Comments

I realise this is not actually what the spirt of the post is about, but: Some people have asked me to consider going back to earning-to-give -- why is that? Seems like you have quite a bit of impact working at METR.

I realise this is not actually what the spirt of the post is about, but: Some people have asked me to consider going back to earning-to-give -- why is that? Seems like you have quite a bit of impact working at METR.

Thanks for the post. Of your caveats, I'd guess 4(d) is the most important:

Generative AI is very rapidly progressing. It seems plausible that technologies good enough to move the needle on company valuations were only developed, say, six months ago, in which case it would be too early to see any results.

Personally, things have felt very different since o3 (April) and, for coding, the Claude 4 series (May).

Anthropic's run-rate revenue went from $1B in January to $5B in August.

This post misquotes Garry Tan. You wrote (my emphasis):

Y Combinator CEO Garry Tan has publicly stated that recent YC batches are the fastest growing in their history because of generative AI.

But Garry's claim was only about the winter 2025 batch. From the passage you cited:

The winter 2025 batch of YC companies in aggregate grew 10% per week, he said.

“It’s not just the number one or two companies -- the whole batch is growing 10% week on week”

He's been saying the same thing for a while. E.g. here:

back in the day when we were working with companies you know what was sort of a aspirational growth rate what would we tell people to try to do week on week. Well 10% week on week is is an amazing metric to hit yeah and I think back then if uh you were like maybe the top one or two you know maybe even the top one or two companies in the whole batch you'd be able to achieve that. And since summer of last year the wildest thing is realizing that uh both summer and fall [2024] batch in aggregate on average over the batch in 12 weeks average 10% week on week growth so not just the very best the Airbnb of the batch but the batch overall

I will add this as a footnote to clarify though, thanks for pointing it out!

Cool, thanks. With that source, I agree it's correct to say that Garry Tan has claimed that "YC batches are the fastest growing in their history because of generative AI" for the summer 2024, autumn 2024 and winter 2025 batches.

Have you noticed him making a similar claim for earlier batches?

Not to my knowledge. I agree with your point that maybe it's just too soon to see any results (this is why I put "yet" in the title).

I've been trying to think about what a good prediction market for this post would be, because I'd like to get some signal on whether this is the explanation - any thoughts? Maybe something like "if I run this exact same analysis one year from now, will at least two 2024 batch companies be on the list of 20 fastest 2-year growth YC startups?"

I've no experience writing questions for prediction markets. With that caveat: something like that question sounds good.

Ideally I'd like to see the 1-year analysis run in 2026Q1.

Notably, in that video, Garry is quite careful and deliberate with his phrasing. It doesn't come across as a case of him doing excited offhand hype. Paul Buchheit nods as he makes the claim.

Thanks for the interesting post!

I do think you have a mistake, though: Wiz is not a GenAI company. They do vanilla cloud cybersecurity. IIRC they started seriously recruiting for their ML team only in 2023, when it was already a decacorn.

Executive summary: Despite hype, preliminary analysis suggests that generative AI has not yet led Y Combinator startups to grow faster in terms of valuations, though measurement issues, macroeconomic headwinds, and the possibility of delayed effects leave room for uncertainty.

Key points:

This comment was auto-generated by the EA Forum Team. Feel free to point out issues with this summary by replying to the comment, and contact us if you have feedback.

Epistemic status: I think you should interpret this as roughly something like “GenAI is not so powerful that it shows up in the most obvious way of analyzing the data, but maybe if someone did a more careful analysis which controlled for e.g. macroeconomic trends they would find that GenAI is indeed causing faster growth.”

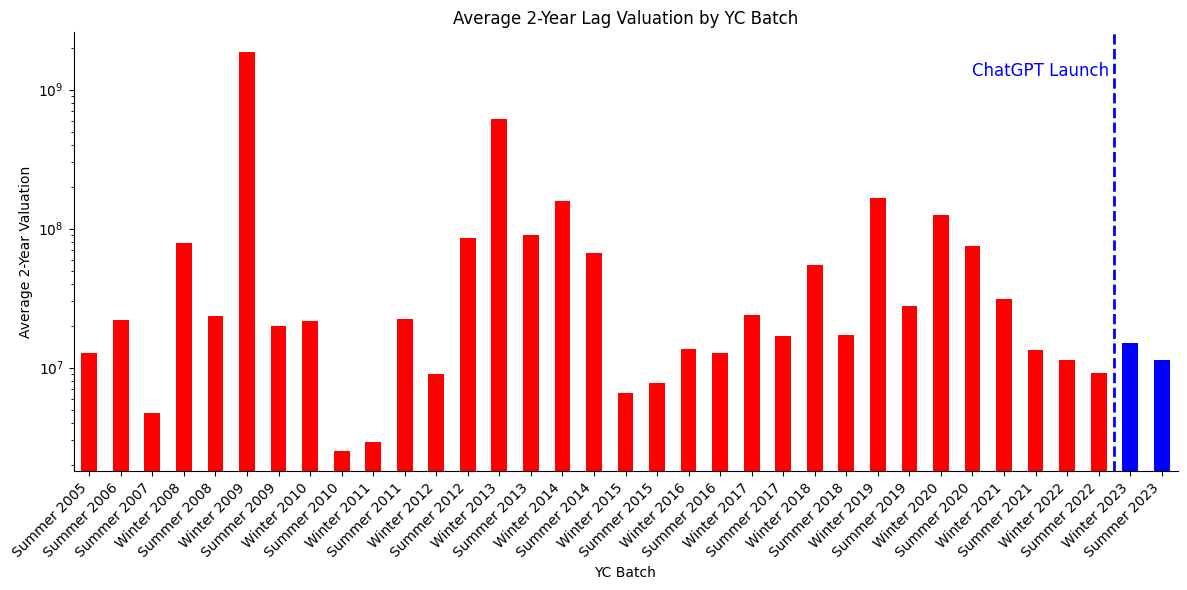

Of the 20 companies which had the highest 2 year growth post-YC, only 1 (Tennr) was a 2023+ batch company, even though 16% of the companies I could find 2 year growth data for were 2023+.[1] The average valuation of a YCombinator company two years after it goes through YC is only $13.3M for 2023+ batches, compared to $46.1M for <2023 batches.[2]

“YC-backed” is sometimes used as a synonym for “good startup,” but the most talked-about GenAI startups (Anthropic, Cursor, etc.) aren’t YC-backed.[3] It's possible that YCombinator startups have secularly become worse, and this effect overshadows any increase from generative AI.

All code and data can be found here.

I scraped a list of all YC-backed companies from here. I then asked Claude Haiku 3.5 (with a web search tool) to identify the valuations of each company annually after it went through YC.

Valuation numbers were adjusted using the cpi python package to be in June 2025 dollars.

I then randomly sampled results to confirm that the extracted valuations were correct. I particularly manually verified the list of the top 20 1- and 2-year growth companies.

It is hard to know for sure how much a company is using GenAI. It seems safe to assume that most YC companies were not using it much before the launch of ChatGPT (if only because the technology wasn’t available), and somewhat reasonable to assume that companies were mostly using it afterward (because YC pivoted very hard into GenAI startups).

I therefore use being before or after the launch of ChatGPT as a proxy for using GenAI. This is not an ideal identification mechanism for obvious reasons but I think it’s a reasonable proxy. Importantly, Garry Tan talks about “the whole batch” growing, not “the GenAI startups in the batch”.

I expect there are two major sources of error in this project.

These sources of errors tend to more heavily affect the results for the average statistics and don't affect the estimates of the top companies as much. I therefore would suggest believing the top 20 lists more than the information about the average statistics.

| Company | Batch | Valuation (2025 $) |

| Deel | Winter 2019 | $6.5B |

| Zenefits | Winter 2013 | $6.1B |

| Whatnot | Winter 2020 | $4.0B |

| Jeeves | Summer 2020 | $2.3B |

| Airbnb | Winter 2009 | $1.9B |

| Prometheus | Winter 2019 | $1.8B |

| Airbyte | Winter 2020 | $1.6B |

| Yassir | Winter 2020 | $1.1B |

| AtoB | Summer 2020 | $870.9M |

| QuickNode | Winter 2021 | $845.8M |

| DoorDash | Summer 2013 | $804.2M |

| Cruise | Winter 2014 | $669.2M |

| Vouch | Summer 2019 | $653.0M |

| Newfront | Winter 2018 | $625.6M |

| Tennr | Winter 2023 | $605.0M |

| Ginkgo Bioworks | Summer 2014 | $602.2M |

| Flexport | Winter 2014 | $488.5M |

| Instacart | Summer 2012 | $479.1M |

| Postscript | Winter 2019 | $474.9M |

| Observe.AI | Winter 2018 | $380.4M |

Tennr is the only 2023+ company on this list.

| Company | Batch | Valuation (2025 $) |

| Whatnot | Winter 2020 | $1.8B |

| Airbyte | Winter 2020 | $1.8B |

| AtoB | Summer 2020 | $870.9M |

| Teespring | Winter 2013 | $832.3M |

| Zenefits | Winter 2013 | $676.7M |

| Legora (formerly Leya) | Winter 2024 | $675.0M |

| Cruise | Winter 2014 | $669.2M |

| Newfront | Winter 2018 | $625.6M |

| Jeeves | Summer 2020 | $593.6M |

| PostHog | Winter 2020 | $534.2M |

| Postscript | Winter 2019 | $474.9M |

| Observe.AI | Winter 2018 | $380.4M |

| Khatabook | Summer 2018 | $346.3M |

| Heroku | Winter 2008 | $313.7M |

| SFA Therapeutics | Summer 2021 | $272.1M |

| QuickNode | Winter 2021 | $272.1M |

| Ginkgo Bioworks | Summer 2014 | $270.3M |

| Vouch | Summer 2019 | $264.5M |

| Tractian | Winter 2021 | $223.2M |

| Moonshot Brands | Winter 2021 | $195.9M |

Legora is the only 2023+ company on this list.

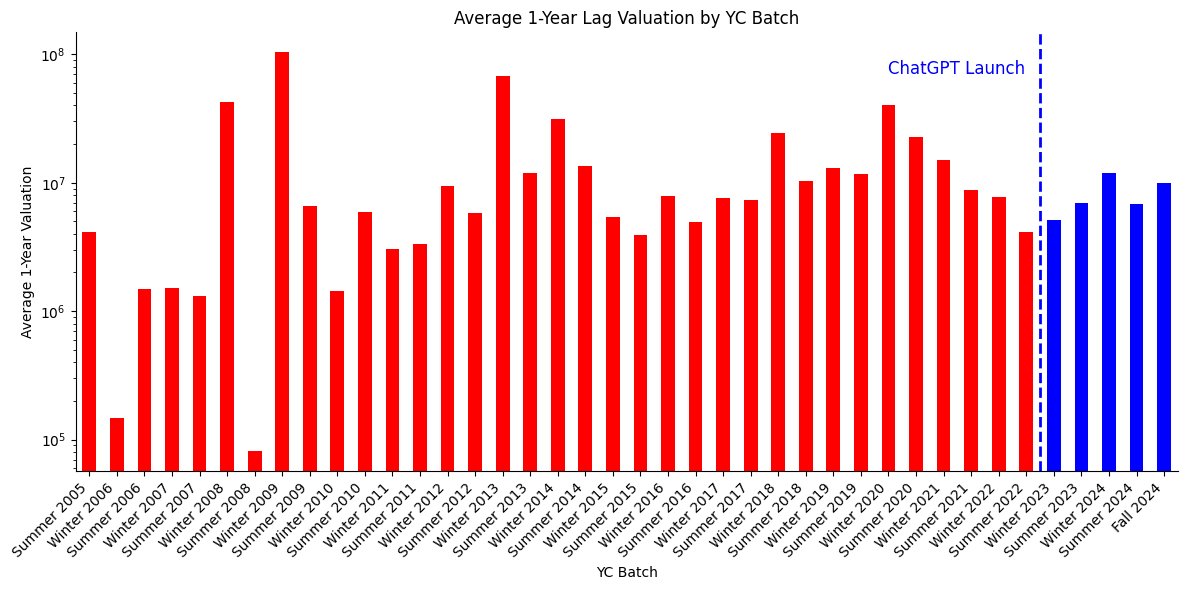

The fastest growing YC batch of all time was Winter 2009. This is because it was a small batch (16 companies), one of which was Airbnb.

YC has shifted to having much larger batches (Summer 2025 was 159 companies, 10x W09). This brings down the average, and I’m not sure one should read that much into the average statistics, but I will include them for completeness.

Y Combinator CEO Garry Tan told CNBC that this group is growing significantly faster than past cohorts and with actual revenue. The winter 2025 batch of YC companies in aggregate grew 10% per week, he said.

“It’s not just the number one or two companies -- the whole batch is growing 10% week on week,” said Tan, who is also a Y Combinator alum. “That’s never happened before in early-stage venture.”

He's repeated this point in previous interviews, e.g. saying that both Summer and Fall 2024 batches grew 10% week-on-week on average.

Tan does not say what metric he is using to measure startup growth, and the cynical reader may suspect if he was using a real metric like “revenue” he would have said so instead of leaving it unspecified. (My understanding is that YC requires companies to report some metric weekly, and this is probably what he is referring to, although it's unclear.)

If Garry or someone else from YC is reading this, I would value more insight into what exactly has been growing 10% week on week.

I do think that there is a meaningful sense in which Y Combinator startups are just not the right reference class for someone who is thinking about generative AI startups. My mental brainstorm of the most valuable GenAI startups turns up mostly companies which are not YC-backed (Anthropic, OpenAI, Cursor, Harvey, Windsurf, etc.).

My guess of the YC companies which have benefitted the most from the GenAI boom are Scale AI (S16) and Replit (W18). This seems consistent with the view that AI will make a lot of valuable companies, but they will still take 10+ years to exit.

The only two post-ChatGPT companies on the top-20 lists are both GenAI companies (Tennr and Legora). This is consistent with a view that GenAI startups are doing well and it’s just that YCombinator startups as a reference class are doing worse.

I therefore do think that these results are not as broadly applicable as they might seem. That being said, it's also hard for me to find examples of quick billion-dollar AI exits outside of YCombinator. Cursor, for example, was almost an example of a company that got acquired for billions of dollars after only two years after being founded, but didn't quite make it. So I would still generally back the claim that we have not seen many $1B+ exits <4 years after founding.[4] [5]

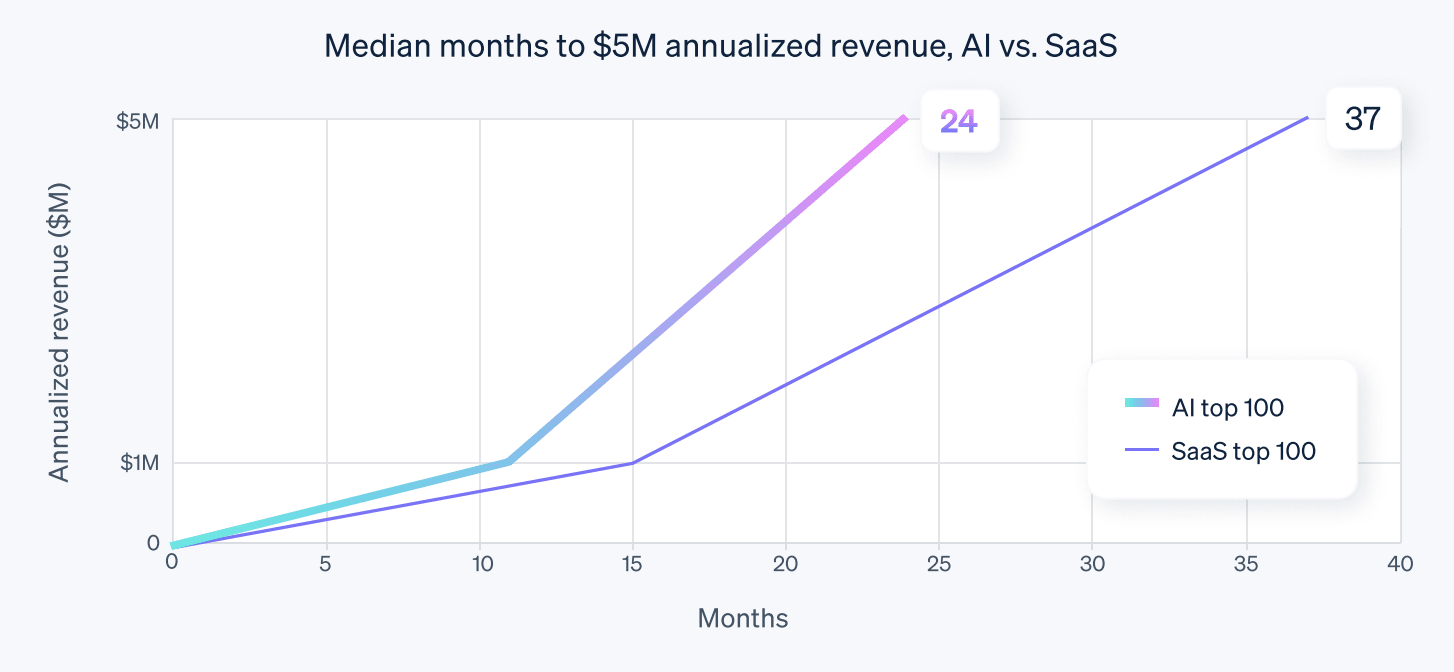

Stripe published this report. A key graph:

There are a couple of possible explanations for why their results disagree with my findings:

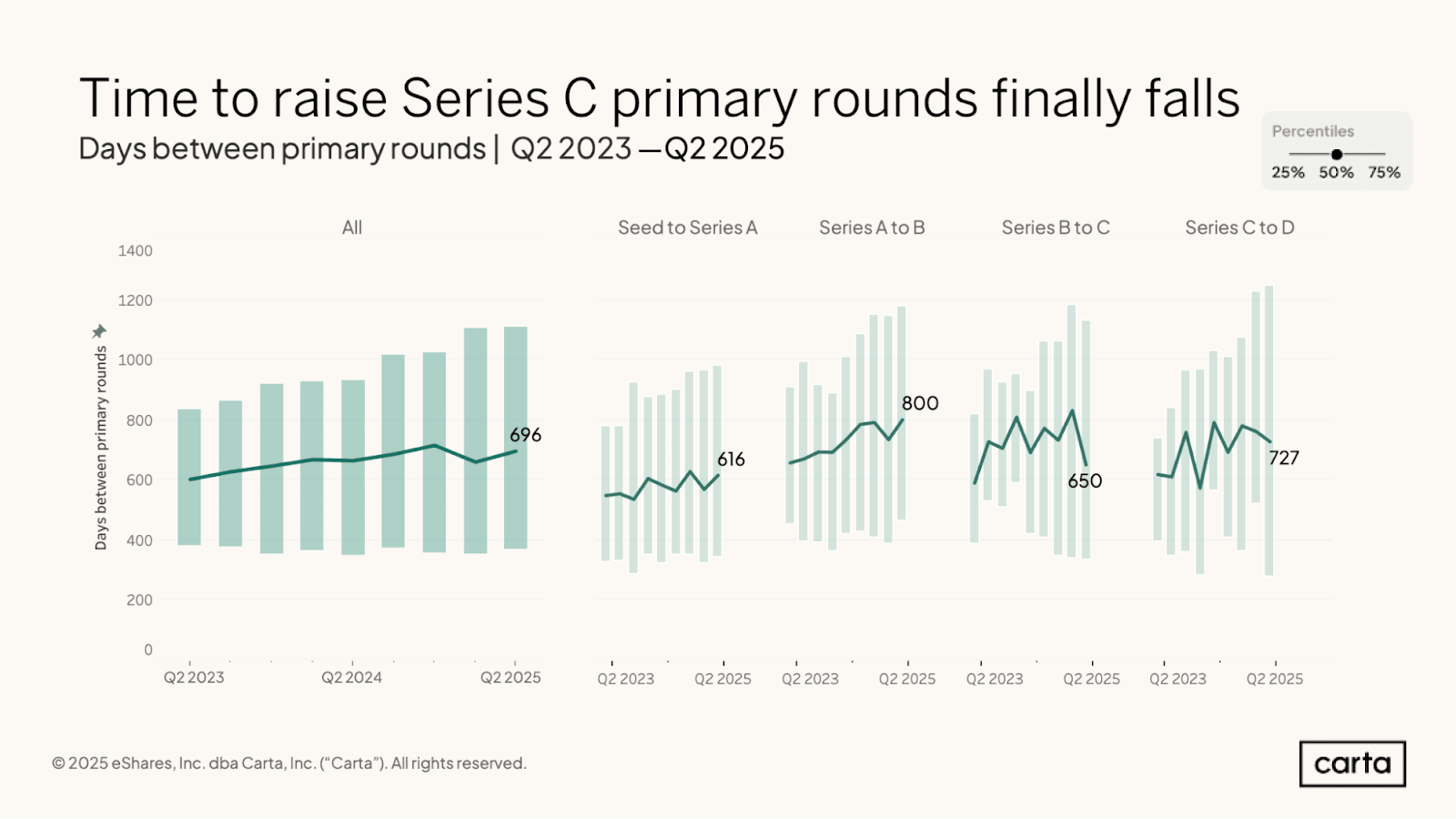

Carta’s Q2 report shows that companies are taking longer to raise initial rounds:

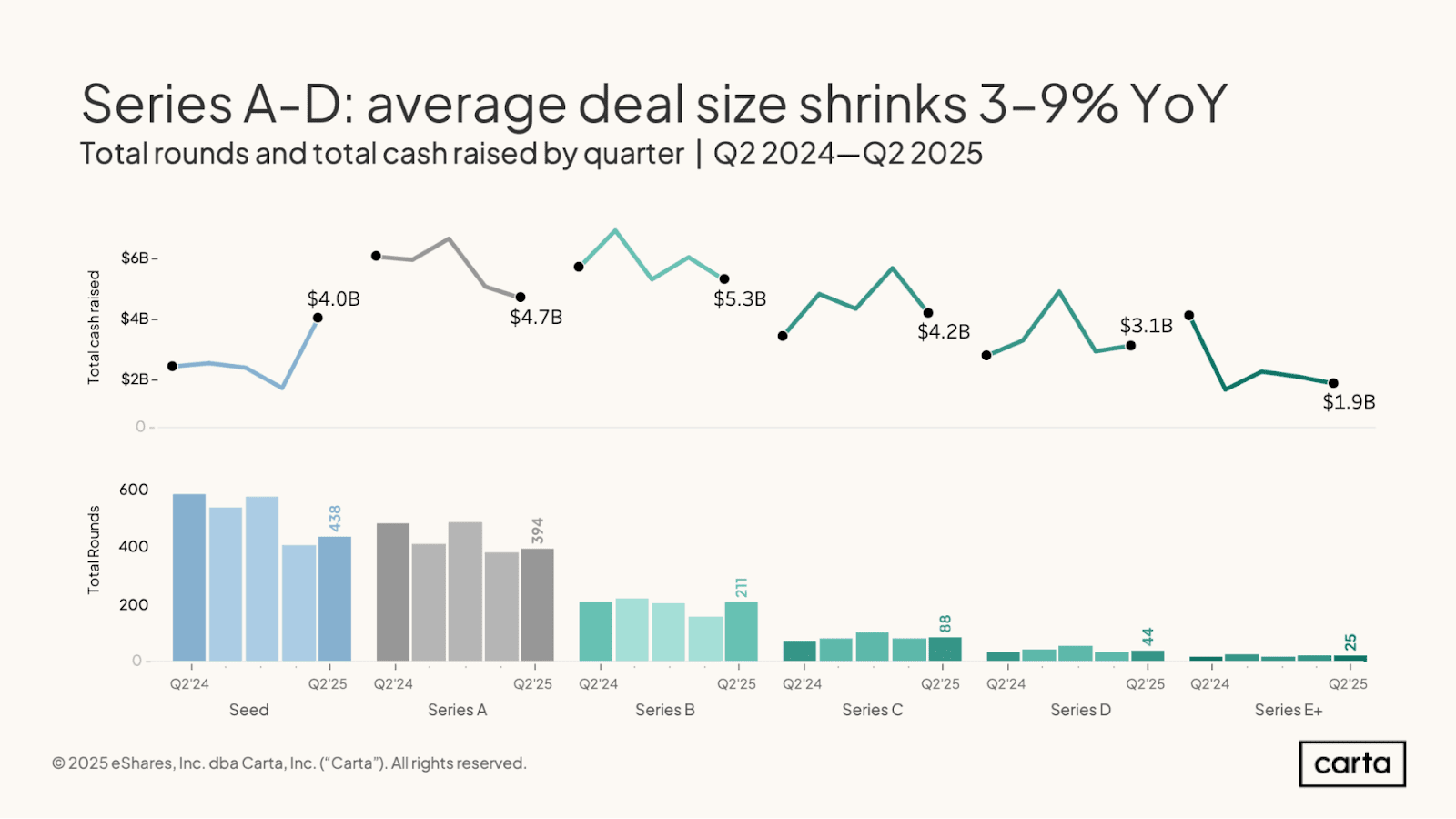

An optimistic interpretation of this would be that companies are able to reach profitability more quickly and therefore don’t need to raise money as aggressively. Unfortunately, if this were true I think we would see that companies valuations are increasing, but Carta actually reports a decrease in average deal size YoY:

The one exception is that average seed round size seems to have increased. My guess is that Q2 just had some outliers, but if this trend holds true in Q3 and Q4 it might indicate a real sustained shift.

Overall, this data seems consistent with the view that startups are not growing more rapidly than they used to be (although Carta’s dataset doesn’t go back very far, is fairly noisy, and is subject to various other caveats[6]).

While generative AI might not make it easier for people to have billion dollar companies quickly after going through Y Combinator, it also probably doesn't make it dramatically harder. My guess is that most entrepreneurs should basically assume that the results for generative AI companies are roughly in line with historical YCombinator software companies and the fact that I found them to be lower is mostly due to noise. (Whether this trend will continue is, of course, more debatable.)

The declining influence of YCombinator is maybe even a positive sign about the strength of AI: maybe AI means that you don't even need to go through YCombinator anymore and that's why the YCombinator companies aren't doing so well (the best AI companies are just successful without YC).

If you are interested in researching this area more, I would be curious to know:

There are a bunch of factors which could explain the relatively sluggish performance of YC startups post-ChatGPT: high interest rates, YC being less attractive, etc. I have made no attempt to control for these and expect that, if I did, the 2023+ startups would perform better.

However, this does mean that even the most favorable interpretation of the data implies that the newer startups have their growth boosted by an amount smaller than the harm caused by factors like interest rates, which means that the benefit is relatively small.

A prediction market about whether next year will show the same results is here.

All dollar figures are in 2025 dollars, unless otherwise stated

I include averages for completeness, but think that changes in e.g. how many companies YC accepts per year make those figures hard to interpret.

Scale AI is, I think, the major exception, but they are perhaps the exception that proves the rule as they were founded in 2016 and attribute their early growth to self-driving cars.

Which is a high bar! But it is one that founders might need their company to meet if they want to exit before their labor gets substantially automated away.

I haven't measured the base rate here at all, so I don't feel very confident that this rate isn't actually higher than it was previously.

Notably their dataset covers all companies, not just GenAI ones.

Hey Ben :)

On 2., this is a kind offer! Is there some way you'd be able and comfortable sharing some of these with participants in CEA's ongoing career bootcamps?

We have a fair few software engineers, current or former C-suite types, etc.

(Or is there some way we could connect individuals with you?)

Thanks!

Probably yes, DMed you