Although ESG may not be as "buzz-worthy" as it was a few years ago - and some folks will say one can never trust corporate America anyway, there could be some merit to the idea expressed (in the same vain as a given company being lobbied by a shareholder to consider use of cryptocurrency - or stablecoin - as an alternative to U.S. Dollar holdings for its treasury); perhaps there is some way to further refine the idea, such that it behooves a given foundation (and the staff who know its finances best) to at least study the matter?

(Regardless thereof, kudos for sharing a quick read & interesting read!)

Although I’ve referred to there being approximately 1 OOM more capital invested than granted in any one year, there’s some nuance – of the granted funds, all of them are in fact being allocated in that year (by definition); whereas of the invested funds, some of the assets may well have allocated to impact funds some years ago.

This could be 1 OOM effect, if you invest for 10 years, so that's pretty important.

Although 90% (or whatever) of your assets could be invested in impact investing funds, you probably won’t allocate all of your assets to impact investments. For example, you will probably want to hold some of your capital in listed equities, and you might consider it too hard to find effective impact investments in that asset class.

If you do a significant fraction, it's pretty easy to reduce your overall return significantly (if you are trying to maximize returns), which really cuts into your charitable impact. So overall, it doesn't look very promising to me.

A foundation’s investments could do as much good as its grants, potentially

This is a crosspost from the new Animal Welfare Alignment Newsletter by Anima International. You can subscribe on Substack if you are interested in following these efforts. Audio reading also available on Substack.

The goals of this post are to:

1. Raise a question I see as crucially important to the goal of aligning AI to animal welfare...

I used AI to fix transcription errors, rerrarange the ideas, and suggest tweaks to the title and some sentences.

Three of the most exciting projects to come out of EA in recent years are, in a vague sense, CEA spinouts:

* Kairos is directly a spinout of CEA and now handles most support for university AI safety groups. Basically everyone I've found who knows them is really excited about what they do

* NEST is an opinionated ideas-fi...

Hello! I'm Justin Portela. I got hired by GWWC to make YouTube videos after AI in Context did such a kickass job.

My channel is using that same cinematic, high-production value beauty to talk about everything in the EA universe that isn't AI.

...

I used an LLM to help draft this post and create images; I’ve rewritten it extensively and endorse it.

Exec summary

I think foundations should put more effort into having impact through their investments (confidence: high). I more tentatively think that doing so could lead them to have as much impact again as they have through their grants (confidence: lower).

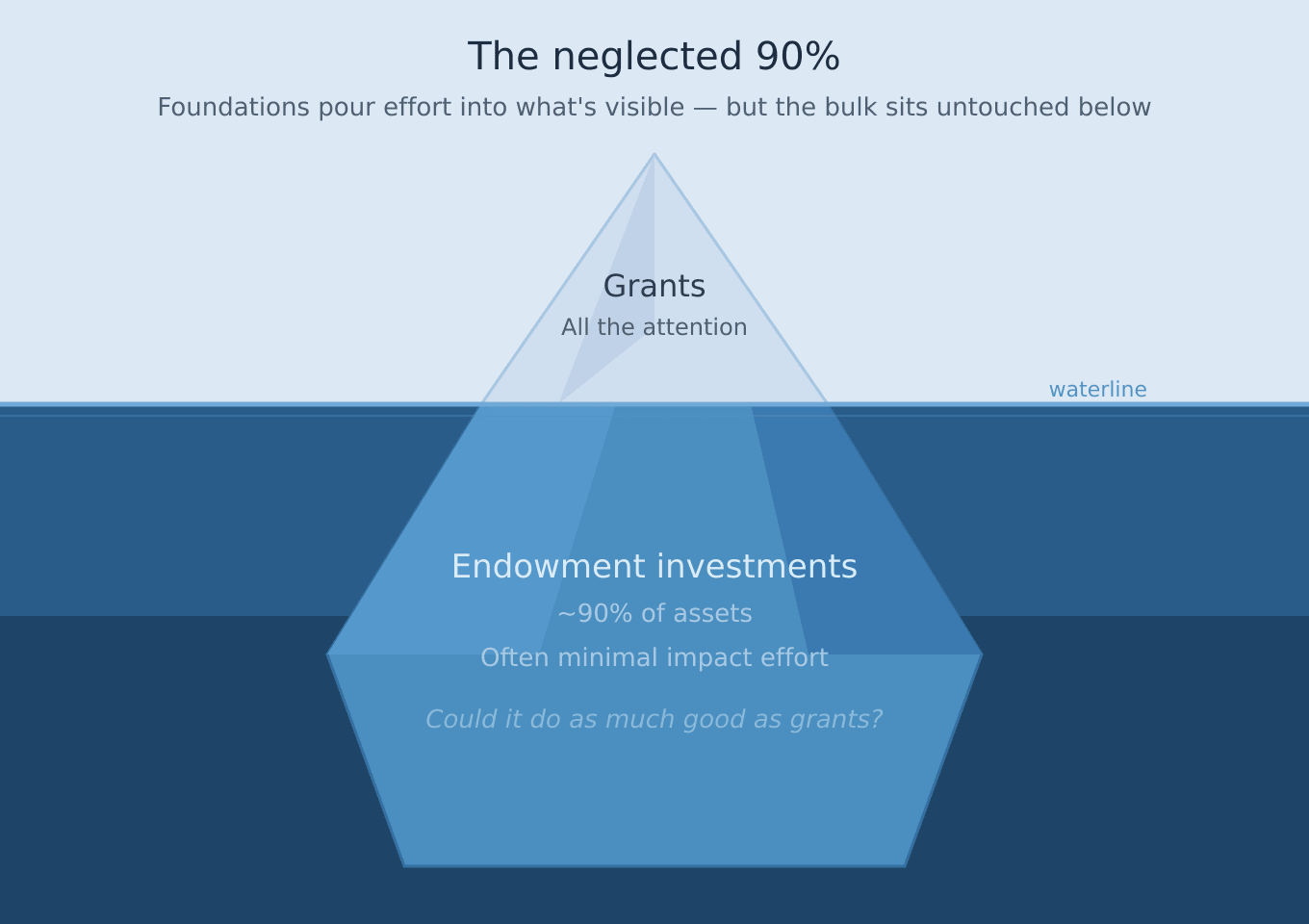

Foundations expend a lot of effort on making effective grants. And rightly so. But imagine a foundation that grants out 10% of its assets in a given year. That means 90% of its assets are being invested; most foundations give little or no thought to whether those investments are having a positive impact on the world.

Put another way: foundations allocate something close to 100% of their "impact effort" – the time and resource they put into converting assets into impact – to grantmaking, and close to 0% to impact investing. The 0% allocation of effort is the correct allocation if there is literally zero scope to have positive impact as an investor.

I'll make two claims.

First, that impact investing can achieve better than zero impact – I'm pretty confident that this is true, even if you don’t want to concede on investment returns.

Second, and with less confidence, that the best impact investing opportunities can come within one order of magnitude (OOM) of the best grants. If true, that implies the "50/50 claim": that half the impact that foundations can have comes from investing, and the other half from donating.

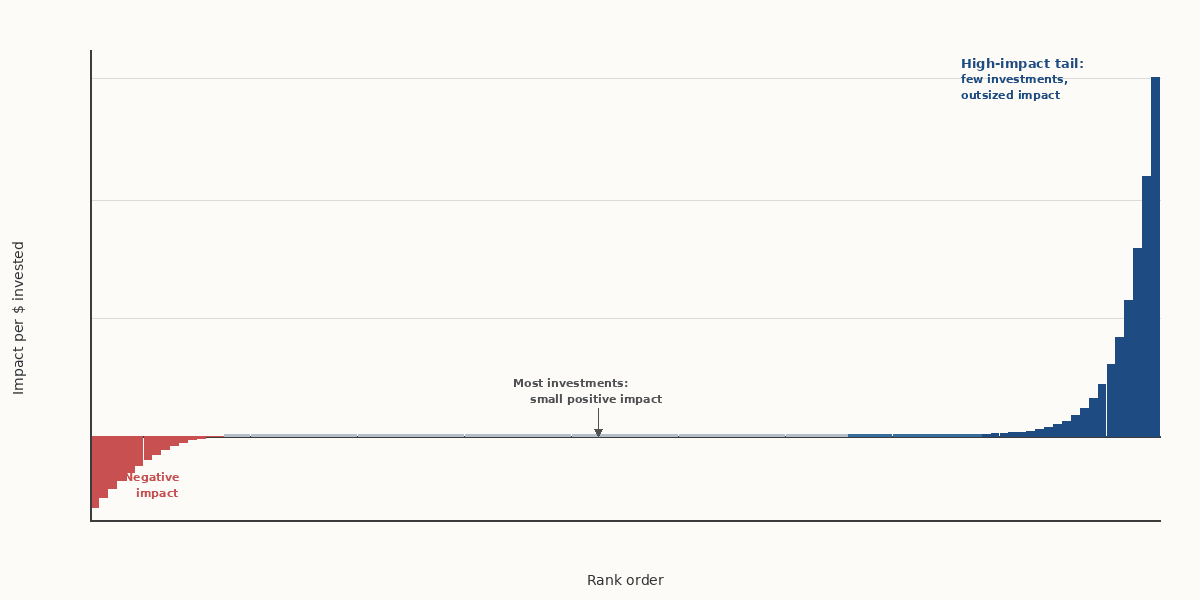

My first claim is, to my mind, a very weak claim, and likely to be correct. However, I think many still need to be convinced on this so I'm going to argue that investments follow a Pareto/fat tailed distribution in the amount of impact they have (just as donations do). Just because most investments are low impact doesn't mean we should throw the baby out with the bath water. Instead, we should focus our efforts on finding the minority of investments which have a much higher impact.

As for the second claim, I’ll argue based on some examples. The level of modelling that I've done is quite light touch, so check out the caveats below to see how much you’re swayed. If the modelling is what stands between a foundation and taking action, please tell me. That might motivate me to do it more rigorously.

I’ll briefly discuss the (often legitimate) concern that there’s no easy way to do impact investing for the cause areas you consider most important. I don't think this is a reason to give up.

Although this article mostly focuses on how you can find impact as an allocator to capital, investors can also have impact through stewardship, including policy advocacy. This means: as an investor you have influence, so a good steward will use that influence for good. For brevity, I’ve not covered that point, but it’s part of what I think a foundation should do.

Impact investing also follows a Pareto distribution

I believe that if you take all the possible investment opportunities, and quantify the impact of all of them, the distribution will be fat tailed / Pareto.

If you restrict to impact investments (i.e. those labelled as impact investments by asset managers) it won’t change the fat-tailed nature of the distribution much, because most people in the impact investing world are not actively considering impact per $ invested. I would expect the amount of the investments which are net negative to reduce, because impact investing funds do screen out harmful investments quite a lot.

I have two reasons for thinking it's fat-tailed:

This is the default distribution for contexts where nothing constrains the distribution to be within a small number of ooms of each other

I've seen lots of examples of impact investments through my work; sometimes I produce quick Fermi estimates of the amount of impact, and those examples seem to support the fat tailed distribution

Pareto is the unconstrained default

For brevity, I won't dwell on this. The essence of the argument is that there is no "impact market efficiency" - nothing which somehow constrains all of the impact to be within a small number of OOMs of each other. In the absence of those forces, there is no reason to believe that impact can't be many orders of magnitude apart from each other. There's also a few other arguments which are outlined in this earlier short article.

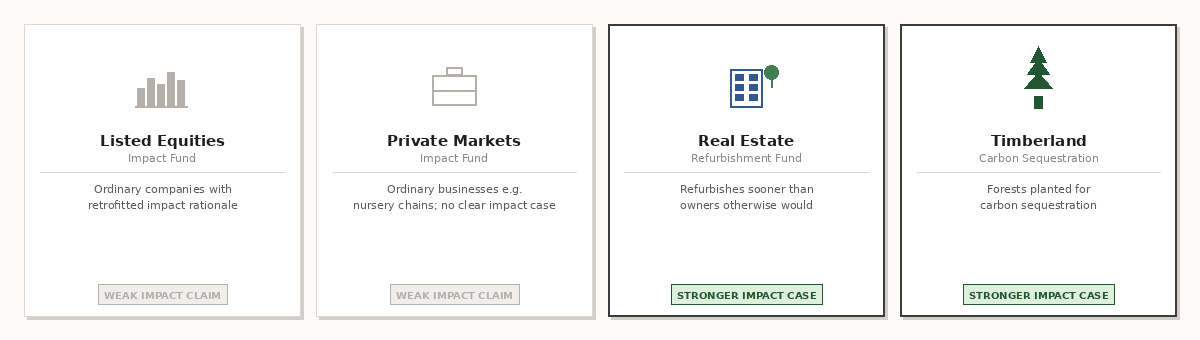

As for the second point, here are four stylised examples inspired by real impact funds I've encountered in the market.

Examples: Four funds

The first is a listed equities impact fund. If you look through the underlying holdings, the companies look fairly ordinary – the kind of businesses you'd find in any diversified equity portfolio. The asset manager has a rationale for each one being "impactful," but in most cases the justification amounts to something like: this company provides a service its customers value. That's true of almost every company that survives in a competitive market. It's not a meaningful impact claim.

The second is a private markets fund investing in fairly standard targets. The investments look much like what any private markets manager has been doing for decades. One holding, for example, is a chain of nurseries — not a specialised provider serving low-income families or underserved communities, just an ordinary nursery chain of the kind my daughter attends. Again, the impact framing feels retrofitted onto investments that would have been made anyway.

The third is a real estate fund that acquires office buildings not in need of refurbishment and refurbishes them anyway — specifically to improve energy efficiency and air quality. This is more unusual. Most real estate owners are deterred from early refurbishment by the time value of money: incurring a cost years before you have to is financially suboptimal. This fund absorbs that cost deliberately. There is potential upside: better energy efficiency reduces tenants' operating costs, which supports higher rents. The strategy also attracts high-quality tenants with their own net zero commitments. There's also a health benefit from improved ventilation — healthier staff are more productive — though this tends not to move facilities teams as much as it probably should. The claim to counterfactual impact is stronger: most office owners don't do this, so the fund is causing something that wouldn't otherwise happen.

The fourth is a timberland fund — investing in forests for carbon sequestration. The impact complexity here is worth briefly acknowledging: forestry approaches optimised for rapid carbon sequestration can damage ecology; trees have complicated effects on the water cycle; and there are biophysical effects alongside the biogeochemical ones (trees can reduce albedo in ways that have a warming effect, and arguably even a net warming effect). The best funds in this space have grappled with these issues seriously, and I'll assume we're looking at that end of the market.

The first two funds have weak impact cases. (I still believe that some positive impact is achieved with those, just that the amount of impact is very small). The last two have better cases. Now consider: between the real estate fund and the timberland fund, which has more impact per dollar?

The answer, measured by carbon sequestered or emissions averted, is timberland. Land used for forestry is orders of magnitude cheaper than prime office real estate, which among other factors produces a cost-effectiveness difference of at least 100x. This is the Pareto distribution in action. Both funds have a real impact claim. One is dramatically more impactful than the other.

Is impact investing really within one OOM of donating?

If it is within one OOM, then a foundation is investing around one OOM more than it's donating in a year, and the investments may have no more than one OOM less impact, so those effects roughly cancel each other out. Which suggests that the foundation could be missing out on half its impact. There's a few nuances, which I discuss in the section about the 50/50 claim.

Here are two examples where I've tried to model it, however roughly. Instead of sharing full models, I will, for brevity, highlight the key features of the models which help to explain why the numbers come out favourably.

Timberland. When I compare the cost per tonne of carbon sequestered via a timberland fund against the cost of achieving a similar outcome through donation, the numbers are surprisingly close. The typical concern about impact investing is about counterfactuals (that your capital isn't truly additional, because someone else would have provided it anyway). That doesn't necessarily apply here. The constraint on more carbon-sequestering forestry can, in some cases, simply be capital: there's enough land, there are enough operators, they just need funding. More capital genuinely means more trees. I've found it hard to get evidence I fully trust, and the additionality argument doesn't apply uniformly across all timberland investments. But at least some of the time, it does seem to hold.

Pharma. A fund invests in small, early-stage pharmaceutical companies — often spin-outs from large pharma — operating in jurisdictions where capital for drug development is scarce. The fund provides not just capital but specialist expertise, including support navigating the FDA approval process. Sometimes the companies are founded by scientists who are technically excellent but have little experience with regulatory pathways — that was handled by colleagues at their former employer. The fund can potentially accelerate the approval timeline by months or in some cases years. It also selects investments partly on the basis of the drug's health impact, although this might not make a huge amount of difference because impactful drugs also tend to have better market prospects.

When I model this in terms of life-saved equivalent per dollar, it comes out within one order of magnitude of a GiveWell-recommended charity. This isn't invoking anything about it being an investment, therefore you get the money back to do more good later - it's just looking at amount of health improvement caused per unit capital deployed. The assumptions doing the most work are:

First, that when the fund claims favourable counterfactuals (allocating capital in areas where pharmaceutical funding is scarce) I discount this only moderately rather than heavily. The reasons for limited scepticism are that there's a commercial incentive to find neglected areas, and that pharmaceutical expertise creates a real moat that limits competition.

Second, I apply somewhat less scepticism to the later steps in the theory of change than I would for a philanthropically-funded intervention. The reason is that for-profit healthcare, unlike philanthropy, has a direct feedback loop between outcome and revenue – imperfect given the asymmetry of knowledge between providers and patients, but partially corrected by regulation. FDA approval itself is a meaningful filter for both efficacy and safety.

A belief that someone more experienced can help a company get through the FDA process about 6 months to a year more quickly also does quite a lot of work. (Also that the process just removes time-wasting mistakes, as opposed to corrupting the regulatory process by helping ineffective drugs get approved)

I think my models are probably not bad. But it would take me a bit of time to tidy them up enough to publish them, and I can't rule out that writing them up carefully would shift the conclusions somewhat, though I'd expect them to hold within a small number of OOMs.

Cause areas

There is now a reasonable ecosystem of impact funds focused on climate and environment, and a smaller but meaningful set addressing housing and other social issues. For foundations whose priorities sit in these areas, the market offers options worth exploring.

If your interests are animal welfare, there aren’t many obvious options, but the investment community is doing quite a bit about AMR (anti-microbial resistance) and a lot on climate and nature loss. Some of those outcomes overlap with things that animal advocates would care about. I haven’t seen any AMR funds - it’s normally one of several priorities, and quite often it’s a topic that investors engage on (i.e. a stewardship thing) rather than an impact that’s achieved by allocating capital.

For foundations focused on AI safety or pandemic preparedness, on the other hand, the picture is more disappointing. From what I've seen of the institutional investment market, impact funds in these areas are essentially nonexistent. This is a gap – but it's also an opportunity, because foundations don't have to be passive consumers of whatever the market happens to offer. They can be market makers, not just market takers.

A foundation that seeds an AI safety or pandemic preparedness fund does more than deploy its own capital. Once an asset manager has built such a fund, they have a commercial incentive to raise further capital from other asset owners. The asset manager becomes an evangelist for the cause – going out to other institutional investors and making the case that these are important areas deserving of capital. The foundation's seed investment catalyses a much larger flow of both money and attention.

What might such funds invest in? For AI safety, one could imagine building out the ecosystem of companies that audit and evaluate models for safety and alignment – infrastructure that needs to exist and is currently very underprovided. For pandemic preparedness, possibilities include companies improving air quality in the built environment, businesses working on metagenomic sequencing, or services helping airports and other high-traffic environments monitor for early signs of pathogen risk. A real estate fund applying the refurbishment model described above, but with a focus on clean air rather than carbon, would fit naturally in this category.

A note on the 50/50 claim

I said earlier that if the amount of impact from impact investing is within one OOM, then a foundation is investing around one OOM more than it's donating in a year, and the investments may have no more than one OOM less impact, so those effects roughly cancel each other out. I suggested that the foundation could be missing out on half of its potential impact - this is the 50/50 claim.

This glosses over a few considerations:

Although 90% (or whatever) of your assets could be invested in impact investing funds, you probably won’t allocate all of your assets to impact investments. For example, you will probably want to hold some of your capital in listed equities, and you might consider it too hard to find effective impact investments in that asset class.

There’s potentially scope to adjust your strategic asset allocation to lean more towards impact-friendly asset classes, but before doing that you would need to think through several considerations that are too nuanced for me to get into here.

Although I do believe that there exist some investments which have great impact without compromising on investment returns, there are some complications. These opportunities are rare.

This leaves you with the choice of being overexposed to a small number of funds (which leaves you with concentration risk) or accepting that only a portion of your portfolio will be in the opportunities that you consider to be best.

Although I’ve referred to there being approximately 1 OOM more capital invested than granted in any one year, there’s some nuance – of the granted funds, all of them are in fact being allocated in that year (by definition); whereas of the invested funds, some of the assets may well have allocated to impact funds some years ago.

These considerations tend to lean more towards allocating less effort to impact investing. I haven’t focused too much on this until now because I’m largely dealing in orders of magnitude, and at the level of crudeness, I don’t think this is going to move the dial a huge amount.

Also, this leaves out the impact from stewardship, which may, potentially, make up for this.

Stewardship and policy influence

Capital allocation is only one of two high-level levers available to foundations. The other is stewardship, which means using your position as an asset owner to influence for positive outcomes. It’s typically interpreted to mean an extension of the standard investor governance actions: voting proxies, filing shareholder resolutions, engaging management. It can include policy influence, which means foundations using their standing as major capital allocators to shape the policy and regulatory environment; the evidence from sovereign bond markets suggests this lever has real teeth. I plan to cover both in follow-up pieces if there's appetite for it.

A final note

The argument here isn't that impact investing is uniformly good or that the market is trustworthy. It's that the same rigour we apply to grantmaking should be applied to the rest of foundation assets – and that doing so carefully will reveal a small number of opportunities with large impact potential. If the modelling above is even roughly right, foundations that ignore this are leaving a significant fraction of their total impact on the table.

If you're a foundation thinking about how to act on any of this, I'd welcome the conversation. Feel free to reach out.

29

More posts like this

316

EA is underfunding animal advocacy according to our own preferences

Although ESG may not be as "buzz-worthy" as it was a few years ago - and some folks will say one can never trust corporate America anyway, there could be some merit to the idea expressed (in the same vain as a given company being lobbied by a shareholder to consider use of cryptocurrency - or stablecoin - as an alternative to U.S. Dollar holdings for its treasury); perhaps there is some way to further refine the idea, such that it behooves a given foundation (and the staff who know its finances best) to at least study the matter?

(Regardless thereof, kudos for sharing a quick read & interesting read!)