Hey! It's great that you're thinking about how to optimize your donations for taxes (and great that you're planning to donate so much!)

Some issues I found with your model:

Donating $100k doesn't give you $32k of tax rebate, because the marginal tax rate isn't 32% the whole time. From $165k of AGI, the marginal tax rate is 24%; so your total rebate looks more like 35*.32+65*.24 ~= $27k of tax rebate. (You kind of mentioned this in the post but I figured it was good to calculate the impact of, in case it was really high)

It's worth accounting for the fact that without any donations, you could have taken the standard deduction of $13k, which would be worth 13*.32 ~= $4k rebate already. So your total improvement from yearly donating to a DAF is ~= $23k, not $32k.

Two considerations against waiting at all are that

the value of money in EA could decline by more than 16%/year. One reason is that the total EA capital base has historically grown at over 30%/year, EA is still building grantmaking capacity towards an optimal level of spending, and there are diminishing returns to money.

Yeah, I need to put more thought into exactly how long I want to wait, but currently I'm thinking 3 - 5 years max before donating, maybe sooner if I quickly become more confident in my cause prioritization decisions.

Two additional things you may find interesting to consider:

Given the size of our national debt, taxes are quite likely to go up in the next few years, implying that you'll get more of a tax break for a charitable donation in a few years than you get now.

On the other hand, taxes are not entirely "money lost" - a good part of government spending goes into causes that you may not be entirely averse to - although it's hard to tell what a marginal dollar will do, e.g. whether it will be used to cut the taxes of millionaires, or to provide social benefits to the poor.

On the other hand, taxes are not entirely "money lost" - a good part of government spending goes into causes that you may not be entirely averse to - although it's hard to tell what a marginal dollar will do, e.g. whether it will be used to cut the taxes of millionaires, or to provide social benefits to the poor.

To your point on marginal impact - governments certainly don't spend money they take in dollar for dollar, and in fact it seems the correlation between intake and expenditure is quite far from 1:1. US government debt is on the order of trillions of dollars, so while its maybe slightly better than flushing your money down the toilet, I'm not sure I'd value it much higher

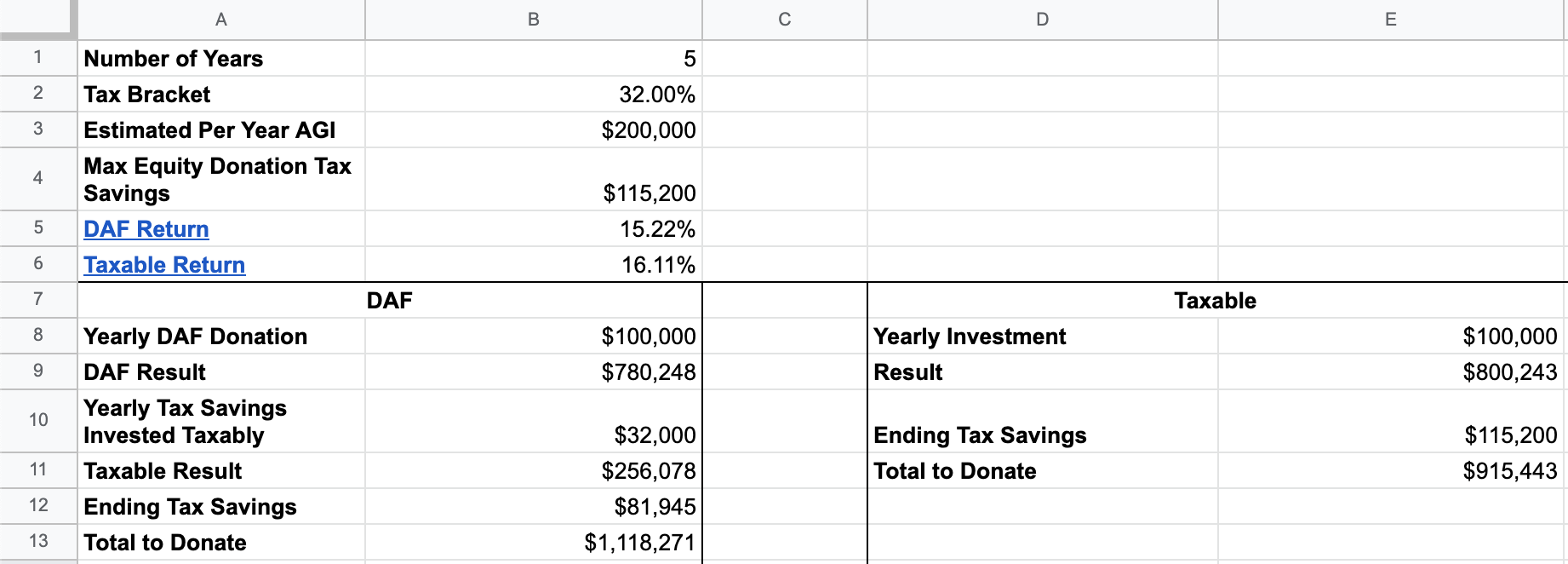

I'd like to invest some money to donate in 3 - 5 years after I've had more time to solidify my cause prioritization. I've been considering whether to donate the money now to a donor advised fund (DAF) and let it appreciate there before disbursing to nonprofits later or to invest it in a taxable investment account and donate the appreciated investments later.

I've always heard that taxable accounts tend to win over DAFs because DAFs take an additional yearly percentage as admin fees from your balance (e.g. 0.6%) and so earn less. But DAFs also let you take the tax deduction sooner whenever you contribute to one. I decided to put together a spreadsheet to see in what scenario a DAF might come out ahead.

The approach I found that resulted in the most money to donate in the end is a hybrid approach of donating yearly to a DAF, then investing the tax savings from the DAF donation in a taxable investment account. When ready to disburse money to a nonprofit, you disburse the appreciated funds from the DAF, donate the appreciated assets in the taxable investment account, and finally also donate the tax savings from donating the taxable investments.

I modeled this in a spreadsheet based on the following:

Yearly adjusted gross income of $200,000.

Yearly DAF contribution of $100,000.

US tax bracket of 32%.

Taxable investment return of 16.11% (10 year average return of the Vanguard S&P 500 ETF VOO minus its 0.03% expense ratio).

DAF investment return of 15.22% (10 year average return of the Schwab Total Stock Market Index Fund SWTSX offered by the DAF provider Schwab Charitable minus their 0.6% admin fee and the fund's 0.03% expense ratio).

This formula I found for computing investment growth.

It assumes:

The limitations applied to DAFs (e.g. only being allowed to disburse funds to registered charities) don't matter to you.

As you can see, the hybrid approach comes out ahead by a little over $100,000.

I found the big limitation with the taxable investment approach is that when donating the appreciated investments at the end of the time period, you'd be unable to deduct the full value donated even with the ability to roll over charitable deductions for up to five additional years due to the 30% deduction cap when donating appreciated equities. While the total you could donate from the appreciated assets is around $800,000, you'd only be able to deduct $360,000 ($200,000 AGI * 30% * 6 years) and so only have an additional tax savings of about $115,000.

Note that this model isn't 100% accurate, as I've made some tradeoffs between accuracy and simplicity. In particular, it suffers from the following limitations:

It only takes into account federal US taxes, not state taxes.

It treats 10 year average returns of the two investment options considered as the actual yearly returns, which isn't guaranteed.

Assumes your income doesn't increase during the investment period, and so you stay in the same tax bracket the whole time.

It doesn't account for you falling into a lower tax bracket after making the DAF donation.

Feedback Wanted

I'd appreciate feedback on this approach, as I'm considering taking it before the end of the year. Please let me know if there are any problems with this approach I haven't considered, any mistakes in my modeling, or any adaptations to the taxable investment approach that would cause it to beat the DAF approach.

Thanks to Jeremy Rosenthal for reviewing earlier versions of my spreadsheet and helping me improve it significantly.

AI Use Note: Main body text entirely human written. Claude (Opus 4.8) helped develop models of animal life histories in the appendix.

Cross-posted from Good Structures.

Executive Summary

* Animal advocates sometimes make claims like “there are X of this animal...

“How long have you been v*g*n?”

This is one of the most common icebreakers at animal protection events. It’s a baseline assumption, and it mostly holds true: if you’re out advocating for animals not to be tortured or abused, realistically these days you are v**n, or close. And it makes for good conversation. It seems fairly safe to assume when you meet strangers.

But this assumption is hurting the movement in a way which we don’t always notice: someone new comes into the sp...

Summary

Back in November 2023 I posted here to launch Spiro and raise our first $198k. Two and a half years later this is an update and a fundraiser for the next step.

The short version: we've now reached over-5,900 people with TB preventive medicine, including over 3,000 children under five years old. Our early results have held up well an...

{kind=link}

Hey! It's great that you're thinking about how to optimize your donations for taxes (and great that you're planning to donate so much!)

Some issues I found with your model:

Those both make sense. I'll try to incorporate them into my spreadsheet in the near future. Thanks for sharing!