compared to a card payment.

In my experience living in the UK (8 years), bank transfers are extremely commonly used by small and large companies alike, and even for interpersonal transactions (say, paying your half of the bill to an acquaintance who has picked up the bill at a restaurant that wouldn't split the check), just because of the convenience and speed of them. Every utility and rent bill I've ever gotten has included bank transfer details as a payment option, sometimes as the only payment option. It's true that there's usually no recourse to reversing such a transfer, so obviously you need to exercise reasonable caution, but "distrust any attempt to get you to make a bank transfer" seems a bit much.

Thanks that is a good point, I've adjusted the wording.

Agreed with the interpersonal transactions (in fact it's amazing being able to bank transfer your acquaintances instantly and for free!), and with rent, but I must say I don't see it offered that commonly with regular companies - do you have any examples?

With utilities there is the bank transfer option but one is better off trying to use direct debit for extra protection via the Direct Debit Guarantee

We've paid the contractors for our home renovations via bank transfer, I think it's pretty common in that industry.

I was thinking for example of my energy and water bills, which both list various ways that one can pay. Looking at my energy bill now, I see that bank transfer is listed as the first option, followed by debit/credit card (if one calls on the phone), cheque, and finally direct debit. I find bank transfer the easiest for usage-based utilities, as I prefer to pay exactly what I owe rather than make estimated monthly payments as I'd need to do with direct debit... I'm a little paranoid about whether I will be refunded in a timely manner for overpayments, or if I will be hit with late fees if the estimate is too low. I didn't actually realize about the extra protection afforded in the case of direct debits, though, thanks! Good to know.

My invoices for accountancy services also list bank transfer as an option, though they also allow other ways to pay... I agree it would be weird for a big company to have bank transfer as the only option. Private contractors (repairmen etc.) have sometimes just given me an invoice with their bank details only.

This is a great post, although I'd maybe question the promotion of MSE as the best resource for UK personal finance. The site has a policy of only promoting risk-free products and strategies, so it has an over-emphasis on (eg.) savings accounts over investment accounts even in situations where the latter would be more appropriate. The information it provides is largely accurate, and sometimes useful, but I wouldn't recommend adopting its overall approach to personal finance.

Outside of investments, their information is unbeatable IMO and is very wide ranging (eg: booking flights, loans, utility bills).

I've never seen them advise against investing but only that they don't provide investment advice.

I do agree that MSE leans towards risk-free products, but I totally appreciate that stance given that 34% of adults in the UK have £0-1000 in savings and 65% have less than 3 months worth of savings.

In terms of accuracy and usefulness, I don't know of any resource that is as good on say consumer rights, insurance, travel, loans, household bills, benefits and other day-to-day stuff.

So yes I agree that 100% adopting its approach is suboptimal but as a first pass I think the people would be much better off following MSE, and then deviating when they are in a position where they can afford to take risks.

One analogy I often use in situations like this is someone asking whether the Earth is round. My answer would be initially yes, just to make sure that we are on the same page about the Earth not being flat, and only then could we get into the fact that it is technically an ellipsoid.

Sure, I understand why it takes that stance, but I’d still suggest (eg.) the resources on r/ukpersonalfinance would be a better place to create a personal finance strategy. MSE is basically a consumer review site - it’ll give you some easy suggestions to save money, and comparisons of some financial products, but if you don’t have a long-term financial strategy then money saving only takes you so far.

Thanks for writing this. Do you have any advice on getting a financial advisor? I've been wanting to hire one as a one-off to check I'm doing everything right. But not sure how to find a good person

No first hand experience I'm afraid, but the /r/UKPersonalFinance wiki has a good breakdown

Inspired by this post, a short intro to some of the important features and misconceptions of the UK personal finance landscape.

For further information:

This is only a brief overview, though I am happy to expand on any topic if there is interest. I am not your financial advisor and this is not financial advice.

The topics covered are tax, banking, investing, and giving. Links to further reading are provided for each section.

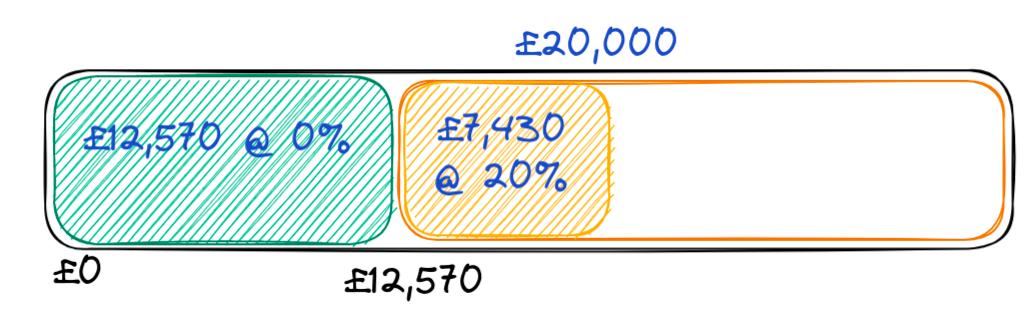

The UK has a marginal tax band system:

This is automatically calculated and deducted from your paycheck. Every month your employer should provide a payslip with your gross pay and deductions for tax, national insurance, pension, and student loan (if applicable). You should check this alongside online salary calculators like this, and speak to your HR/accounting department if there is anything you are not sure about.

Your salary is £20,000, the first £12,570 is taxed at 0%. The portion between £12,571 and £20,000 is taxed at 20%.

So you pay:

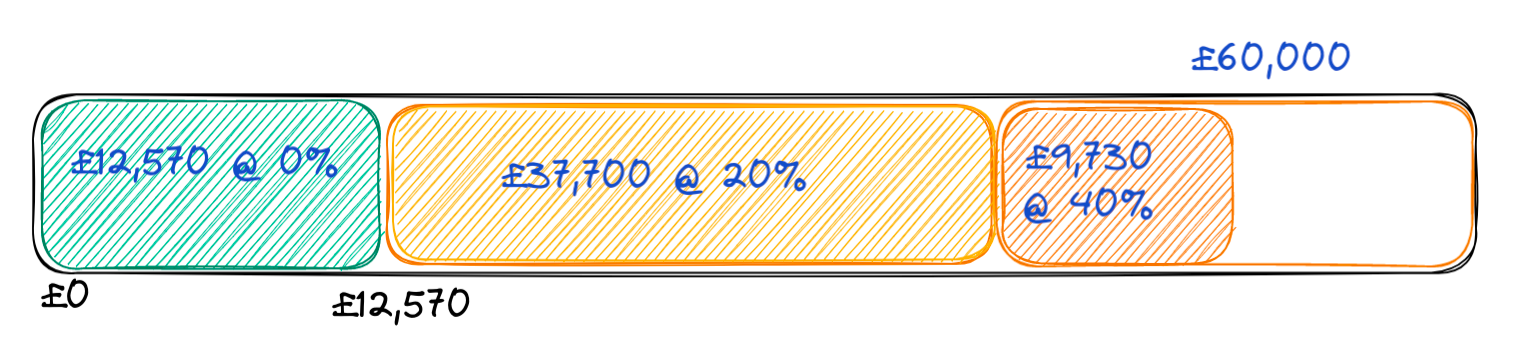

Your salary is £60,000, the first £12,570 is taxed at 0%. The portion between £12,571 and £50,270 is taxed at 20%. The portion between £50,271 and £60,000 is taxed at 40%.

So you pay:

Your whole income is not taxed at your marginal tax band so it is impossible to take home less money as a result of a pay raise.

These figures can be verified for example here (https://www.thesalarycalculator.co.uk/salary.php).

National Insurance is used to calculate your state pension. From the state retirement age[1], you get a weekly pension payment from the government.

The size of this payment depends on the number of 'qualifying years' that you have paid national insurance (or earned it via credits - eg. by being on certain kinds of benefits, or being a parent or carer). Note that this does not take into account how much national insurance you have paid, only the number of years that you contributed.

If you pay national insurance for 35 years you get the full state pension[2]. If you only pay national insurance for 20 years, you will get 20/35ths of that amount.

What you pay is also done on a marginal tax band system, though slightly confusingly the bands are per week/month rather than taking your total income over the whole year.[3]

Pretty much, what you pay 20% income tax on, you pay 12% national insurance on, and what you pay 40%+ income tax on, you pay 2% national insurance on.[4]

So a more accurate diagram is:

And our examples from earlier are now:

Your salary is £20,000, the first £12,570 is taxed at 0%. The portion between £12,571 and £20,000 is taxed at 20% with national insurance at 12%.

So you pay:

Your salary is £60,000, the first £12,570 is taxed at 0%. The portion between £12,571 and £50,270 is taxed at 20% with national insurance at 12%. The portion between £50,271 and £60,000 is taxed at 40% with national insurance at 2%.

So you pay:

This is best thought of as a 'graduate tax'. Most readers will be on the 'Plan 2' loan[5], and will pay back 9% on anything above £27,295. After 30 years your loan is cleared, regardless of how much you have paid back.

Yes there is a headline figure that you technically 'owe', and some interest rate, but that doesn't matter for most people. Only 20% of students are forecast to fully pay off their loan before it is automatically cleared after 30 years.

Another way of thinking about it is imagining that income tax is actually a £999,999,999 loan (with 999% interest added daily). That would actually make no difference in practical terms to your day-to-day life. You still just pay more tax the more you earn, and not worry about whatever 'balance' you owe.

One way to plan around these tax traps is by reducing your salary, the two most common ways being through charitable donations and pension contributions (covered later).

There are 'high street' banks with physical branches, and 'neo' banks which are app-only, and which one to go with is up to you. The app-only banks have deals with physical bank branches and post offices if there are things you need to do in person (like deposit cash), and the high street banks nowadays have pretty slick apps. So it's really a matter of personal preference.

The important thing is to pick a bank which is FSCS-certified. This means that your account is insured up to £85,000[7] by the government should the bank go bust. Notable 'banks' which are not FSCS-certified include Revolut and Wise[8]. Their terms and conditions do state that customer deposits are ring-fenced but we've all seen what that counts for these days...

I advise having (at least) 2 bank accounts, one daily driver and one backup one because banks can and do instantly freeze accounts if they detect suspicious activity and frustratingly can't give you any information while they conduct their compliance checks.

Banks in the UK are now required to allow read-only access to 3rd party apps because of a scheme called Open Banking. This means that you can use apps that connect to all your accounts and help you keep track of your spending and budgeting. Some are listed here, I recommend reading the privacy policies and what they do with your data before choosing to use one of them.

The Current Account Switch Service (CASS) makes it super easy to move over from one bank to another bank. It will move all outgoing standing orders and direct debits, and all payments to your old account will be forwarded to your new account for three years (maybe longer). And it happens within a week.

Many banks have switching offers[9] so it can be an easy way to make hundreds of pounds by opening a bank account and consistently switching it to whichever bank is currently running an offer. Make sure that you read the terms and conditions, usually highlighted on that MSE page.

In short, you should make sure that the information that financial institutions hold on you is accurate. If they think you've missed payments, or not paid back loans, or have pending court judgements against you, this will affect your ability to borrow money or get approved for products.

The MSE Credit Club covers Experian, and you can sign up to ClearScore as well and check them every month for any anomalies.

There are a few reasons why you might consider using a credit card (instead of a debit card) for your day-to-day spending:

At a basic level credit cards work like this:

So your January 1st spend doesn't leave your wallet until 14th February!

If you don't clear your balance every month, then you are charged interest.

A more advanced way is to apply for a credit card which is marketed as "0% on purchases for X months". This means that rather than paying off your full balance at the end of every month, you are allowed to make a small "minimum payment", incur no interest, and then pay off the entire balance at the end of the 0% offer.

Important details for credit cards:

There are an incredible number of scammers and fraudsters out there, some very sophisticated. This could probably be a post on its own but in short:

I will not share my opinion here or any specific strategies, but I recommend you understand:

The site Monevator is a good place to start, and has the best guide on low cost index funds and comparing brokers.

The /r/UKPersonalFinance wiki also has a good page on investing 101, and fees.

In order to start investing you have to use a broker. Basically a website where you can buy and sell stocks and bonds and funds. Factors that go into a broker are cost, availability of the things you want to buy, and trust.

There are a couple of ways in which brokers charge fees. Some charge an ongoing percentage of your total portfolio. So if you have £10,000 invested via the platform and the fee is 0.5%, you will pay £50 per year. Other brokers will charge a flat fee per year. Finally some brokers have a 'transaction fee' for every trade you make. When you run the numbers for how much you are investing and how many trades you plan on doing per year, you will likely find that for portfolios ~<£20,000 the percentage-fee brokers are more cost effective, and above that the flat-fee brokers are cheaper.

Different brokers allow you to trade different products. So make sure that the broker you choose will let you buy what you want. Vanguard for instance has a very limited selection.

There are some new very cheap brokers like Trading212, which on the surface look promising but the customer reviews are not great, with long delays and poor customer service.[10] Read customer reviews, check /r/UKPersonalFinance, see how long the company has existed for, and understand how they make their money.

What I'm describing here is the more common 'defined contribution' (DC) workplace pension, as opposed to 'defined benefit' (DB) schemes notably used in the civil service and NHS

Almost every employer is required to enroll employees in a pension scheme. This is different to the state pension outlined earlier. There is some variation in how it might operate exactly but in short, you will 'sacrifice' some of your salary and your employer will add to this, and this gets locked away until age 55 (though this is set to increase).

This is a hugely beneficial scheme to employees, since not only do you contribute to your pension out of your 'gross' salary (ie. before income tax and national insurance are deducted), but your employer also kicks in some extra cash, and when you cash it in in your retirement, there are tax advantages (like taking 25% of it tax-free).[11]

Your HR department will let you choose how much of your salary you sacrifice to your pension, to allow you to best plan for your retirement (and avoid some of the tax traps mentioned earlier).

So what happens to this money until you withdraw it? Your company will be using a pension provider or broker (eg. Aviva, Scottish Widows) to invest this money. You will have an online account where you can see what it is invested in, and (usually) be able to change the investments.

As you move from job to job, you will accumulate different workplace pensions at different pension providers. It is a simple process to move the money from an old pension to a new one and it can be worth doing this to keep things all in one place. The government have a service to help you track down your old workplace pensions.

The UK has a (truly ridiculous[12]) scheme where every tax year, you can invest £20,000 in stocks[13], and never have to pay any tax on any sale of those stocks for all time. This allowance doesn't carry over between years so if you don't utilise the full amount in one tax year, you don't get to make up for it the next year. ISAs are like a tax-free wrapper, and you can continue to manage your ISA investments from previous years without paying any taxes.

If you are investing outside of an ISA (which should only be because you've already maxed-out your £20,000 ISA in a tax year), you will be investing in something that is usually called a General Investment Account or GIA. There are taxes and duties to be paid on transactions within a GIA, such as capital gains tax, dividend tax, and stamp duty.[14]

Employers can set up a scheme whereby you can donate to charities directly from your gross salary meaning that you save on income tax (but not national insurance) and potentially avoid the tax traps described earlier. Sometimes these schemes are limited in the list of charities you can donate to, and you need to petition HR to get a new charity added.

One service that exists is the Charities Aid Foundation (CAF) which you can donate money to as if it were a charity, and then from there allocate your money to whichever charities you like (including GiveWell, EA, AMF etc).

Getting your employer to set up a payroll giving scheme, and getting that payroll giving scheme to plug in to CAF, is a low effort way to allow you and your colleagues to give in a tax-advantaged way.

Edit: You may also want to explore Tyve at your organisation

If you donate money after you've been paid your salary, you can use the Gift Aid scheme to allow the charity to claim some extra money and possibly receive a tax rebate yourself.

When you donate to a charity, you will be asked if your donation is eligible for Gift Aid, and possibly have to fill out a form. If you do this, then the charity is allowed to claim an extra 25% of your donation from the government. So if you donated £100, the charity could claim £25 from the government.

Note that you will already have paid income tax and national insurance on your £100, so it's not the boon that it sounds like.

If you are in the 40% (or higher) marginal tax band, you can claim back some money from the government. The amount is the difference between your marginal tax band (eg. 40%) and the basic rate of tax (20%) of your donation amount. So if you donated £100, the charity gets £125, and you can claim back £125 x 20% which is £25.

You claim this by filling out a self-assessment (which you need to complete if you earn £100,000+) or by ringing HMRC[15].

You can use CAF as an individual if you want to manage all your donations in one place. By doing all your donations through CAF, you will have a clear record of how much Gift Aid you can claim rather than it being scattered across different donation sites.

You earn £60,000 per year (making your marginal tax band 40%). You donate £1,500 through payroll giving. Your take-home pay only reduces by £900. (From £43,849.40 to £42,949.40, assuming no other deductions).

You earn £60,000 per year (making your marginal tax band 40%). You donate £1,200 to a charity after you've been paid. The charity can claim 25% from the government, giving them £1,500. And you can claim a tax rebate of £300 (1500 * 0.2), meaning you are only out-of-pocket £900.

Currently 66, with planned increases

Currently £185.15 per week

Which doesn't really make a difference other than for bonuses, or changing a job / getting a raise mid-way through the year.

From April 2022 l to November 2022, the rate was 13.25% so online tax calculators sometimes use that rate, sometimes use 12%, and sometimes use an average :)

If their undergraduate course started between 1st September 2012 and 31st July 2023. Other 'Plans' work similarly with different payment thresholds and tax rates

Or under 20 in approved education or training

If you temporarily exceed this, you are still fully covered. So if you receive an inheritance or sell a house, your temporary large balance is fully covered.

Formerly TransferWise

Sound too good to be true? Banks think that once you switch to them, you will stay with them for a long time and they can eventually upsell you..

Though they are FCA-regulated so your investments are protected should the company go bust

There are also inheritance tax advantages, and pensions are not counted for most means-tested benefit criteria

Giving a pretty giant tax break to those who have the means to invest £20,000 each year

There are also 'cash' ISAs which are tax-free savings accounts, but most savings interest is tax-free, so their usefulness is limited

You do have an annual capital gains tax-free allowance, and you can offset losses from previous years against gains. Other techniques to look into for minimising capital gains tax are 'bed and breakfast'ing and 'bed and ISA'ing.

I've heard Monday morning first thing is the best time :)

CAF charges a fee for its services. This seems crucial to deciding between GAYE/Payroll Giving vs Gift Aid — from the intro email when I registered to do GAYE:

My employer doesn’t cover it so I’m looking for an alternative method.