Last updated 2026-07-11.

A donor-advised fund (DAF) is an investment account that lets you take a tax deduction now and give the money to charity later. When you give money to a DAF, you can deduct that money just as you would deduct a charitable donation. The DAF invests the money tax-free. At any time, you can write a grant from your DAF to a charity of your choice.

You can open a DAF through a donor-advised fund provider. A provider charges an administrative fee to invest your DAF and make donations when you recommend them.

For donors in the United States, which DAF provider is best?

The short answer

All the big DAF providers offer similar features. For most people, it doesn't matter much which one you choose.

- If you already have a DAF, you might as well keep using it.

- If you have a brokerage account at Fidelity, Schwab, or Vanguard, then the easiest thing to do is to open a DAF with your brokerage account. That way, you can manage all your investments in one place.

Otherwise, this handy flowchart can help you choose a DAF provider that fits your preferences.

The long answer

That flowchart should cover most use cases, but it might give you the wrong answer if you have unusual circumstances. In the rest of this post, let's look in detail at how DAF providers compare.

Cross-posted from my website.

My process

I made a list of every United States nationwide DAF provider I could find. I excluded regional DAF providers (example: Silicon Valley Community Foundation), providers that only support certain causes (example: National Christian Foundation), and providers that don't work with individual donors (example: American Online Giving Foundation). Your local community foundation might offer a better DAF than any of the national providers of my list, but there are too many community foundations for me to look at them all.

I ended up with eleven DAF providers (in alphabetical order):

- American Endowment Foundation (AEF)

- Charityvest (see disclaimer)

- Daffy (see disclaimer)

- Endaoment

- Fidelity Charitable

- GoFundMe Giving Fund (see disclaimer)

- Greater Horizons

- National Philanthropic Trust (NPTrust)

- Schwab Charitable

- T. Rowe Price Charitable

- Vanguard Charitable

This list is probably not comprehensive, but it's all the DAF providers I could find that meet my criteria.

I spoke to representatives at these providers to fill in some gaps in my knowledge. I also spoke to a few DAF users and financial advisors who manage DAFs at different providers.

I then eliminated five DAF providers:

- T. Rowe Price Charitable funds have excessively high fees (0.6% or higher).

- AEF and NPTrust both charge higher administrative fees than Vanguard/Schwab, offer a worse user experience, and don't have any special features to compensate.

- Endaoment runs on the blockchain, which weirds me out. Maybe it's fine, but Endaoment didn't appear at a glance to have any advantages over other DAF providers, so I declined to investigate further.

- Fidelity is nearly identical to Schwab, but it's slightly worse in a few ways (for more, see here).

Six DAF providers remain: Charityvest, Daffy, GoFundMe, Greater Horizons, Schwab, and Vanguard.

Caveat 1: I don't have good firsthand knowledge of any of these DAF providers except for Fidelity Charitable (which I used to use) and Greater Horizons (which I currently use). I created accounts at the other providers to get a sense of how they work, but I haven't tried to do anything fancy like set up an advisor-managed account. I had to make subjective judgments on things like UI, so don't take my claims as definitive.

Caveat 2: This article is not about whether you should open a DAF in the first place. You might want to keep your money in a taxable account, or maybe donate it all right away. But if you've already decided you want a DAF, then I hope this article will help you choose a provider.

Comparison

Let's compare Vanguard, Schwab, Greater Horizons, GoFundMe, Daffy, and Charityvest on these questions:

- What fees do they charge? [More]

- Do they have contribution/grant minimums? [More]

- What investment choices do they offer? [More]

- Do they have reasonable default investment options? [More]

- How flexible are their advisor-managed accounts? [More]

- Can you contribute complex assets such as cryptocurrency or real estate? [More]

- How good is the user experience? [More]

- How risky are the newer DAF providers (Charityvest, Daffy, GoFundMe)? [More]

Fees

Minimum fees:

- Charityvest has no minimum fee for cash accounts, and a minimum annual fee of $100 for accounts that hold stocks and bonds.

- Daffy has four tiers of accounts, with minimums of $36, $60, $240, and $480 per year.

- GoFundMe has no fees at all.

- Greater Horizons has a minimum annual fee of $500.

- Schwab has no minimum annual fee.

- Vanguard has a minimum annual fee of $250.

Charityvest, Greater Horizons, Schwab, and Vanguard offer tiered fee structures based on the account value. Daffy charges a monthly fee but no percentage-based fee. See Appendix for full details on the administrative fees for each provider.

GoFundMe has no administrative fees whatsoever. Users can optionally provide tips.

Daffy has a unique pricing structure. It offers four plans at different tiers: $3/month, $5/month, $20/month, and $40/month. The cheap tiers have contribution limits and restrictions on what features can be used.

Daffy is the cheapest DAF provider if you have a basic account with at least $6,000 or a $20/month account with at least $40,000. The $20/month tier has almost all the features of the $40/month tier, the main difference being that at $20/month, your contributions are limited to a maximum of $100,000 per year.

If you're on Daffy's $3/month plan, contributions are capped at $25,000 per year.

Daffy's $40/month plan has no limit. You can put $10 million in your DAF and still only pay $40/month. But be aware that Daffy has changed its fees more than once already, and may change them again.

If you only use a DAF as a convenient way to donate appreciated stock (or other assets), and you don't plan on keeping money in the DAF long-term, then you want a DAF with no minimum fee—your best options are Schwab and GoFundMe.

Daffy, Charityvest, and GoFundMe are startups, which makes them riskier. If we exclude the two startup-y DAF providers:

- If you have less than $25,000, Schwab is cheapest.

- If you have between $25,000 and $1 million, the three providers (Greater Horizons, Schwab, Vanguard) charge the same fees.

- For larger accounts, Vanguard is cheapest.

Minimums

Donor-advised funds have three types of minimums:

- Minimum contribution to create an account

- Minimum additional contribution

- Minimum grant size

- Minimum size for an advisor-managed account

|

Charityvest |

Daffy |

GoFundMe |

Greater Horizons |

Schwab |

Vanguard |

| Account Min |

$0 |

$0 |

$1* |

$0 |

$0 |

$25,000 |

| Contribution Min |

$15 |

$0 |

$5 |

$0 |

$0 |

$5,000 |

| Grant Min |

$15 |

$18 |

$5 |

$0 |

$50 |

$500 |

| Advisor Min |

$1 million |

N/A |

N/A |

$0 |

$0 |

N/A |

*GoFundMe has no account minimum, but it only allows you to donate up to 97% of your account balance at a time, to allow for market fluctuations. You can only donate a whole number of dollars, so effectively you are required to keep $1 in your account. I'm told they plan to change this requirement to make it more flexible.

Investment choices

If you don't know much about investing or you want to invest in whatever default your DAF provider uses, skip to the next section.

Let's compare the investment options for Charityvest, Greater Horizons, Schwab, and Vanguard.

Two providers are excluded from the table:

- GoFundMe doesn't let you pick your own allocation. Instead, you can choose between five pre-set allocations: cash, Treasury bonds, "diversified" (a mix of 40% stocks and 60% bonds), pure stocks (via low-cost index funds), and ESG (a mix of 40% ESG stocks and 60% ESG bonds).

- Daffy provides many more investment options than the other providers, so I discuss Daffy in its own section.

The DAF providers offer index funds covering the following asset classes.

|

Charityvest |

Greater Horizons |

Schwab |

Vanguard |

| US stocks |

|

|

|

|

| US small-cap |

|

|

|

|

| international stocks |

|

|

|

|

| emerging market stocks |

|

|

|

|

| US bonds |

|

|

|

|

| international bonds |

|

|

|

|

| TIPS |

|

|

|

|

| money market |

|

|

|

|

Vanguard offers funds covering many other market segments, including US growth/value, US REITs, European stocks, Pacific stocks, corporate bonds, dividend growth stocks, and commodities. Other than Daffy, Vanguard has the best variety in terms of index fund offerings.

The expense ratios on the funds themselves are low enough not to matter as long as you stick with the passively-managed funds. (Vanguard and Schwab offer a few actively-managed funds with higher fees, which you should avoid.) You can use any of these DAF providers to construct a globally diversified portfolio for an average expense ratio of about 0.05%.

Vanguard and Charityvest investors can approximately replicate the global market portfolio with 30% US stocks, 30% international stocks, 20% US bonds, and 20% international bonds. Investors with Schwab or Greater Horizons don't have access to international bonds, so the closest they can get is something like 30% US stocks, 30% international stocks, 40% US bonds.

All six providers offer ESG funds. All but Schwab's have low expense ratios; Schwab's ESG funds are unreasonably expensive.

If you want to invest in cryptocurrency, you can either do that through an advisor-managed account, or you can invest in a cryptocurrency fund through Daffy. Daffy is the only provider that offers crypto funds.

In summary:

- If you want the global market portfolio, use Vanguard or Charityvest because they offer an international bond index.

- If you want ESG funds, use any except Schwab.

- If you want cryptocurrency (and you don't want an advisor-managed account), use Daffy.

- If you want a wide diversity of options, use Vanguard.

- Otherwise, any provider is a good choice.

Default investments

Each of the five DAF providers offers a few default investment allocations. The defaults cater to investors with different levels of risk tolerance (conservative/balanced/aggressive).

Schwab's default investments are not good because they charge unconscionably high fees. Schwab does offer some low-fee options (listed in the previous section), so if you use Schwab, make sure you choose their low-fee funds instead of the defaults.

The other five providers—Charityvest, Daffy, GoFundMe, Vanguard, and Greater Horizons—charge low fees on their default investments. So if you use one of those providers, you don't need to worry about fees.

All six providers offer ESG portfolios. Again, though, Schwab's ESG funds are unreasonably expensive.

All the providers' default funds allocate too much to US stocks relative to the global market portfolio. I personally wouldn't use a default allocation because I'd want to invest more into international stocks. Every provider other than GoFundMe lets you choose your own allocation if you want to.

Daffy custom portfolios

Daffy is the only DAF provider that lets you build a custom portfolio from a long list of eligible ETFs. Not every ETF is eligible, but there are around 500 choices.

Custom portfolios are only available for the $20/month tier, so this is not a cost-effective offering for smaller DAFs.

The full list of ETFs includes the following categories, among others:

- All the big Vanguard index funds (VT, VTI, VXUS, VUG, VTV, BND, BNDX, VB, etc.)

- Alternative assets: emerging market stocks (VWO), high-yield bonds (USHY), commodities (COMT), gold (AAAU), bitcoin (FBTC), ethereum (FETH), REITs (VNQ/VNQI)

- Sector ETFs (technology, healthcare, consumer staples, etc.)

- Factor funds from Vanguard, iShares, and Schwab; including value funds (VFVA, IVLU), momentum funds (VFMO, IMTM), and multi-factor funds (VFMF, ISCF, EMGF)

Unfortunately, Daffy does not include some of my favorite ETF providers: AlphaArchitect, Avantis, Cambria, and Return Stacked. It also doesn't include any managed futures ETFs.

Advisor-managed accounts

Schwab, Charityvest, and Greater Horizons allow donors to appoint an investment advisor who can invest in things other than the pre-selected funds. Their program guidelines (links: Greater Horizons, Schwab (p. 11–14)) dictate what investments are allowed. Charityvest's advisor-managed accounts must hold a minimum of $1 million.

Vanguard and Daffy allow advisor-managed accounts, but advisors don't get to invest in anything beyond what individuals get.

Some examples of restrictions that apply to advisor-managed accounts at Schwab/Charityvest/Greater Horizons:

- "Risky" investments are not allowed, including margin, short sales, options (except covered calls/puts), futures, and swaps, unless held within a mutual fund or ETF structure. (Return stacked funds should be allowed; I know that Greater Horizons allows them because I hold a return-stacked (RSST) in my Greater Horizons DAF.)

- The advisor may not charge higher fees to the DAF than to the donor's personal accounts.

- The donor's family members may not serve as investment advisors.

Schwab has some additional restrictions that Greater Horizons does not:

- The account must trade using a Schwab brokerage account.

- The advisor must establish a benchmark and then track that benchmark reasonably closely. If the account deviates substantially from the benchmark, the advisor is accountable to Schwab's investment committee.

- The account must meet certain asset allocation requirements. For example, it cannot allocate more than 25% to any one security, more than 25% to emerging market equities, or more than 50% "to publicly traded funds that pursue alternative or non-diversified investment strategies, e.g., commodities or cryptocurrencies".

- Advisors may not invest in funds that they own or manage.

(Charityvest allegedly also has some restrictions, but they're not publicly listed.)

Greater Horizons provides the most flexibility to investment advisors. If I wanted to do anything unconventional, I would use Greater Horizons. (In fact, I do use Greater Horizons for exactly that reason.)

Contributing complex assets

Four of the six providers—Greater Horizons, Schwab, Charityvest, and Vanguard—can accept donations of complex assets, including cryptocurrency, private equity, real estate, and more. Daffy can accept cash, stocks/ETFs/mutual funds, private stock, and cryptocurrency, but not other types of exotic assets. GoFundMe can only accept cash, stocks/ETFs, and transfers from other DAFs.

Those four providers claim to accept more or less any type of asset that can legally be donated. But if you want to donate a large position in a complex asset, you should contact your DAF provider of choice to confirm they can receive it.

These providers all manage donations of complex assets through the same third party (Charitable Solutions LLC).

(Amusingly, AEF, NPTrust, and Schwab each claim to be "uniquely flexible" when handling complex assets. If they're all uniquely flexible, I guess that means none of them is?)

User experience

Most donors only care about the basic features of a DAF—they don't need fancy investment options or the ability to donate complex assets. So the main deciding factors for most people are (1) fees and (2) user experience.

Of the providers I'm focusing on, Greater Horizons easily has the worst sign-up process. You have to request that a customer service representative reach out to you. Then they send you a PDF form to fill out and the representative manually creates the account for you. In contrast, the other providers all let you sign up online and you can fill out your personal information on the website.

In the process of writing this article, I created accounts at Vanguard, Schwab, GoFundMe, Daffy, and Charityvest and went through a few common use cases. I found them all easy to use. Vanguard was slightly more complicated than the others. GoFundMe's "main flow" (sign up -> contribute funds -> donate to charity) was easy to use, but some things outside of the main flow were unintuitive.

Another important aspect of user experience is the quality of customer service. Good customer service matters, but it's difficult to assess—if you have a good/bad customer service experience, that might have more to do with the specific person you talked to than the quality of service in general. That said, I communicated through email and over the phone with all of the providers to get answers to my questions, and had decent experiences with all of them. My customer service experience might not generalize because reps from Charityvest, Daffy, and GoFundMe reached out to me after I published this article, which means they were on their best behavior (see disclaimer). That said, the Daffy rep didn't do a great job of answering my questions, and the GoFundMe rep did an excellent job. I have heard anecdotes from a personal friend and from an independent financial advisor who report that Daffy customer service was helpful and responsive when dealing with issues.

I've heard that Schwab has particularly good customer service. I've heard Vanguard the brokerage has worse customer service, but that Vanguard Charitable has a separate customer service department and it's better than Vanguard the brokerage.

A side note: You might think it's a good idea to evaluate user experience by looking at reviews on a site like Trustpilot or Better Business Bureau. I would avoid looking at those sites because they are protection rackets—they offer to remove bad reviews in exchange for money. So the companies with good reviews are just the ones who pay to get the bad ones deleted.

I can't give objective metrics for user experience, but my ranking based on my personal experience is Charityvest > Schwab > Daffy > GoFundMe > Vanguard > Greater Horizons.

How risky are new DAF providers?

Daffy, Charityvest, and GoFundMe's DAF offerings only started a few years ago. If they can't earn enough money to sustain themselves, they might have to dissolve customers' accounts and use their money to pay their bills (which they have a legal right to do, as established by National Heritage Foundation v. Highbourne Foundation). You might not want to use those DAF providers if you're concerned about the risk.

I believe that:

- There is a non-trivial probability that Daffy/Charityvest will close down and you'll have to transfer your money to another DAF provider. (I have no reason to believe they're riskier than the average startup, but most startups go out of business.) GoFundMe is an older company, but its DAF offering is new, so there is a non-trivial probability that it will stop offering DAFs.

- If your provider does close down, they will almost certainly let you transfer your money to another DAF provider—it's unlikely that you will lose your money permanently.

Here's why you are unlikely to lose your money:

Charityvest and Daffy both use a financial structure that is novel for DAF providers. They were founded concurrently with sister corporations (Vennfi, Inc. for Charityvest and Aside, Inc. for Daffy). Vennfi/Aside receive funding from VC firms and Charityvest/Daffy pay the corporations to develop their technology. This lets the corporations run at a loss using VC funding until the DAF providers grow large enough to make the corporations profitable.

This structure works in donors' favor. If the for-profit corporation declares bankruptcy, VC funders can only make bankruptcy claims against the corporation, not against the DAF provider, so donors' money is safe. And according to their 2022 public filings (viewable through the Florida Check-A-Charity website), Charityvest/Daffy have very little debt (or at least they did as of 2022).

(GoFundMe Giving Fund has a similar structure, except that its partner for-profit (GoFundMe) is a well-established company in its own right.)

Even if you don't lose your money, there's a risk that DAF providers raise their fees. Since the first version of this article in 2021, Schwab/Vanguard/Fidelity have not changed their fees at all; but Charityvest and Daffy have both changed their fees at least once. If you open an account with Charityvest/Daffy on the premise that it's cheaper, that premise might stop being true at some point. (Charityvest used to have lower fees than the big DAF providers, but in early 2025 they raised their fees and now they're tied with Fidelity and Schwab.)

It's possible to transfer money from one DAF to another, so if your provider starts charging exorbitant fees, you can move away from it.

The best DAF provider(s)

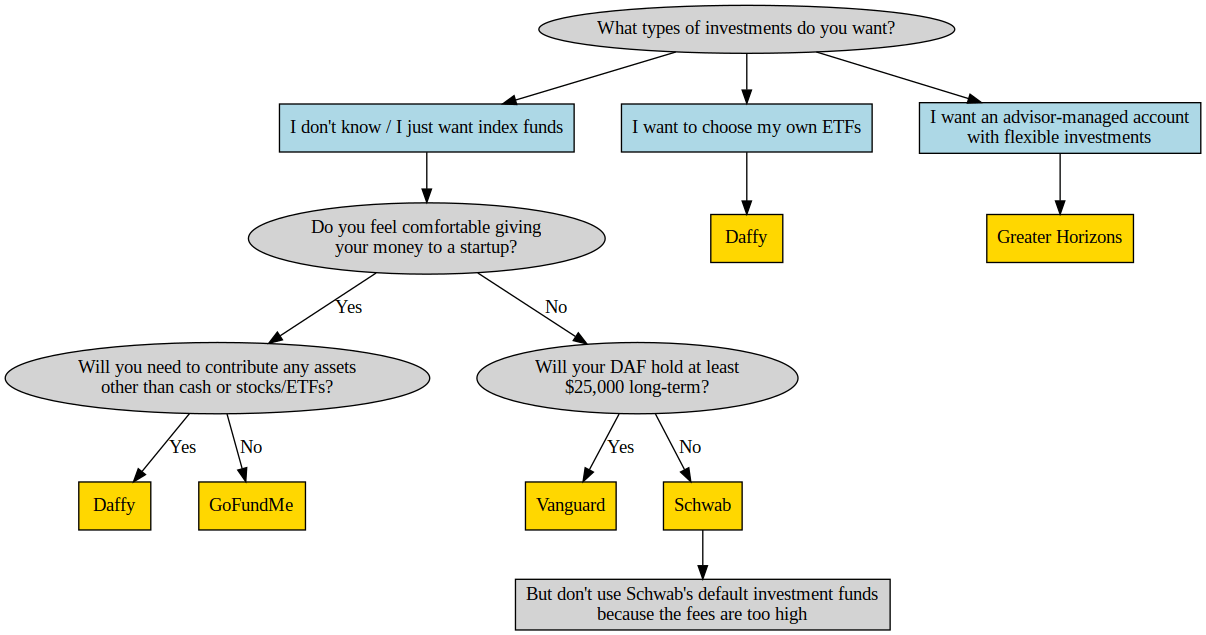

This flowchart shows the best DAF provider depending on your circumstances.

A text description of this flowchart:

- If you want an advisor-managed account, use Greater Horizons.

- If you want to choose your own ETFs, use Daffy.

- If you feel comfortable giving your money to a startup with an unproven track record:

- If you will need to contribute any assets other than cash or stocks/ETFs, use Daffy.

- If not, use GoFundMe.

- Otherwise:

- If your DAF will hold at least $25,000 long-term, use Vanguard.

- If not, use Schwab—but remember not to use the default investment funds because their fees are too high. Set your allocation to cheap index funds instead.

Some other factors you might care about, that I didn't put on the flowchart because it would be too big:

- If you only plan on keeping money in your DAF for a short time, use Schwab, GoFundMe, or Charityvest because they let you keep an empty account without charging you (the others charge a flat fee).

- If you want to not just contribute cryptocurrency, but invest in cryptocurrency (without using an advisor-managed account), you need to use Daffy.

- If you want to donate exotic assets such as real estate or artwork, don't use Daffy or GoFundMe. Any of the other providers should be able to accommodate you. (Among the other providers, Vanguard has the lowest fees.)

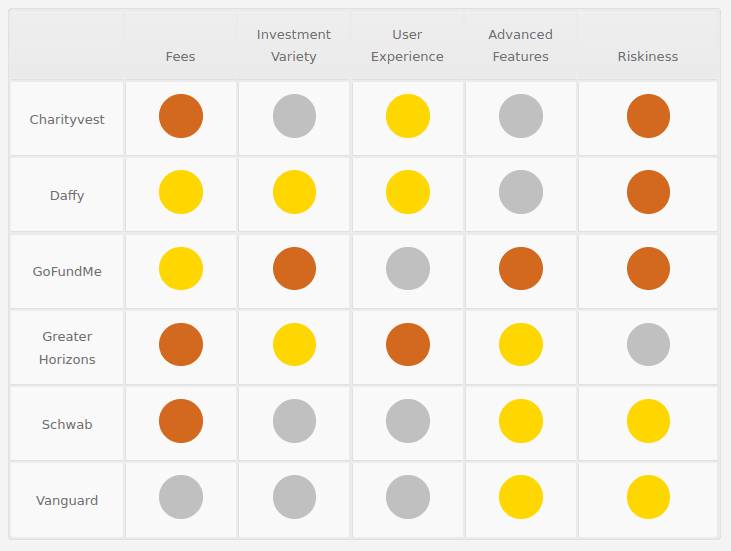

This table illustrates my evaluation of the providers along five dimensions, ranked as bronze, silver, or gold.

This article only covered Charityvest, Daffy, GoFundMe, Greater Horizons, Schwab, and Vanguard. That's not because I believe these are better across the board than the other providers. For example, I think Fidelity has a better UI than Vanguard; and NPTrust offers more flexibility than Schwab for advisor-managed accounts. Rather, I chose these DAF providers because each one is the best at something, while the other providers are not the best at anything (even though they are good at some things).

More on other DAF providers

Even though I didn't compare them in detail, here are my impressions of five other DAF providers, ranked from most to least favorable.

- Fidelity Charitable is basically as good as Schwab. I like Fidelity a little bit less because it provides fewer investment options and the UI is slightly harder to use, but Fidelity still seems like a fine choice as long as you're careful to avoid their high-fee investment options.

- Bonus fact: If you have at least $5 million, Fidelity Charitable lets you manage your own investments (without appointing an advisor). I don't believe any of the other DAF providers let you do that.

- NPTrust and AEF are maybe passable but they have some serious issues:

- They're more opaque than the other DAF providers, and I had a bad experience talking to them.

- They make it more difficult to set up an account.

- For advisor-managed accounts, they impose more restrictions on the investment advisor than Greater Horizons does.

- They charge somewhat higher administrative fees than Fidelity/Schwab/Vanguard.

- NPTrust's pre-selected investment funds are too expensive. NPTrust should only be used with an advisor-managed account. AEF does not have pre-selected funds—you must appoint an investment advisor.

- AEF's website is so buggy that it's unusable on Firefox. Even ignoring the bugs, AEF has a much worse UI than Fidelity/Schwab/Vanguard.

- A former AEF user reached out to me to give some more information about AEF:

- The donor portal has restricted functionality, for example there is no way to get a statement of transactions.

- AEF charges a 1% fee if you withdraw or grant >80% of your funds within six months of opening the DAF.

- T. Rowe Price Charitable is too expensive to be worth using. If you have a DAF at T. Rowe Price, you should consider switching to a new provider.

- Endaoment runs on the blockchain. I don't know how that works and I would be nervous about depositing any money without getting a better understanding first. Maybe it's fine; all I'm saying is I don't know, and I'm not going to trust them with my money if I don't know. Other than the blockchain thing, Endaoment seems better than the legacy DAF providers.

Appendix: Table of administrative fees

Fees can be found at these links:

AEF, Charityvest, Endaoment, GoFundMe, Fidelity, NPTrust, Schwab, T. Rowe Price, Vanguard.

Greater Horizons does not publish its fees online. I learned what it charges by speaking to a representative. I don't like it when companies don't publish their fees, but I will respect Greater Horizons' preferences by not disclosing them. If you want to know the specifics, contact them directly.

Minimum fees:

|

AEF |

Charityvest |

Daffy |

Fidelity |

NPTrust |

Schwab |

T. Rowe Price |

Vanguard |

| Minimum Fee |

$500 |

$48 |

$36 |

$100 |

None |

None |

None |

$250 |

Percentage-based fees:

| Account Value |

AEF |

Charityvest |

Fidelity |

NPTrust |

Schwab |

T. Rowe Price |

Vanguard |

| First $250K |

0.70% |

0.60% |

0.60% |

0.85% |

0.60% |

0.50% |

0.60% |

| Next $250K |

0.70% |

0.60% |

0.60% |

0.70% |

0.60% |

0.50% |

0.60% |

| Next $500K |

0.35% |

0.30% |

0.30% |

0.60% |

0.30% |

0.39% |

0.30% |

| Next $1.5M |

0.25% |

0.20% |

0.20% |

0.45% |

0.20% |

0.18% |

0.13% |

| Next $2.5M |

0.15% |

0.15% |

0.15% |

0.25% |

0.15% |

0.12% |

0.13% |

| Next $5M |

0.15% |

0.10% |

|

0.15% |

0.13% |

0.10% |

0.13% |

| Next $5M |

0.15% |

|

|

0.10% |

0.12% |

0.10% |

0.13% |

| Next $15M |

0.10% |

|

|

|

0.10% |

0.09% |

0.10% |

| Over $30M |

|

|

|

|

|

|

0.05% |

Caveats:

- Charityvest has no minimum fee on cash-only accounts.

- Daffy charges $36 per year, $60 per year, or $240 per year, depending on your account type. It does not charge any percentage-based fees.

- Fidelity uses a flat fee schedule on accounts with over $5 million.

Some observations:

- GoFundMe is the cheapest because it's free.

- Otherwise, Daffy is the cheapest if you have more than $40,000.

- Other than Daffy and GoFundMe, Charityvest is cheapest or tied for cheapest above $6,000, and Schwab is cheapest below $6,000.

- T. Rowe Price is on the low end for administrative fees, but its investment options charge high expense ratios. It only offers two reasonably-priced funds (an S&P 500 index fund and a "balanced" index fund).

- Even though Schwab has lower fees than Vanguard at one tier, there is no account value at which Vanguard has a higher total fee.

- Even though NPTrust has lower fees than Schwab at one tier, there is no account value at which Schwab has a higher total fee.

- Fidelity's flat fee structure above $5 million means that near the bottom of a tier (e.g., $11 million), it's cheaper than Schwab or Vanguard, and near the top of a tier (e.g., $19 million), it's more expensive.

Disclaimers

The original version of this article did not include Charityvest, Daffy, or GoFundMe. I updated the article when representatives from those DAF providers reached out to ask me to include them. Everything I wrote about them is my own opinion.

(The original version of this article did not include Endaoment, but I discovered it on my own, and I have nothing to disclaim with respect to it.)

I learned about Charityvest in May 2021, when the CEO, Stephen Kump, emailed me to ask me to review it prior to its public launch. He gave me access to the beta (which I used to check out Charityvest) and added $20 to my account (which I did not use, to avoid any conflict of interest). I did not receive any other compensation for writing about Charityvest.

In early 2022, a representative from Daffy reached out to me, and I proceeded to forget about their message for a year. I rediscovered it in late 2023, when a couple of other people asked me for my opinion on Daffy and I decided to update this article to include it. I did not receive any incentive from Daffy.

A representative from GoFundMe reached out in March 2026 to tell me that they had just launched a DAF offering. I did not receive any incentive from GoFundMe.

Changelog

- 2022-03-10: Add a Charityvest review and add it to the recommendation flowchart.

- 2023-01-06: Update fee minimums.

- 2024-04-24: Significant revisions:

- Add changelog.

- Add a Daffy review.

- Add a new section on default investment options.

- Correct an error: I previously wrote that Vanguard's account minimum is $0, but it is $25,000.

- Update information on T. Rowe Price: I originally wrote that it only offered one reasonably-priced fund, but now it offers two.

- Substantially change recommendations based on a number of factors:

- Add consideration to a provider's default investment options. Previously, I hadn't considered them at all, but I expect many (most?) DAF users will use the defaults, so that was an oversight.

- Downgrade my recommendation of Schwab. Previously, I had Schwab as my top recommendation for most people, but their default funds are too expensive.

- Add Daffy as a possible recommendation and rearrange the flowchart accordingly.

- Remove the "best DAF provider for most people" recommendation (previously I recommended Schwab). Every DAF provider has some hiccup that a significant number of people won't like, so I don't think I can reasonably give a general recommendation. (Schwab's default funds are too expensive; Vanguard is too expensive for small donors; Charityvest/Daffy are new orgs that might go out of business.)

- Generally rewrite to increase clarity.

- 2025-01-31: Add some more information about AEF.

- 2025-02-05: Update to reflect Charityvest's recently raised fees. Previously Charityvest was cheaper than Fidelity/Schwab at most account values, and now it's a three-way tie up to $5 million.

- 2025-05-09:

- Daffy now allows you to choose your own ETFs. Update to explain this and incorporate it into the flowchart.

- On the previous update, I forgot to account for Charityvest's raised fee when determining which DAF provider is cheapest. Update to fix this.

- 2025-12-10:

- Update based on Daffy's fee tier changes. Previously the lower tiers had a lifetime contribution limit, which is now annual; the $20/month tier is now restricted to a $100,000-per-year contribution, and there is a new $40/month tier without such a restriction.

- Daffy now accepts donations of private stock.

- Under How risky are new DAF providers?, add something about how new DAF providers may raise their fees, because they've done this a few times already.

- Update the image and flowchart description under The best DAF provider(s), which I forgot to change in my May 2025 edit.

- Update the bronze/silver/gold rankings, which I also forgot to change last time.

- 2026-07-11: Add information on Endaoment and GoFundMe Giving Fund; change flowchart accordingly.

Thanks for writing this! I opened and donated to a Charityvest DAF mostly based on this post.