Comments

Here's a twitter thread by Nathan Young with some further discussion and links to Manifold markets about the sale's impact on the FTX Future Fund.

Here's a twitter thread by Nathan Young with some further discussion and links to Manifold markets about the sale's impact on the FTX Future Fund.

A group of us attempted to put the relevant facts and forecasts in one place to give clarity: https://forum.effectivealtruism.org/posts/yjGye7Q2jRG3jNfi2/ftx-will-probably-be-sold-at-a-steep-discount-this-is-bad

This comment is speculative/editorial.

Coordination / Bailout

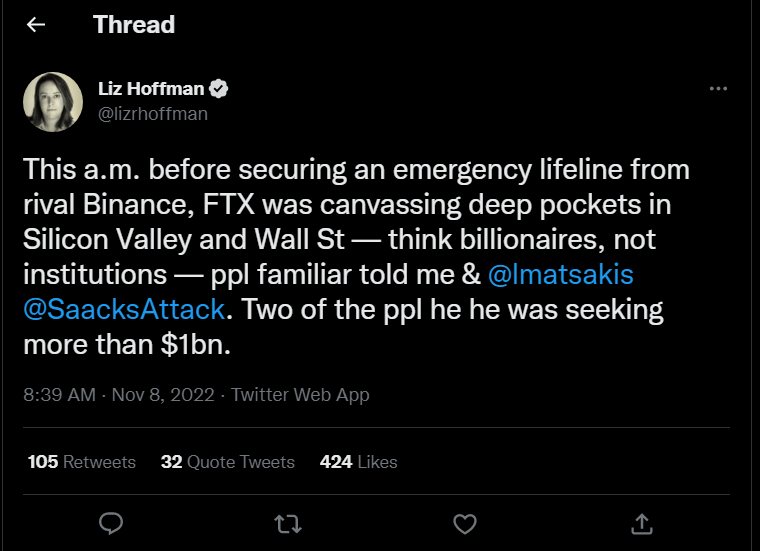

Some sort of coordination or saving of FTX seems desirable. Relevant to this, tweets by Liz Hoffman claims FTX reached out this morning privately for aid. The ask may have started at $1B, but in a few hours the need rose to $5B.

https://twitter.com/lizrhoffman/status/1590021299295768578

If this is true, it seems plausible that the smaller amount could have been secured, but the increasingly larger amounts made it difficult. This seems relevant to ideas about coordination or bailout.

Cause of collapse seems relevant / Bank run seems problematic

Notice that it's unclear how collapse of its tokens and especially a run of withdrawals would cause solvency or liquidity issues for FTX.

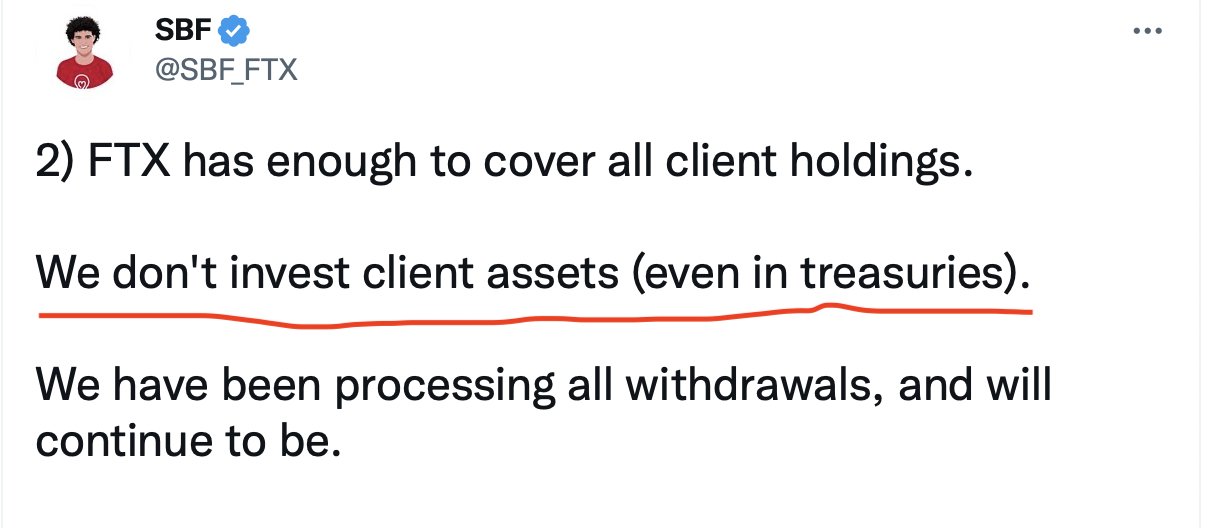

For customer deposits, FTX should be holding assets as cash/tokens, not lending them out or leveraging them. This is what SBF has represented.

It seems possible that FTX had leveraged non-customer assets as part of its business strategy, and the collapse took them by surprise. It could be the suspension of customer withdrawals was simply due to the volume of withdrawals (the amount was rumored to be up to $6B this Tuesday).

It seems good for to EA that this is explained. It seems that SBF, EA competency, and the long term future seems all associated by now.

SBF seems like a very good person. Almost regardless of what happened, I don't think a reasonable person's opinion of him should be reduced.

All of the FTX regranters and the FTX grantees, seem to be very virtuous and effective EAs[1]. FTX funding seemed to be building deeper competency in other areas. This seems like a huge loss for EA.

I have never received or applied for FTX funding and I never took any actions to lead me being funded by the FTX FF. In the past, FTX regranters approached me.

SBF seems like a very good person. Almost regardless of what happened, I don't think a reasonable person's opinion of him should be reduced.

I think if he lied publicly about whether FTX's client assets were not invested then I think this should very much reduce a reasonable person's opinion of him. If lying straightforwardly in public does not count against your character, I don't know what else would.

That said, I don't actually know whether any lying happened here. The real situation seems to be messy, and it's plausible that all of FTX's client assets (and not like derivatives) were indeed not invested, but that the thing that took FTX out were the leveraged derivates they were selling, which required more advanced risk-balancing, though I do think that Twitter thread looks really quite suspicious right now.

Matt Levine seems to think it was the leveraged derivatives. I will quote him at length:

One question that might be too early to answer is: Why was there a liquidity crunch in the first place? A crypto exchange is a weird sort of business, in many ways more like a brokerage than a traditional exchange. The simplest way to run the business is to take deposits from customers, buy crypto for the customers, keep everything segregated, and make money on commissions. Coinbase Global Inc.’s balance sheets are public, and pretty simple: It has about $101 billion of customer cash and crypto assets, and about $101 billion of offsetting customer liabilities. If the customers asked for their $101 billion back, presumably Coinbase would just give it to them.

A more complicated way to do it is to provide leverage to customers: Instead of taking $100 of customer cash to buy $100 worth of Bitcoin, you take $100 of customer cash to buy $200 worth of Bitcoin. A lot of FTX’s business is in perpetual futures, a leveraged product, sometimes levered 20 to 1. If you are an exchange and you are in this sort of business, you will need to come up with the extra $100 to lend to your customer. Presumably that doesn’t come from your equity: You are doing some sort of borrowing, perhaps from other customers, perhaps from outside financing sources, perhaps from your affiliated hedge fund, etc. You will have some customers who owe you money, and others whom you owe money. You will be like a bank. If everyone to whom you owe money demands their money back at once, you will need to get the money back from the ones who owe you money, which might be hard. (You might not have a contractual right to demand the money back right away, or it might be rude and bad for business, or you might have to liquidate them to get the money back and that would blow up the value of your collateral.) In broad strokes this is a reasonable description of what happened to Bear Stearns, a brokerage that financed its customers’ positions. If you are a crypto exchange that provides leverage, then you are probably bank-like enough for a run on the bank.

Another complicated way to do it is that you take your customers’ assets and go invest them in whatever sounds good to you. You’re holding Solana tokens for a customer, you invest them in some yield-farming thing to make some extra cash, if the customer asks for the tokens back you don’t have them, etc. This is more or less what brought down the Celsiuses and Voyagers and BlockFis of the world, but I would not have expected it from FTX. “FTX has enough to cover all client holdings,” Bankman-Fried tweeted yesterday. “We don’t invest client assets (even in treasuries).”

Alas, the original tweets from SBF appear to be down now. Not sure whether that's much of an update, though it does look very vaguely suspicious.

I'm confused about this. This seems to explain why customers with invested assets can't withdraw immediately. But if a customer has only cash in their account, why can't they withdraw it if it's not being invested? If customer A's cash is being used to secure margin loans for customer B, then how is it true that customer A's cash is "not invested"?

Without trying to make an affirmative statement about what happened at FTX or saying there wasn't any other factors, it seems likely that the idea "that customer funds solely belong to the customer and don't mix with other funds" is simplistic and effectively impossible in any leveraged trading system. In reality, what happens is governed by risk management/capital controls, that would almost always blow up in a bank run scenario of the magnitude that happened to FTX.

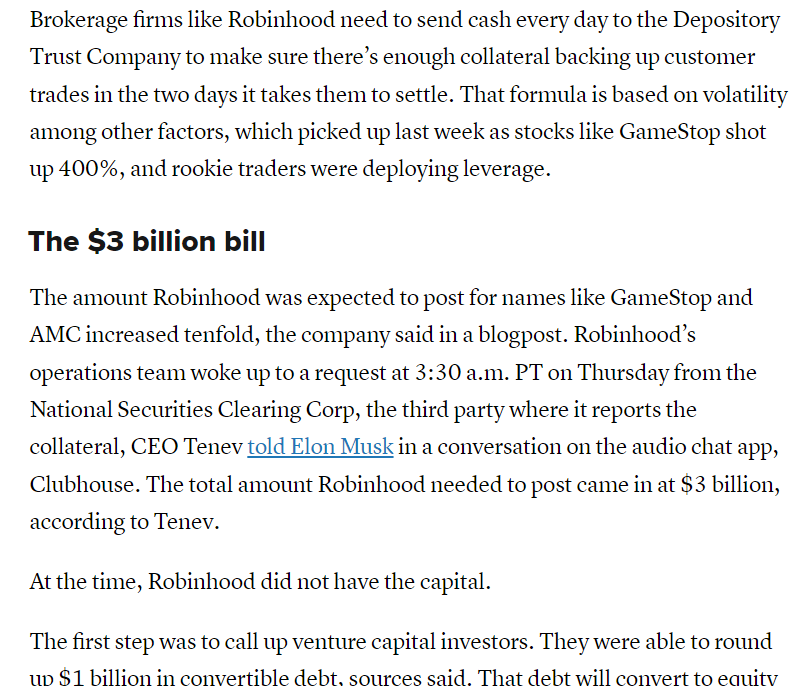

For example, Robinhood, which no one believes was speculating on customer funds, had a huge crisis in Jan 2021, that needed billions of dollars. This was just due to customer leverage (and probably bad risk management, the magnitudes seem much than what FTX faced this week).

Is it not ominous that people were prepared to wriye Robinhood a check, but not FTX?

Your comment is valid. This reply is getting into sort of low quality/twitter/reddit style speculation and I might stop writing after this:

Some factors that seem different:

It's worth noting that FTX has previously been in trouble with the FDIC for misrepresenting how funds were stored: https://www.msn.com/en-ca/money/topstories/crypto-exchange-ftx-ordered-to-halt-false-and-misleading-claims-by-us-bank-regulator/ar-AA10QJdY

The Federal Deposit Insurance Corporation said a July tweet by Brett Harrison, head of FTX's U.S. operations, contained misleading claims that funds held at and stocks purchased through FTX were FDIC insured, and ordered the company to remove any misleading language from its social media accounts and websites.

In the tweet, which Harrison has since deleted, he stated that direct deposits from employers to the crypto exchange are “stored in individually FDIC-insured bank accounts” and that stocks purchased via FTX US “are held in FDIC-insured” brokerage accounts. The FDIC said in its cease and desist letter to FTX US that those statements implied that FDIC insurance was available for cryptocurrency and stock holdings, and that the agency does not insure brokerage accounts.

In a tweet on Friday, FTX CEO Sam Bankman-Fried emphasized FTX is not FDIC-insured, and apologized if anyone misinterpreted previous comments.

What you said is valid in general. As a reply/rebuttal, I think your focus/association with "lying" is misdirected or stilted.

Basically, what probably happened to FTX is something like the financial engineering described in this link in this top level post: https://dirtybubblemedia.substack.com/p/is-alameda-research-insolvent. This take, which is quite hostile, doesn't involve lying per se.

It's extremely difficult to communicate how normalized something like the above has become, and how much of the "tech" and business success in the 2010s was the result of similar financial engineering and loose capital.

Succeeding in this way, while not lying, is not exactly honest either. But in this moral space, I strongly put all of my support behind SBF and his decisions as a person, based on his choices and goals.

Before ending today's weird sojourn into corporate finance, I want to point out it's really disappointing how this has been discussed. I don't think the modesty and general intuition most people have expressed is very good, the quality of the modal post wasn't very good (for its first ~10 revisions), and clearly voted up because of who the authors are; clueful, fair comments are shouted down, while EA leaders making making similar appeals to authority/applause lines are voted up.

It's wild you are at 30/23 here.

It's not just that most people don't understand, they are wildly brandishing their opinions and producing a weird ignorant cloud—it's hard to explain, but maybe this person might understand.

Zooming out, I think this is important because basically, it's possible EA is worse off, A LOT worse off, by having a billionaire come in and flame out like this, than not being there at all.

I guess there's several issues that need to be dealt with. But the one issue that I think is important and hard to handle well, is the perceptions of competency and spirit of EA.

Throwing off someone because they had a business failure, or pointing out their conduct disproportionately, because they are on the "way down", is at least as bad as sucking up to them and ignoring it on the way up, and to me, plausibly way worse.

So it's good to see SBF for who he is, and the work he did and decisions are quite likely entirely valid. That is why I wrote my parent comment and the first paragraphs of this comment.

the quality of the modal post wasn't very good (for its first ~10 revisions), and clearly voted up because of who the authors are; clueful, fair comments are shouted down, while EA leaders making making similar appeals to authority/applause lines are voted up

I have no particular opinion on SBF's character, but this paragraph seems ungenerous. Other than being a prolific poster and generally swell guy, Nathan doesn't seem particularly prominent in the EA community. Certainly not as much as Jonas Vollmer, who's a key figure at many EA orgs. And what appeal to authority did Ben's comment make?

Well, besides ignoring Nathan Young's huge clout, yes, this seems fair.

He bought a $20,000,000 penthouse with his spoils and lives in the lap of luxury. He's been flying private jets around the world and spending hundreds of millions of dollars trying to influence people to allow him to make more money. Thousands of less educated people put their money into his products which may have vanished. He's a bad person.

Yes, bribing celebrities to convince poor people to put their money into shitcoins is not altriusm. I hope he is sued and every penny is returned to those who fell for this. The EA community is going to need to have a moral reckoning over how the movement was hijacked by a conman.

A quick note[1] from a moderator (me) about discussions about recent events related to FTX:

The moderation team will be keeping an eye on these discussions — as we do with all discussions — and we plan to enforce the norms as usual. To be clear, however, we will not be censoring any particular perspective on the topic.

EDIT: I've made a forum post about it.

Some EAs could be destabilized in their mental health. We should install an emergency network also involving people not currently working as therapists but with previous professional experience. Can someone organize this? I've already reached out to the EA Mental Health Navigator and posted about it in the EA Mental Health slack channel.

I believe the title of this article is misleading - FTX.com was not technically bought out by Binance. Binance signed a non-binding letter of intent to buy FTX.com. Sometimes this is just a minor detail, but in this case it seems quite important. As of the time I am writing this comment (9 a.m. California time on November 9) Polymarket shows an 81% chance that Binance will pull out of this deal.

https://polymarket.com/market/will-binance-pull-out-of-their-ftx-deal

I am not an expert in crypto, but I think people should not assume that this acquisition will go through. It is possible that FTX will just become insolvent. See the relevant Polymarket:

https://polymarket.com/market/will-ftx-become-insolvent-by-eoy

Yes you're right. Yesterday morning, the title was less inflammatory and a reasonably factual statement.

The post is less relevant and sliding off the FP, I'll probably delete the entire post at some point (the comments will remain).

Few more things on FTX/Alameda (from Financial Times’ Alphaville blog)

Reuters on what may have happened (ie possible transactions connecting FTX and Alameda as well as Binance’s opaque history)

An old story on SBF & FTX’s history & connections to EA

https://www.sequoiacap.com/article/sam-bankman-fried-spotlight/

Probably less directly relevant now (except as it impacts crypto values generally), but some info on Binance’s opaque financial arrangements

"Ripping off all those innocent Ponzi scheme victims was totally worth it for the future trillions of people SBF will be able to pay for... I'm sorry, I'm hearing that he's lost his entire net worth." What a great day for humanity.

Peter Layman has violated Forum norms in a variety of ways since joining. We are banning Peter for a month with a warning; if their engagement with the Forum continues to violate norms after the ban, we will ban them for a longer period of time.

Here’s a list of some norm violations (this list might not be exhaustive):

I guess the rules should be the same for everyone, but I'm kind of worried a ban in this case makes us look thin-skinned and unable to take criticism. (For what it's worth I think that the titles of the first 2 of the link posts are fine, albeit strongly phrased.)

It's shocking that this post has -67 views. Peter Layman, you are the only honest person in the EA community, and that you are being buried for highlighting a simple truth speaks to how bad the EA community is at assessing the impact it has on the world. This post should not have -67 votes. There is a rampant tribalism mindset within EA, despite the fact that this community is explicitly built on the rationality of rejecting tribalism. Too funny.

As a moderator, I think this comment is unnecessarily rude or snarky ("too funny" is clearly adversarial, which is not generous or collaborative) and breaks Forum norms. Please don't leave any more comments like this or you might be banned from the Forum.

[Addition: I should clarify that the norm-violating behavior is not criticizing EA or the content of what you're saying about tribalism etc., but rather the tone of the comment.]

See: https://twitter.com/SBF_FTX/status/1590012124864348160

This is probably related to liquidity issues / solvency issues.

Sketch of timeline:

Curious about what this implies -

We attempted to answer the third question here: https://forum.effectivealtruism.org/posts/yjGye7Q2jRG3jNfi2/ftx-will-probably-be-sold-at-a-steep-discount-this-is-bad