I think reducing x-risk is by far the most cost-effective thing we can do, and in an adequate world all our efforts would be flowing into preventing x-risk.

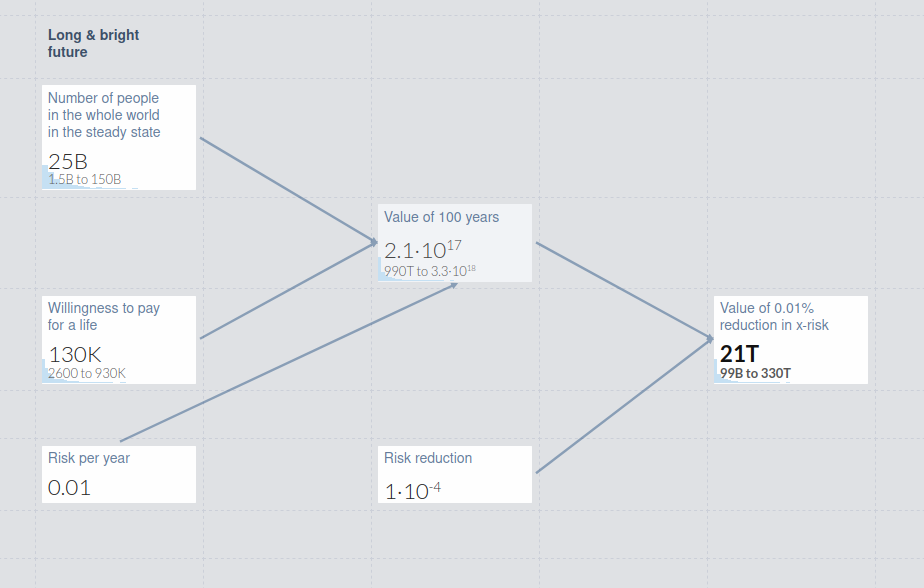

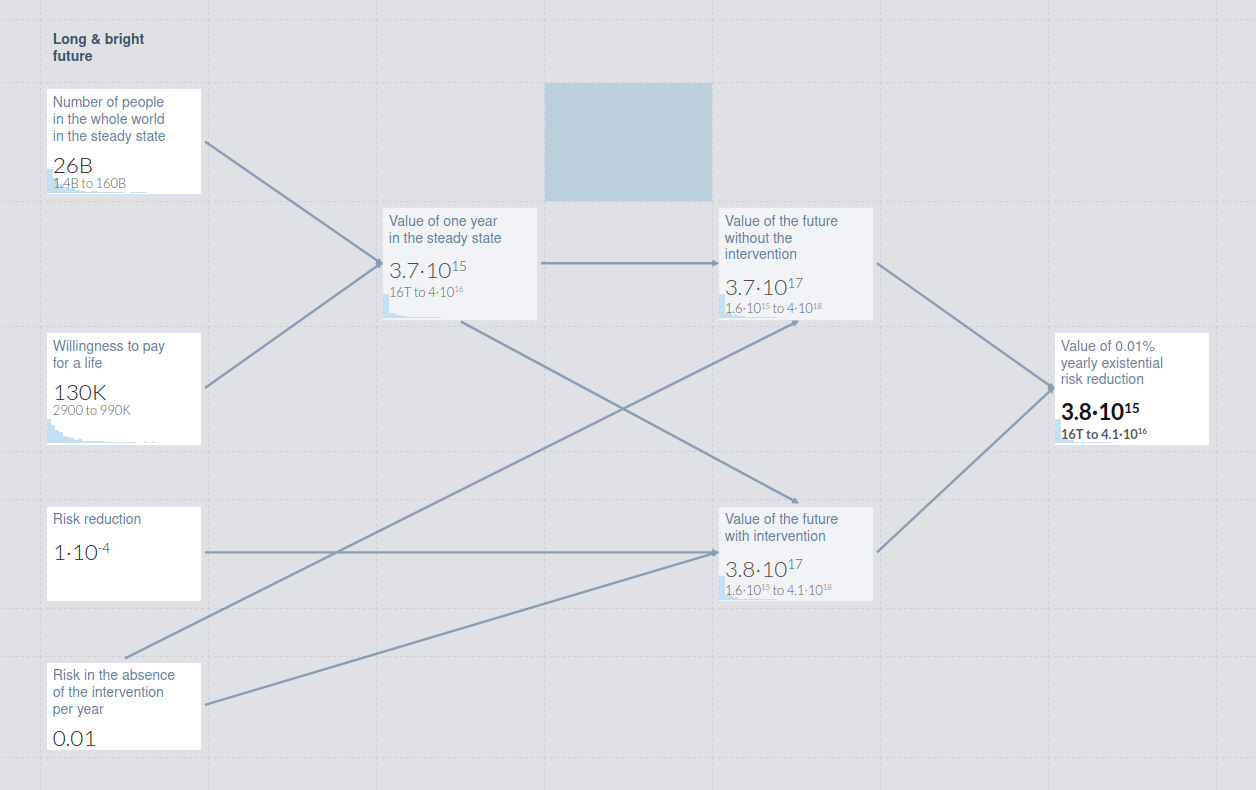

The utility of 0.01% x-risk reduction is many magnitudes greater than the global GDP, and even if you don't care at all about future people, you should still be willing to pay a lot more than currently is paid for 0.01% x-risk reduction, as Korthon's answer suggests.

But of course, we should not be willing to trade so much money for that x-risk reduction, because we can invest the money more efficiently to reduce x-risk even more.

So when we make the quite reasonable assumption that reducing x-risk is much more effective than doing anything else, the amount of money we should be willing to trade should only depend on how much x-risk we could otherwise reduce through spending that amount of money.

To find the answer to that, I think it is easier to consider the following question:

How much more likely is an x-risk event in the next 100 years if EA looses X dollars?

When you find the X that causes a difference in x-risk of 0.01%, the X is obviously the answer to the original question.

I only consider x-risk events in the next 100 years, because I think it is extremely hard to estimate how likely x-risk more than 100 years into the future is.

Consider (for simplicity) that EA currently has 50B$.

Now answer the following questions:

How much more likely is an x-risk event in the next 100 years if EA looses 50B$?

How much more likely is an x-risk event in the next 100 years if EA looses 0$?

How much more likely is an x-risk event in the next 100 years if EA looses 20B$?

How much more likely is an x-risk event in the next 100 years if EA looses 10B$?

How much more likely is an x-risk event in the next 100 years if EA looses 5B$?

How much more likely is an x-risk event in the next 100 years if EA looses 2B$?

Consider answering those questions for yourself before scrolling down and looking at my estimated answers for those questions, which may be quite wrong. Would be interesting if you also comment your estimates.

The x-risk from EA loosing 0$ to 2B$ should increase approximately linearly, so if x is the x-risk if EA looses 0$ and y is the x-risk if EA looses 2B$, you should be willing to pay d=0,01%y−x2B$ for a 0.01% x-risk reduction.

(Long sidenote: I think that if EA looses money right now, it does not significantly affect the likelihood of x-risk more than 100 years from now. So if you want to get your answer for the "real" x-risk reduction, and you estimate a z% chance of an x-risk event that happens strictly after 100 years, you should multiply your answer by 1/(1−z%) to get the amount of money you would be willing to spend for real x-risk reduction. However, I think it may even make more sense to talk about x-risk as the risk of an x-risk event that happens in the reasonably soon future (i.e. 100-5000 years), instead of thinking about the extremely long-term x-risk, because there may be a lot we cannot foresee yet and we cannot really influence that anyways, in my opinion.)

Ok, so here are my numbers to the questions above (in that order):

17%,10%,12%,10.8%,10.35%,10.13%

So I would pay 0.01%0.13%2B$=154M$ for a 0.01% x-risk reduction.

Note that I do think that there are even more effective ways to reduce x-risk, and in fact I suspect most things longtermist EA is currently funding have a higher expected x-risk reduction than 0.01% per 154M$. I just don't think that it is likely that the 50 billionth 2021 dollar EA spends has a much higher effectiveness than 0.01% per 154M$, so I think we should grant everything that has a higher expected effectiveness.

I hope we will be able to afford to spend many more future dollars to reduce x-risk by 0.01%.

For the top number, I'm aware of at least one intervention* where people's ideas of whether it's a good idea to fund moved from "no" to "yes" in the last few years, without (AFAIK) particularly important new empirical or conceptual information. So I did a backwards extrapolation from that. For the next numbers, I a) considered that maybe I'm biased in favor of this intervention, so I'm rosier on the xrisk reduced here than others (cf optimizer's curse), and grantmakers probably have lower numbers on xrisks reduced and b) considered my own conception of how much capital may come to longtermist EA in the future, and decided that I'm probably rosier on our capital than these implied numbers will entail. Put another way, I started with a conservative-ish estimate, then updated down on how much xrisk we can realistically buy off for $X at current margins (which increases $/xrisk), then updated upwards on how much $s we can have access to (which also increases $/xrisk).

My friend started with all the funds available in EA, divided by the estimated remaining xrisk, and then applied some discount factor for marginal vs average interventions, and got some similar if slightly smaller numbers.

*apologies for the vagueness