Comments

I should note that a few months ago, I also massively front-loaded my donations such that I have very little in liquid assets. Though I have never met Jeff, him and his family have been an inspiration to me for many years.

I should note that a few months ago, I also massively front-loaded my donations such that I have very little in liquid assets. Though I have never met Jeff, him and his family have been an inspiration to me for many years.

It's very impressive to donate 80%. For other EAs who are pursuing "earn to give" as a main strategy, I think it's a model to learn with. Although the default is to donate 10%, but I think most EAs could aim for a higher value. However, there's also a case for saving money. I think EAs could use "earn to give+save" as a metric, we can aim for "give+save 50% every year"

I'm interested in advice on retirement savings - mine are far smaller than Jeff's and reading this gives me slight anxiety haha. It would be action-guiding for me as maybe I should just not push myself to donate more and instead have a more solid retirement plan. Kudos to you Jeff on being transparent and generous!

Out of curiosity, where did you donate? (apologies if you already have this written up somewhere else!)

The full list is on our donations page. Lately we've been prioritizing political donations (argument, mechanism).

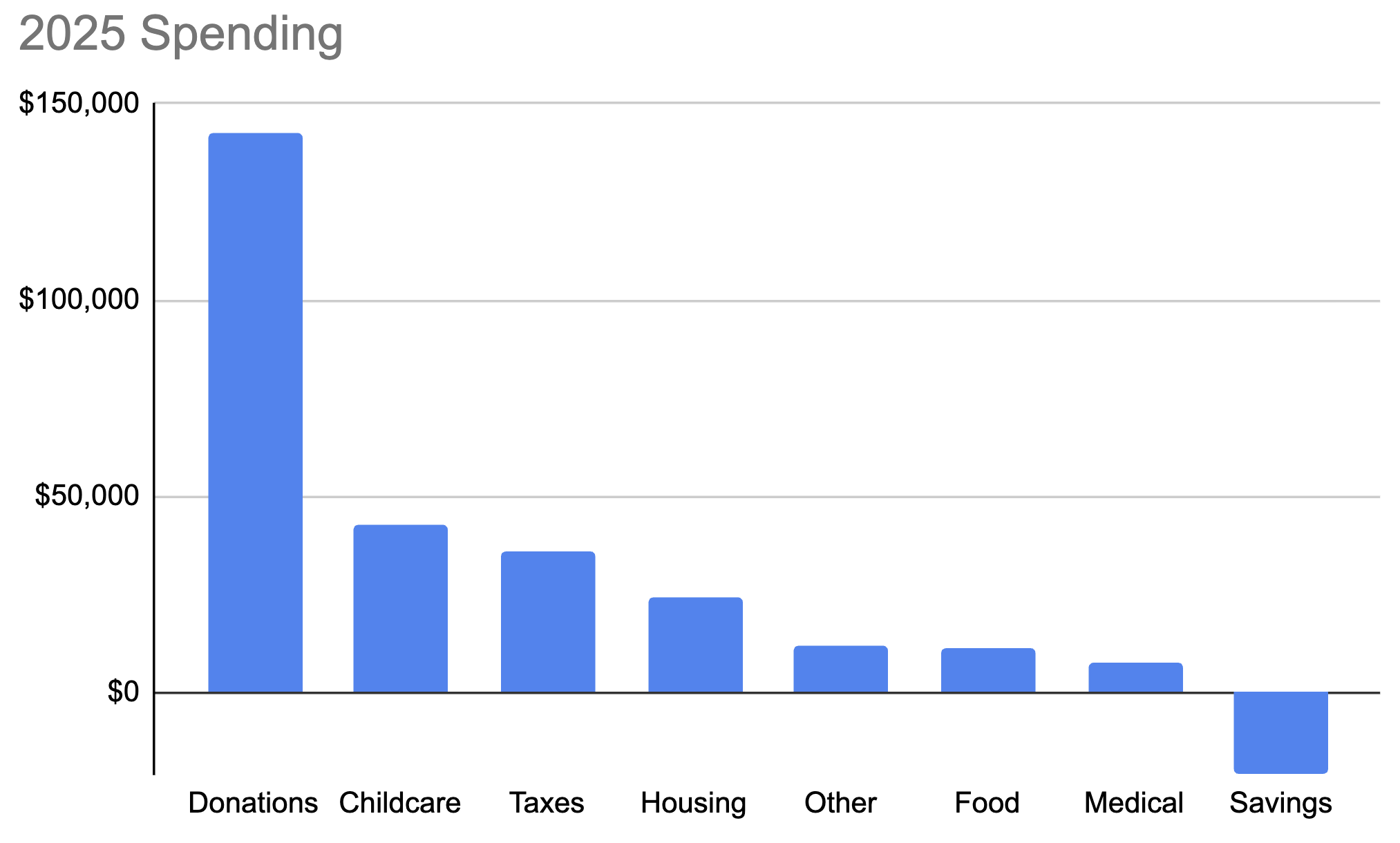

Julia and I had been giving half since 2014, but in 2025 we drew on our savings to donate 81%.

Impressive!

Since we're in a good enough position financially and donating seems very urgent, I now think we should stop contributing to have more to donate going forward...

Even though we're drawing down our savings to donate, our net worth rose 18% over the last year (adjusted for inflation).

Of course returns vary, but if you gave away 80% of your income and your net worth still increased, that means you are close to retirement, so I agree it doesn't make sense to continue to contribute to retirement.

I'd put about 10% on futures where things go very badly, where I'm not here to write a followup and you're not here to read one.

As per your comment on LW, biorisk is a large proportion of the risks in the next 2 years. Are you personally preparing to protect yourself and family from mirror bio or to relocate?

As per your comment on LW, biorisk is a large proportion of the risks in the next 2 years. Are you personally preparing to protect yourself and family from mirror bio or to relocate?

On mirror biology, my impression is the risk there is mostly more than two years out, because it's really very hard. Do you think this specific biorisk is coming sooner?

On relocating, I don't think it would make sense for us to move in response to a bio incident. Instead, I'm more focused on preparations we can take at home.

No, I don't think mirror bio is coming sooner.

I would like to know why you don't think it would make sense to relocate to a place like New Zealand or Australia. My thought is that they demonstrated that they had the will and the functioning government to suppress COVID, and can take advantage of their isolation. You may be able to prevent your family from getting the disease in the US, but then you may have to deal with no electricity or water or fuel if the vital employees are unable or unwilling to show up to work. Australia could likely keep industry functioning conventionally, but even New Zealand might be able to improvise biofuels or go back to animal power.

My top reason for not relocating is that I'm working on preventing this kind of bad outcome, which I think I can do most effectively from Boston.

But even if I were doing work that could be done from anywhere, I don't think I'd relocate: that only helps in a small fraction of the doomy futures, I think there are also a lot of good futures, and I really like living in Boston.

To be clear, my relocation post was for getting ready to relocate quickly in response to a trigger such as a new infectious, fatal disease being discovered.

Thank you for donating and sharing this with the community!

Hi Jeff.

Let's try and make some similar predictions for 2028:

- My odds that the world has changed substantially are up significantly, maybe 55%, primarily due to AI.

Do you see any bet we could make about transformative AI (TAI) timelines, or what they supposedly imply, that is beneficial for both of us?

Useful to see, thanks!

On thinking about the "world got weird because of AI but we are all alive" scenario, I would consider withdrawing from savings to finish paying for the house.

If AI causes something to go terribly wrong on financial systems(lets supose, all banking systems are now easy to hack with AI or something with similar consequences) seems good to not have to prove in legal battles that you actually pais for that % of your own house.

Also, thanks for sharing, I always admired you two very much!

I would be pretty surprised if things failed in that particular way? We do legally own the entire house, and that wouldn't be in dispute. Having money left on the mortgage means that we owe money to the bank, secured by the house. In most kinds of kind of disaster, if ownership becomes unclear, I expect it to be primarily resolved by possession.

I think things are unlikely to fall apart in this particular way, but to the extent that they do, I think it mostly argues for renting over owning, over being an absentee landlord.

I see now. Here in Brazil it works differently. You only own the house after paying full for the bank, before that the bank is the proprietary.

Julia and I had been giving half since 2014, but in 2025 we drew on our savings to donate 81%. It looks to us like we're in a critical window for keeping the introduction of very powerful AI systems from being disastrous, and we want to do what we can while we still can.

Here's what that looks like in the context of our overall spending:

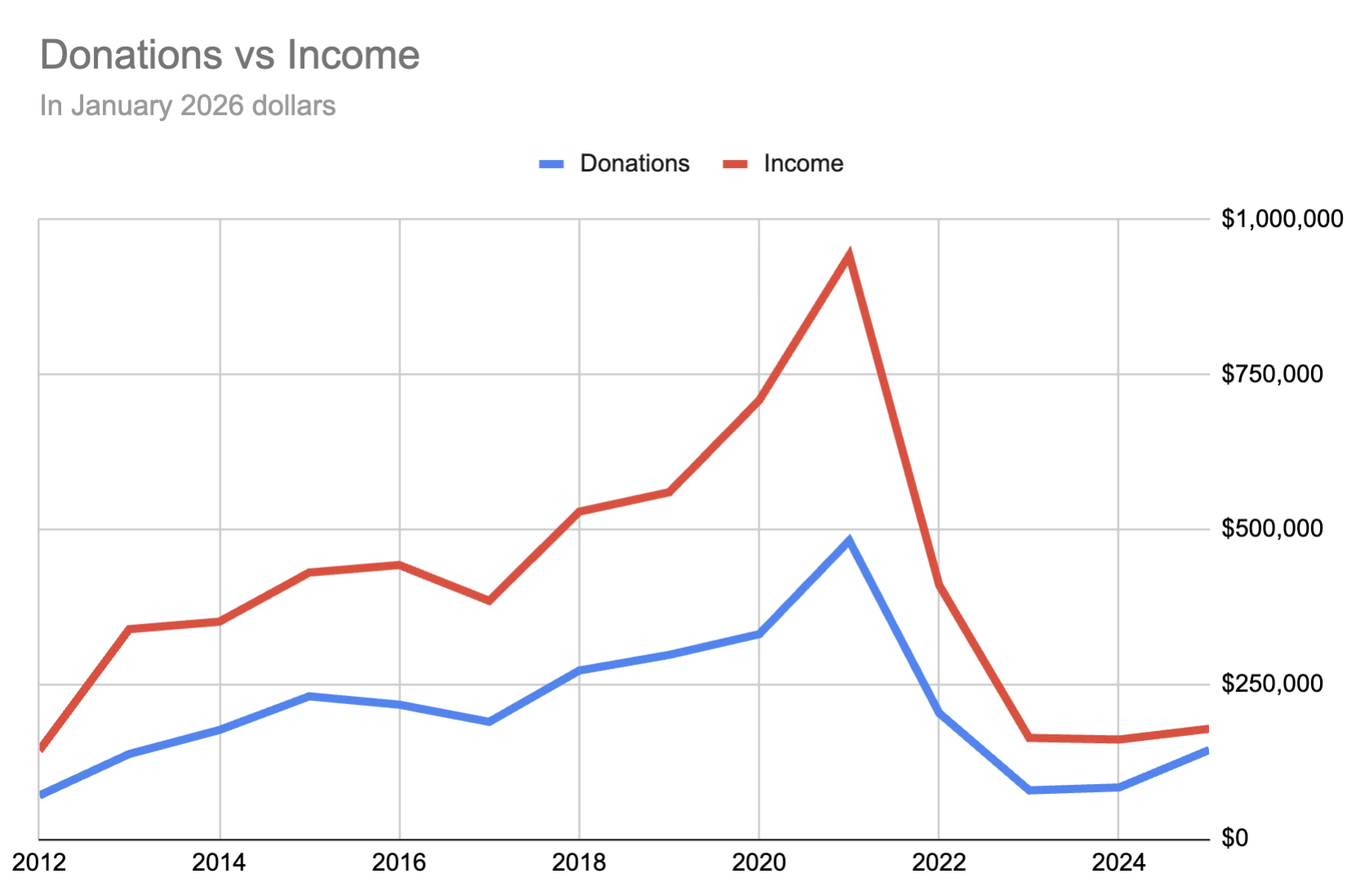

We've been prioritizing donations for a long time, but it feels very different now because of the AI boom. Some of this is that people who've made money in the boom will likely be giving more soon, and so money spent now can help set up organizations to spend future money more effectively. But more importantly, this is a key window of opportunity: transformative AI is coming very quickly, for better or worse. We want to push hard for "better".

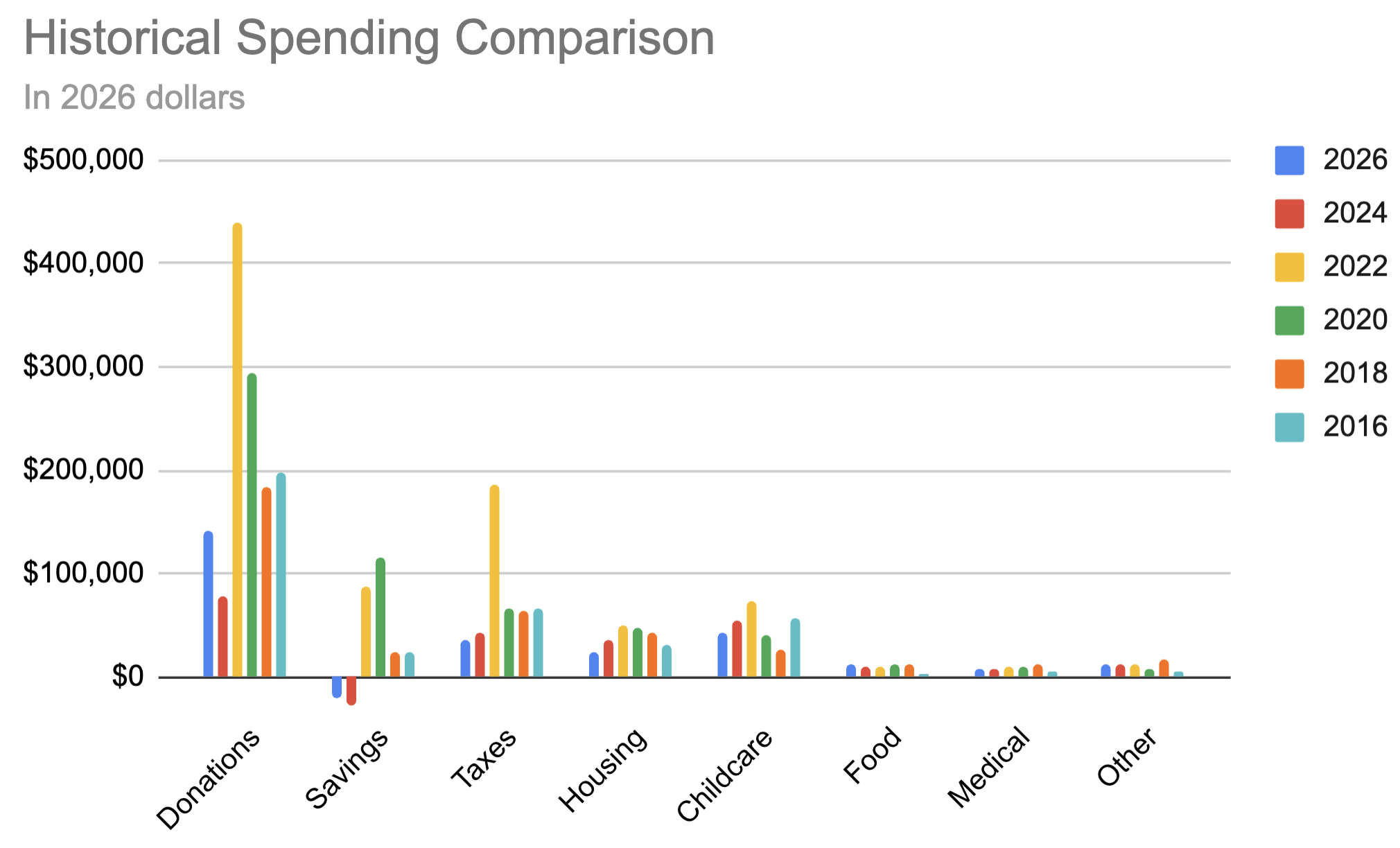

If you compare to previous years (2024, 2022, 2020, 2018, 2016, 2014), we're donating a lot less than we used to in absolute terms:

Until mid-2022 I was working at a big tech company, optimizing to maximize donations, and now I'm at a non-profit. This means we're giving a larger fraction, but of a smaller amount:

I feel good about this change. I'm now building an early warning system for engineered pandemics, which is urgent and important as AI increasingly substitutes for advice from expert virologists. It does mean donating much less than I would have if I'd continued in big tech, but I think this was well worth it. While money can enable important work, I see a lot of projects that primarily need dedicated people to bring them into existence, and I'd be excited for others to switch to direct work.

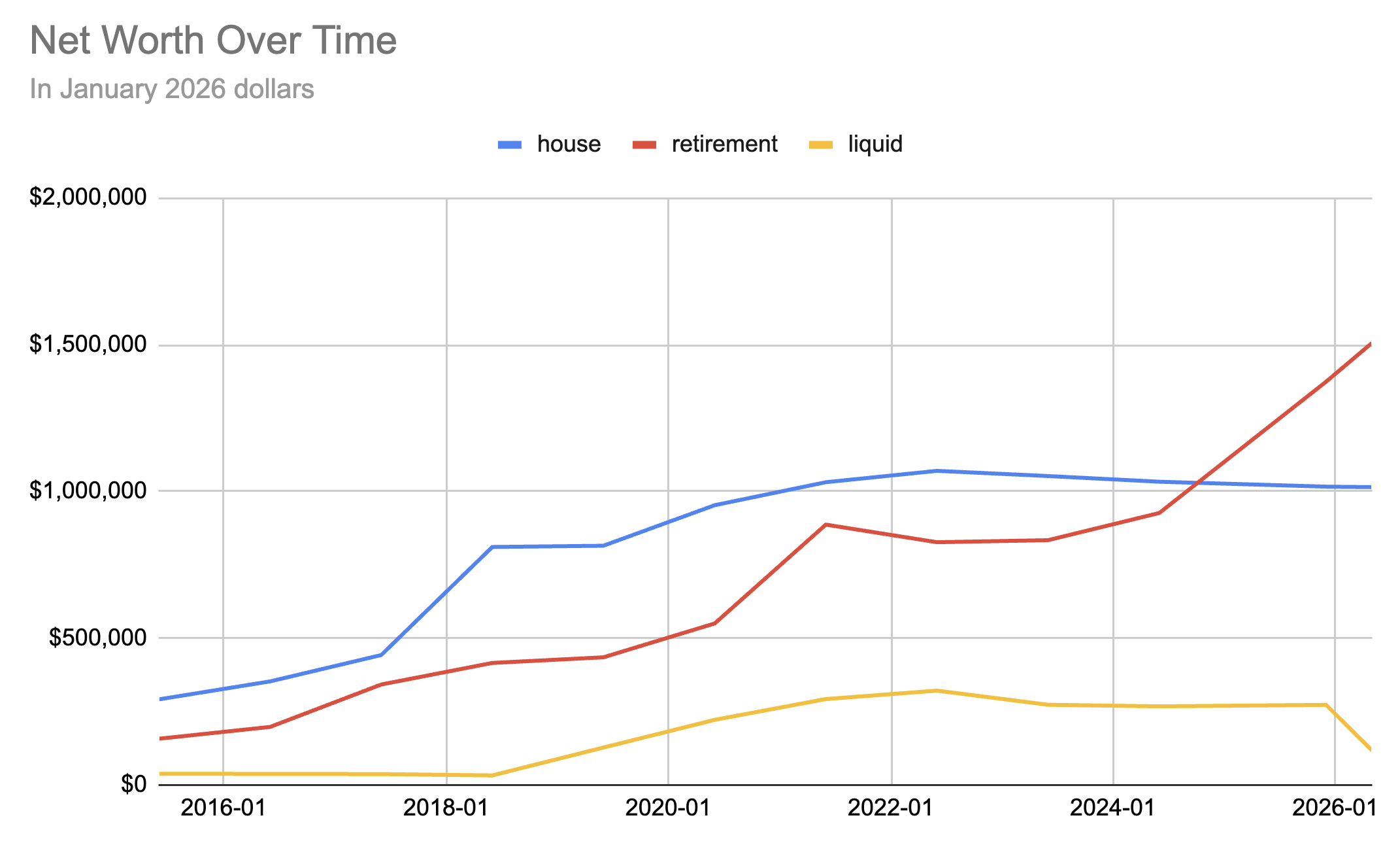

Even though we're drawing down our savings to donate, our net worth rose 18% over the last year (adjusted for inflation). This was driven by stock returns on our retirement savings:

Now, retirement savings growing via stock returns is how it's "supposed" to work: if we give away all the gains then we'll have much less at retirement. But I see ~three futures as AI becomes rapidly more capable:

It's really only in that last world where our savings translate into us having a better life, and as AI continues not hitting a wall I see the chances of ending up in a basically normal world getting pretty small. While we shouldn't donate to where we'd be destitute if we're wrong, we're not in danger of that. [1] So I think we should continue to draw down our non-retirement savings to donate more during this critical period.

Writing this post also got me thinking about our retirement contributions. We're both contributing the maximum, which I think often makes sense even if you don't expect a normal retirement, from a perspective of protecting savings. Since we're in a good enough position financially and donating seems very urgent, I now think we should stop contributing to have more to donate going forward.

Back in 2024 I made a list of what I expected to write in 2026. How did reality differ from expectations?

2024: I think there's a good chance we'll have switched from giving 50% to some form of salary sacrifice. If we do, our pay, donations, and taxes will all be a lot lower.

I did this for a little while. I started at a 10% reduction, and then when Julia's work decided to no longer support voluntary salary reductions I went to 75%. Then a few months ago I decided to stop since I wanted more flexibility in targeting donations.

2024: Childcare should be similar: the nanny share is working and I expect we'll do something similar at least until our youngest starts kindergarten in Fall 2026 (and will show up in the 2028 update).

Yup, still doing a nanny share with our former housemate. While there was a bit where our nanny left and it took us a few tries to find someone who worked out, this is now going well again. We haven't decided what we'll do for afterschool when our youngest starts school in the Fall.

2024: I'd like to hope I have a better way of accounting for housing and savings in general and have gone back and redone all my previous numbers under the new system, but since that sounds like a ton of work I doubt I'll have done that.

My prediction that I would be lazy was correct. This post represents zero accounting improvements, only more data due to the passage of time.

2024: I put about a 10% chance on AI, war, or other major events in this timeframe changing things enough that everything is weird in hard to predict ways.

The world is appreciably different from two years ago, but not in ways that strongly impacted our spending.

Let's try and make some similar predictions for 2028:

I've used the same approach as last year, which was unchanged from 2022 and very similar before then. Numbers below are monthly, based on 2025 spending.

[1] Our house is 2/3 paid off, if we used savings to finish it off that would leave ~$1M saved. At a 4% safe withdrawal income this would be $3.3k/month. We also rent out several parts of our house, totaling $4.8k/month, which brings us to ~$100k/y of raw income. This would need to cover taxes, health insurance, utilities, house maintenance, food, etc, but almost everyone lives on far less. I think the largest risk is that we get a non-extinction future that's still quite bad, but I have trouble seeing moderately higher savings making a large difference there.

I find this quite moving! Sometimes people wonder "do those folks talking about imminent AI risk even take their beliefs seriously?". Well, here we go!