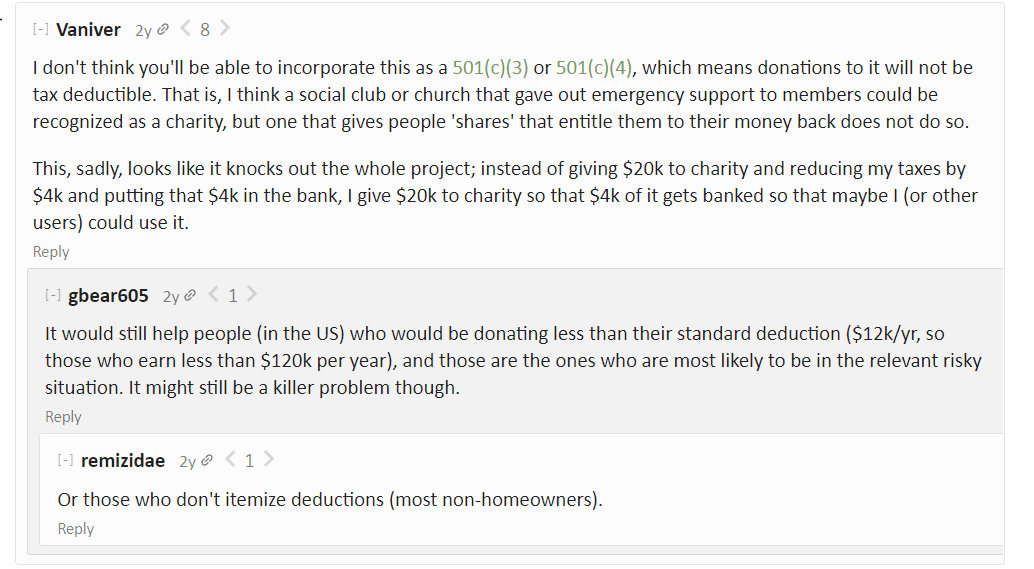

Comments

Thanks for the interesting idea! It makes me happy that people see EA also as a community and care for other community members.

Regarding the specifics, I'm not really clear on why an emergency fund should be coupled with donations.

If this is intended as a non-profit mutual aid fund, I don't think it should be related to charity at all. In my last workplace there was an employee mutual aid fund that each person could opt into by putting in a sum of money (or maybe it was sick days?), and apply for aid whenever needed.

Other than lowering risks for donations specifically, I would think EAs who don't earn enough to donate would be at greater risk for financial emergencies. Moreover, "having and donating money" is really not the only effective altruistic thing one could do.

On the other hand, if this is intended as a kind of insurance and is supposed to actively contribute to charities, wouldn't it make sense to adopt a for-profit insurance attitude (except for the tendency to avoid paying out), take premia from members and cap the payouts in some way, and forward the profits specifically to effective charities?

Even in this case, I think it's problematic to have payouts be proportionate to a member's contributions, as that means the people who'll get the highest expected value from the fund are the richest, while the likelihood of actually needing those funds is disproportionately higher for the poorest.

This seems like the type of infrastructure that should be experimented with on a small scale rather than heavily debated

Agreed! I have applied to ACX Grants to set up a trial version. If anyone else is interested in funding this, send me a message.

I was going to say something similar. Have you considered trialling this with a fiscal sponsor (like Rethink Charity if they’re up for storing money, or Survival and Flourishing’s fiscal sponsor if you can get a grant through them?)

Sounds right. There's a lot to learn about the incentives behind this kind of initiative, but I'm excited about it (I argued for some similar initiatives a couple of years ago)