Comments

I personally know of thousands of extra pounds going to AMF because of this post.

Thank you SO much for putting this together. Tax regime in the UK is super non-intuitive to me (I've only ever just had to deduct donation from taxable income to calculate my new tax position).

Your spreadsheet helped me properly understand how GiftAid works. Really good job!

I knew a lot of this before donating but I still lost some money. I'll describe how. I got my first UK job in September 2015 for a company that did not have payroll giving scheme set up. I donated some money in January 2016 and May 2016 and I let the charity claim gift aid (25%) in both cases. Since I was a 40% tax payer, I was eligible to claim the difference between my tax rate and gift aid (40%-25%=15%) from the government. However, I was told that I could only claim this difference for my May 2016 donation because I didn't pay enough tax in the tax year that ended on April 2016.

If you call tax helpline (https://www.gov.uk/government/organisations/hm-revenue-customs/contact/income-tax-enquiries-for-individuals-pensioners-and-employees), they generally can answer all the questions about your situation.

Thanks for that. As you mentioned in your guide I only recently realised that as I submit self assement return, I don’t need to donate by April 6 tax year end, but can do so before I submit the self assement return in following January which gives me an extra 9 months to work out how much I can donate.

Thanks for writing this! The interaction between donations and the reductions in personal allowance are interesting, and I would not have thought of them otherwise.

This post is extremely helpful, and I have referred to it multiple times as I plan my finances. Thanks again for putting it together.

This was a nice post. The tax laws changed in the US at the end of 2017 and I’m preparing a post to summarize the donation-specific changes. Found this when I was browsing past posts.

I'd love to see the comparison in multiplier for donating stock versus cash in the UK. In the US our largest donors often give in stock because the donor avoids capital gains tax AND can deduct the FMV (fair market value) of the stock. Would be valuable to see how that plays out in the UK for you larger donors.

You can use a donor advised fund in the UK to whom you can donate appreciated stock . As you note this allows you to avoid capital gains and provides a deduction. There is at least one donor advised fund in the UK which allows you to make the donation to both UK and US charities (National Philanthropic Trust NPT ). The Charities Aid Foundation in the UK is also long established - not sure if it allows donation to UK and US as well and seems to accept appreciated stock too. They have an extensive list of UK charities that have passed their scrutiny .

I have used NPT and they work well. However I think that I may have restricted my funds within the trust to the FTSE index which was probably not optimal! NPT are a bit more recent to the UK and do make the charity go through some hoops to make sure they are totally legitimate if they are not on their existing list . (this happened when I made a donation to my university). They charge fees which get significant if you hold less than about £15,000 in the fund . Certainly worth considering though.

This is awesome - thanks for writing it up. I'm hoping it gets sidebarred or otherwise kept somewhere for future reference, and for future years!

On the subject of doing a tax return: I've been using TaxCalc for the last few years. It's about £30 for a licence but covers all sorts of complex scenarios and is super straightforward - I'd recommend it.

For anyone donating their income, being aware of tax rules and making proper use of available deductions can result in significantly increased donations. There are some existing resources on US tax rules (e.g. Ben Kuhn's post), but I hadn't come across any for UK tax rules yet.

So in the hope of saving someone else (and future me!) some time, here's my current understanding. If you'd like to share this with others, there's a less EA-oriented version of this post on my personal blog. All the calculations and charts are in this spreadsheet. There's also a personal tax calculator tab in the spreadsheet.

Note: I'm not an accountant, and I'm definitely not qualified to give tax advice. Almost everything here comes from the tax relief section on the gov.uk website. Before making any decisions, check that what I've written is correct and applies to your situation! If you spot any mistakes, please let me know and I'll do my best to correct them. Tax thresholds and rates here are for 2018/2019. Scotland has different rates.

Summary:

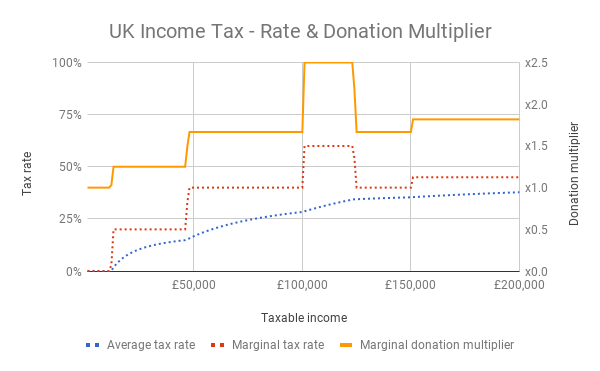

One key income bracket is £100-123.7k. If you're in this bracket, you're paying an effective marginal tax rate of 60%! So for example you could make a £20k donation by giving up only £8k.

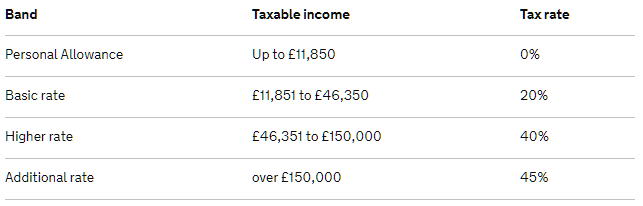

UK income tax is progressive, i.e. increases with income.

UK income tax brackets 2018/2019 (source)

The chart below shows what total income tax looks like for various income levels, and how that breaks down into the various bands. I've included data up to £200k since beyond that it just goes up linearly, and if you're in that band you might consider investing in proper tax advice!

Interactive version of this chart.

A few things you'll notice about the chart:

The steepness of that top line represents your marginal tax rate - i.e. how much tax you'll pay on every extra £1 you earn at that level. This is a useful thing to look at, because it affects the 'donation multiplier' you'll get at that level - i.e. how much your chosen charity will get for every £1 in net income you give up.

Here's another chart which shows that relationship more clearly:

Interactive version of this chart.

What does this second chart show? The yellow line shows the donation multiplier for £1 at each level:

If you're a basic rate taxpayer (i.e. your total taxable income is up to £46.35k) then you don't need to worry about claiming tax back - Gift Aid takes care of it.

Beyond that there are three options I'm aware of: Payroll Giving, doing a tax return, or asking HMRC to change your tax code.

Payroll Giving is great, but your employer needs to be set up for it. If they are, then all you need to do is tell your employer your intended monthly donation. They'll take it straight out of your gross salary and give it to your charity of choice, without any tax being deducted.

If you fill in a Self Assessment tax return, there's a section on charitable donations. Doing one isn't exactly fun, but it's not as difficult as it sounds (and I've heard it's much easier than the US system!). All your employer's data will be imported already, so you only need to fill in additional details on your donations and any other relevant sections. If you're doing regular donations then the next option is probably better for you, but if you want to be able to do things like optimising the tax year of your donations then you'll need to fill in a Self Assessment tax return. And if you earn over £100k you'll have to do one anyway.

Until fairly recently, I thought those were the only two options. It turns out there's a third one! If you give regularly and don't fancy filling in a tax return, you can just ask HMRC to change your tax code. All you need to do is tell them how much you're donating every month, and they'll change your tax code to increase your personal allowance - thereby reducing the amount of tax you'll pay. I think you can probably do this over the phone, but I found their online chat function easy enough. (obviously always make sure you keep a record of all your donations)

There's a pretty useful rule which can allow you to claim tax back on donations made now as if they were made in the previous tax year (assuming you're filling in a Self Assessment tax return). This is great if:

Why does this work? When you fill in a Self Assessment tax return, you do that for the previous tax year (April-April). And you have until January 31 in the following year to do this (i.e. almost 10 months after the end of the tax year).

You're allowed to account for donations made in the current year as if they happened last year. Specifically: "you can also claim tax relief on donations you make in the current tax year (up to the date you send your return) if you either: want tax relief sooner, or won’t pay higher rate tax in current year, but you did in the previous year".

* In this post I've focused on income tax. I haven't taken into account National Insurance payments in any of the calculations, as these aren't deductible. I also haven't modelled the impact on other things like student loan repayments or pension allowance increases. As for income tax, there are some limits to the amount you can claim back, but they're quite high - "Your donations will qualify as long as they’re not more than 4 times what you have paid in tax in that tax year".

Thanks Harald, this is a terrific article and should be required reading for all UK donors. I love the graphs in particular and the content looks accurate to me. I think gift aid and tax relief are important considerations which increase the benefit of giving now relative to giving later- particularly for higher rate taxpayers. In retirement, most people will have a significantly lower income than during working life, and very few people indeed are likely to be higher rate taxpayers in retirement and benefit for a 1.67 multiplier. There also seems to be little tax benefit to donating to charities in your will - unless you have a large estate beyond the high threshold for inheritance tax (effectively 650,000 for married couples) and presumably there is no gift aid on bequests except for any income tax you paid in your final year of life?